EX-99.2

Published on July 16, 2025

Exhibit 99.2

Table of Contents.

|

||||||||

| Section | Page | ||||

| Corporate Data: | |||||

| Consolidated Financial Results: | |||||

| Portfolio Data: | |||||

Disclosures:

Forward-Looking Statements: This supplemental package contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. We caution investors that any forward-looking statements presented herein are based on management’s beliefs and assumptions and information currently available to management. Such statements are subject to risks, uncertainties and assumptions and may be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. These risks and uncertainties include, without limitation: general risks affecting the real estate industry (including, without limitation, the market value of our properties, the inability to enter into or renew leases at favorable rates, portfolio occupancy varying from our expectations, dependence on tenants’ financial condition, and competition from other developers, owners and operators of real estate); risks associated with the disruption of credit markets or a global economic slowdown; risks associated with the potential loss of key personnel (most importantly, members of senior management); risks associated with our failure to maintain our status as a Real Estate Investment Trust under the Internal Revenue Code of 1986, as amended; possible adverse changes in tax and environmental laws; an epidemic or pandemic (such as the outbreak and worldwide spread of novel coronavirus (COVID-19), and the measures that international, federal, state and local governments, agencies, law enforcement and/or health authorities may implement to address it, which may (as with COVID-19) precipitate or exacerbate one or more of the above-mentioned factors and/or other risks, and significantly disrupt or prevent us from operating our business in the ordinary course for an extended period; litigation, including costs associated with prosecuting or defending pending or threatened claims and any adverse outcomes, and potential liability for uninsured losses and environmental contamination.

For a further discussion of these and other factors that could cause our future results to differ materially from any forward-looking statements, see Item 1A. Risk Factors in our 2024 Annual Report on Form 10-K, which was filed with the Securities and Exchange Commission (“SEC”) on February 10, 2025, and other risks described in documents we subsequently file from time to time with the SEC. We disclaim any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, of new information, data or methods, future events or other changes.

Our credit ratings, which are disclosed on page 4, may not reflect the potential impact of risks relating to the structure or trading of the Company's securities and are provided solely for informational purposes. Credit ratings are not recommendations to buy, sell or hold any security, and may be revised or withdrawn at any time by the issuing organization in its sole discretion. The Company does not undertake any obligation to maintain the ratings or to advise of any change in ratings. Each agency's rating should be evaluated independently of any other agency's rating. An explanation of the significance of the ratings may be obtained from each of the rating agencies.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 2

|

|

||||||

Investor Company Summary.

|

||||||||

| Executive Management Team | ||||||||

| Howard Schwimmer | Co-Chief Executive Officer, Director | |||||||

| Michael S. Frankel | Co-Chief Executive Officer, Director | |||||||

| Laura Clark | Chief Operating Officer | |||||||

| Michael Fitzmaurice | Chief Financial Officer | |||||||

David E. Lanzer |

General Counsel and Corporate Secretary | |||||||

| Board of Directors | ||||||||

| Tyler H. Rose | Chairman |

|||||||

| Howard Schwimmer | Co-Chief Executive Officer, Director | |||||||

| Michael S. Frankel | Co-Chief Executive Officer, Director | |||||||

| Robert L. Antin | Director | |||||||

| Diana J. Ingram | Director | |||||||

| Angela L. Kleiman | Director | |||||||

| Debra L. Morris | Director | |||||||

| Investor Relations Information | ||||||||

Mikayla Lynch | ||||||||

Director, Investor Relations and Capital Markets |

||||||||

mlynch@rexfordindustrial.com | ||||||||

| Equity Research Coverage | ||||||||||||||||||||||||||||||||

| BofA Securities | Samir Khanal |

(646) 855-1497 |

J.P. Morgan Securities | Michael Mueller | (212) 622-6689 | |||||||||||||||||||||||||||

| Barclays | Brendan Lynch | (212) 526-9428 | Jefferies LLC | Jonathan Petersen | (212) 284-1705 | |||||||||||||||||||||||||||

| BMO Capital Markets | John Kim | (212) 885-4115 | Mizuho Securities USA | Vikram Malhotra | (212) 282-3827 | |||||||||||||||||||||||||||

| BNP Paribas Exane | Nate Crossett | (646) 342-1588 | Robert W. Baird & Co. | Nicholas Thillman | (414) 298-5053 | |||||||||||||||||||||||||||

| Citigroup Investment Research | Craig Mailman | (212) 816-4471 | Scotiabank | Greg McGinniss | (212) 225-6906 | |||||||||||||||||||||||||||

| Colliers Securities | Barry Oxford | (203) 961-6573 | Truist Securities | Anthony Hau | (212) 303-4176 | |||||||||||||||||||||||||||

Deutsche Bank |

Omotayo Okusanya | (212) 250-9284 |

Wedbush Securities | Richard Anderson | (212) 931-7001 | |||||||||||||||||||||||||||

Evercore ISI |

Steve Sakwa | (212) 446-9462 | Wells Fargo Securities | Blaine Heck | (443) 263-6529 | |||||||||||||||||||||||||||

| Green Street Advisors | Vince Tibone | (949) 640-8780 | Wolfe Research | Andrew Rosivach | (646) 582-9250 | |||||||||||||||||||||||||||

Disclaimer: This list may not be complete and is subject to change as firms add or delete coverage of our company. Please note that any opinions, estimates, forecasts or predictions regarding our historical or predicted performance made by these analysts are theirs alone and do not represent opinions, estimates, forecasts or predictions of Rexford Industrial Realty, Inc. or its management. We are providing this listing as a service to our stockholders and do not by listing these firms imply our endorsement of, or concurrence with, such information, conclusions or recommendations. Interested persons may obtain copies of analysts’ reports on their own; we do not distribute these reports.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 3

|

|

||||||

Company Overview.

|

||||||||

| For the Quarter Ended June 30, 2025 | ||||||||

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 4

|

|

||||||

Highlights - Consolidated Financial Results.

|

||||||||

| Quarterly Results | (in millions) | |||||||

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 5

|

|

||||||

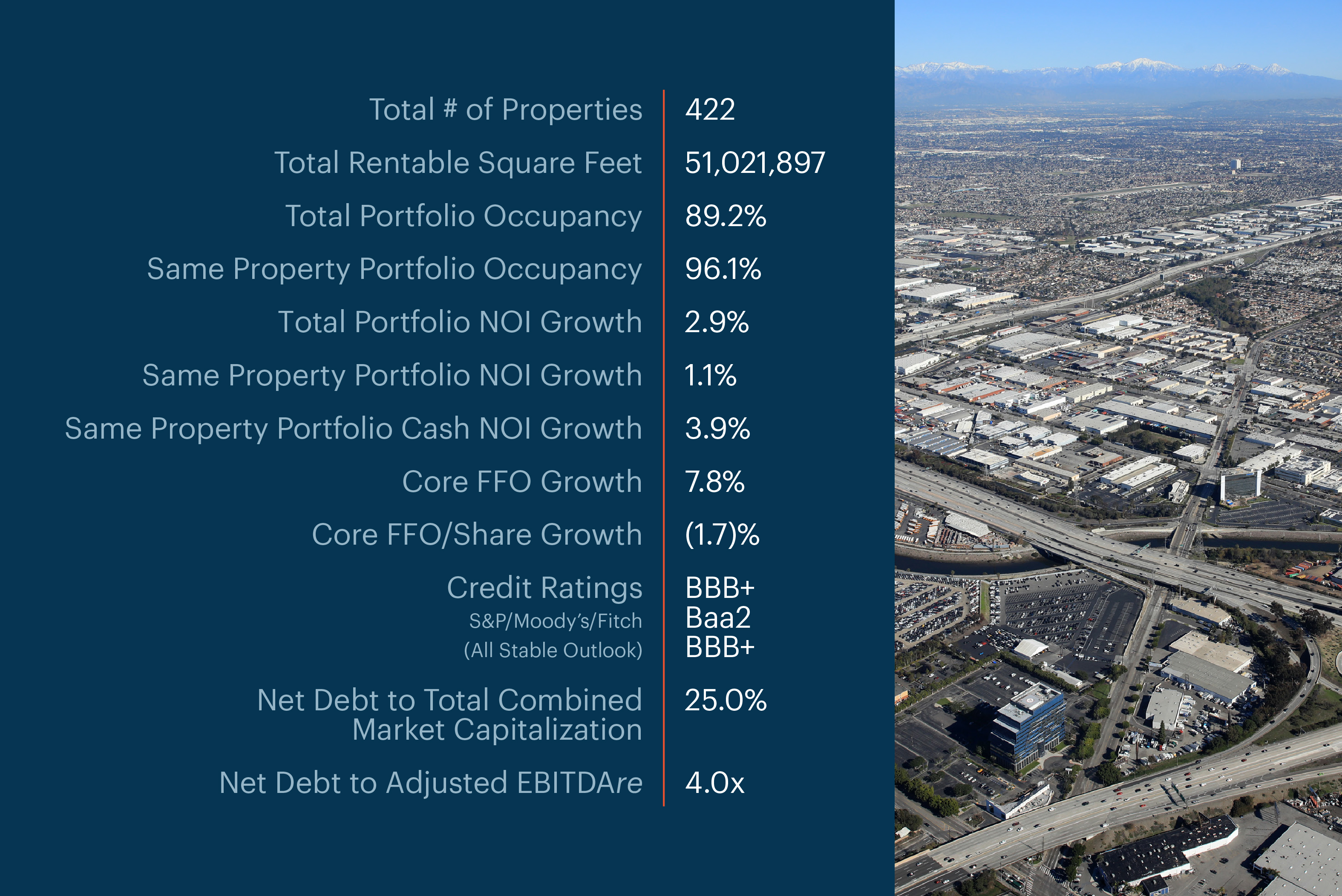

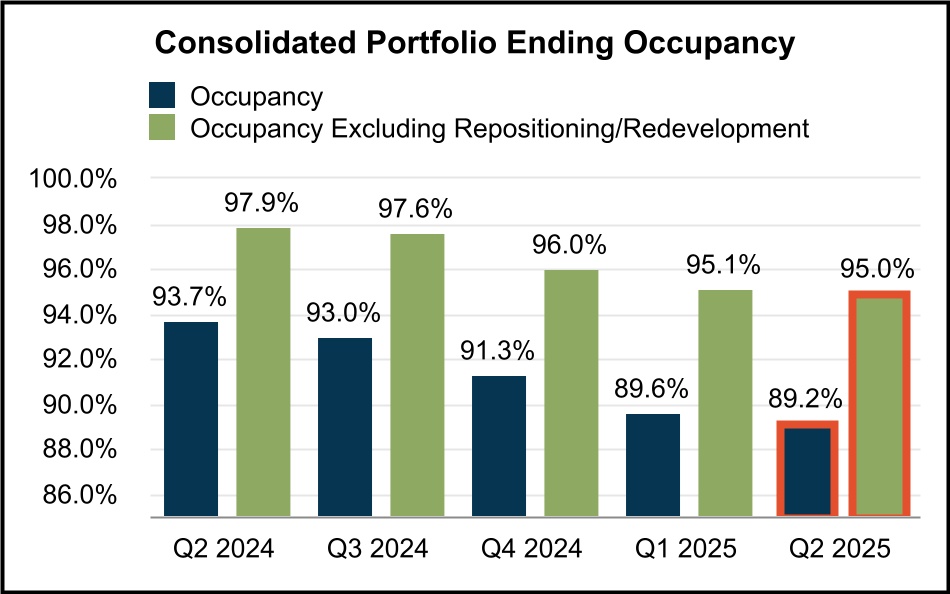

Financial and Portfolio Highlights and Capitalization Data.(1)

|

||||||||

| (in thousands except share and per share data and portfolio statistics) | ||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| June 30, 2025 | March 31, 2025 | December 31, 2024 | September 30, 2024 | June 30, 2024 | |||||||||||||||||||||||||

| Financial Results: | |||||||||||||||||||||||||||||

| Total rental income | $ | 241,568 | $ | 248,821 | $ | 239,737 | $ | 238,396 | $ | 232,973 | |||||||||||||||||||

| Net income | $ | 120,394 | $ | 74,048 | $ | 64,910 | $ | 70,722 | $ | 86,017 | |||||||||||||||||||

| Net Operating Income (NOI) | $ | 186,270 | $ | 193,560 | $ | 183,731 | $ | 183,529 | $ | 181,068 | |||||||||||||||||||

| Company share of Core FFO | $ | 139,709 | $ | 141,023 | $ | 128,562 | $ | 130,011 | $ | 129,575 | |||||||||||||||||||

| Company share of Core FFO per common share - diluted | $ | 0.59 | $ | 0.62 | $ | 0.58 | $ | 0.59 | $ | 0.60 | |||||||||||||||||||

Adjusted EBITDAre

|

$ | 184,111 | $ | 184,859 | $ | 179,347 | $ | 175,929 | $ | 178,106 | |||||||||||||||||||

| Dividend declared per common share | $ | 0.4300 | $ | 0.4300 | $ | 0.4175 | $ | 0.4175 | $ | 0.4175 | |||||||||||||||||||

| Portfolio Statistics: | |||||||||||||||||||||||||||||

| Portfolio rentable square feet (“RSF”) | 51,021,897 | 50,952,137 | 50,788,225 | 50,067,981 | 49,710,628 | ||||||||||||||||||||||||

| Ending occupancy | 89.2% | 89.6% | 91.3% | 93.0% | 93.7% | ||||||||||||||||||||||||

Ending occupancy excluding repositioning/redevelopment(2)

|

95.0% | 95.1% | 96.0% | 97.6% | 97.9% | ||||||||||||||||||||||||

| Net Effective Rent Change | 20.9% | 23.8% | 55.4% | 39.2% | 67.7% | ||||||||||||||||||||||||

| Cash Rent Change | 8.1% | 14.7% | 41.0% | 26.7% | 49.0% | ||||||||||||||||||||||||

| Same Property Portfolio Performance: | |||||||||||||||||||||||||||||

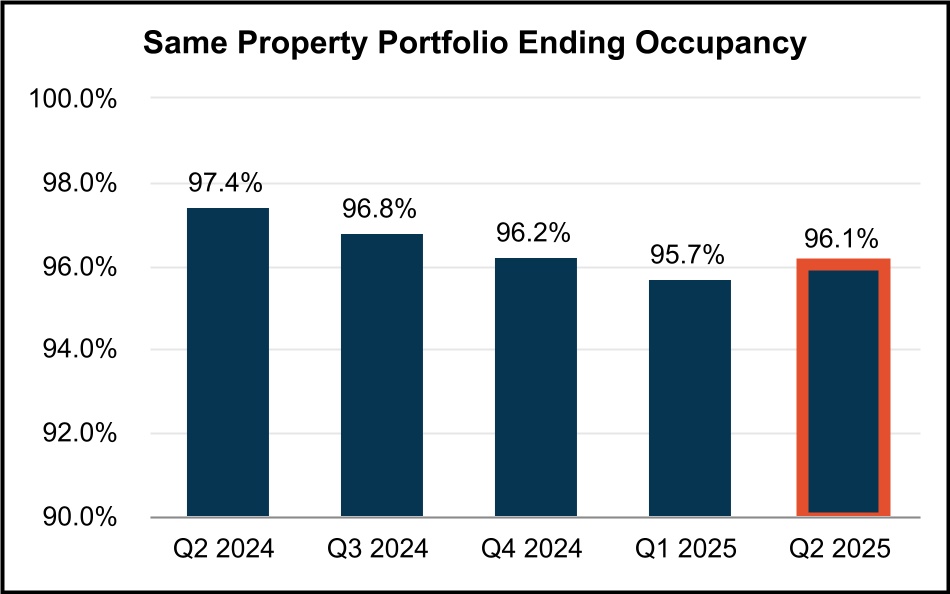

Same Property Portfolio ending occupancy(3)(4)

|

96.1% | 95.7% | 96.2% | 96.8% | 97.4% | ||||||||||||||||||||||||

Same Property Portfolio NOI growth(4)(5)

|

1.1% | 0.7% | |||||||||||||||||||||||||||

Same Property Portfolio Cash NOI growth(4)(5)

|

3.9% | 5.0% | |||||||||||||||||||||||||||

| Capitalization: | |||||||||||||||||||||||||||||

Total shares and units issued and outstanding at period end(6)

|

244,334,274 | 244,310,773 | 233,295,793 | 227,278,210 | 225,623,274 | ||||||||||||||||||||||||

| Series B and C Preferred Stock and Series 1, 2 and 3 CPOP Units | $ | 173,250 | $ | 173,250 | $ | 213,956 | $ | 213,956 | $ | 214,000 | |||||||||||||||||||

| Total equity market capitalization | $ | 8,864,220 | $ | 9,738,017 | $ | 9,233,171 | $ | 11,648,323 | $ | 10,274,542 | |||||||||||||||||||

| Total consolidated debt | $ | 3,379,141 | $ | 3,379,383 | $ | 3,379,622 | $ | 3,386,273 | $ | 3,386,559 | |||||||||||||||||||

| Total combined market capitalization (net debt plus equity) | $ | 11,812,244 | $ | 12,612,821 | $ | 12,556,822 | $ | 14,972,760 | $ | 13,535,391 | |||||||||||||||||||

| Ratios: | |||||||||||||||||||||||||||||

| Net debt to total combined market capitalization | 25.0% | 22.8% | 26.5% | 22.2% | 24.1% | ||||||||||||||||||||||||

Net debt to Adjusted EBITDAre (quarterly results annualized)

|

4.0x | 3.9x | 4.6x | 4.7x | 4.6x | ||||||||||||||||||||||||

(1)For definition/discussion of non-GAAP financial measures & reconciliations to their nearest GAAP equivalents, see definitions section & reconciliation section beginning on page 34 and page 12 of this report, respectively.

(2)Ending occupancy excluding repositioning/redevelopment excludes “Other Repositioning” projects as well as those listed individually on pages 26-31.

(3)Reflects the ending occupancy for the 2025 Same Property Portfolio for each period presented. For historical ending occupancy as reported in prior Supplemental packages, see “SPP Historical Information” on page 37.

(4)For comparability, Same Property Portfolio ending occupancy, NOI growth and Cash NOI growth for all comparable periods have been restated to remove the results of two properties that were sold during Q2’25 and two buildings that were moved to Other Repositioning. See page 32 for details related to dispositions.

(5)Represents the year over year percentage change in NOI and Cash NOI for the Same Property Portfolio.

(6)Includes the following # of OP Units/vested LTIP units held by noncontrolling interests: 8,182,445 (Jun 30, 2025), 8,700,301 (Mar 31, 2025), 8,426,905 (Dec 31, 2024), 8,175,868 (Sep 30, 2024) and 8,218,426 (Jun 30, 2024). Excludes the following # of shares of unvested restricted stock: 542,922 (Jun 30, 2025), 560,382 (Mar 31, 2025), 416,123 (Dec 31, 2024), 405,003 (Sep 30, 2024) and 435,225 (Jun 30, 2024). Excludes unvested LTIP units and unvested performance units.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 6

|

|

||||||

Guidance.

|

||||||||

| As of June 30, 2025 | ||||||||

2025 OUTLOOK*

| METRIC |

Q2-2025 UPDATED

GUIDANCE

|

Q1-2025

GUIDANCE

|

YTD RESULTS AS OF JUNE 30, 2025 | |||||||||||||||||

Net Income Attributable to Common Stockholders per diluted share (1)(2)

|

$1.38 - $1.42 | $1.31 - $1.35 | $0.78 | |||||||||||||||||

Company share of Core FFO per diluted share (1)(2)

|

$2.37 - $2.41 | $2.37 - $2.41 | $1.21 | |||||||||||||||||

Same Property Portfolio NOI Growth - GAAP (3)

|

0.75% - 1.25% | 0.75% - 1.25% | 0.9% | |||||||||||||||||

Same Property Portfolio NOI Growth - Cash (3)

|

2.25% - 2.75% | 2.25% - 2.75% | 4.5% | |||||||||||||||||

Average Same Property Portfolio Occupancy (Full Year) (3)(4)

|

95.5% - 96.0% | 95.5% - 96.0% | 95.9% | |||||||||||||||||

Net General and Administrative Expenses (5)

|

+/- $82M | +/- $82M | $39.6M | |||||||||||||||||

| Net Interest Expense | +/- $107M | +/- $109.5M | $54.0M | |||||||||||||||||

(1)Our 2025 Net Income and Core FFO guidance refers to the Company's in-place portfolio as of June 30, 2025, and does not include any assumptions for additional prospective acquisitions, dispositions or related balance sheet activities that have not closed.

(2)See page 38 for a reconciliation of the Company’s 2025 guidance range of net income attributable to common stockholders per diluted share, the most directly comparable forward-looking GAAP financial measure, to Company share of Core FFO per diluted share.

(3)Our 2025 Same Property Portfolio is a subset of our consolidated portfolio and includes properties that were wholly owned by us for the period from January 1, 2024 through June 30, 2025, and excludes properties that were or will be classified as repositioning/redevelopment (current and future) or lease-up during 2024 and 2025 (as separately listed on pages 26-31) and select buildings in “Other Repositioning.” As of June 30, 2025, our 2025 Same Property Portfolio consisted of buildings aggregating 38.0 million rentable square feet at 289 of our properties, representing 80% of Q2-2025 total portfolio NOI.

(4)Calculated by averaging the occupancy rate at the end of each month during the year-to-date period and December 2024.

(5)Our Net 2025 General and Administrative expense guidance includes estimated non-cash equity compensation expense of $37.3 million.

* A number of factors could impact the Company’s ability to deliver results in line with its guidance, including, but not limited to, interest rates, inflation, the economy, the supply and demand of industrial real estate, the availability and terms of financing to the Company or to potential acquirers of real estate and the timing and yields for divestment and investment. There can be no assurance that the Company can achieve such results.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 7

|

|

||||||

Guidance (Continued).

|

||||||||

| As of June 30, 2025 | ||||||||

2025 Guidance Rollforward (1)

| Earnings Components | Range ($ per share) |

Notes | ||||||||||||||||||

Q1 2025 Core FFO Per Diluted Share Guidance |

$2.37 | $2.41 | ||||||||||||||||||

| Same Property Portfolio NOI Growth | — | — | SP Net Effective NOI growth guidance unchanged 0.75% - 1.25% |

|||||||||||||||||

Repositioning/Redevelopment NOI |

(0.01) | (0.01) | Projected rent commencement timing extended |

|||||||||||||||||

Net General & Administrative Expenses (2)

|

— | — | Guidance unchanged +/- $82M |

|||||||||||||||||

| Net Interest Expense | 0.01 | 0.01 | Guidance updated +/- $107M |

|||||||||||||||||

Current 2025 Core FFO Per Diluted Share Guidance |

$2.37 | $2.41 | ||||||||||||||||||

| Core FFO Per Diluted Share Annual Growth | 1% | 3% | ||||||||||||||||||

(1)2025 Guidance and Guidance Rollforward represent the in-place portfolio as of June 30, 2025, and does not include any assumptions for additional prospective acquisitions, dispositions or related balance sheet activities that have not closed unless otherwise noted.

(2)Our Net 2025 General and Administrative expense guidance includes estimated non-cash equity compensation expense of $37.3 million.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 8

|

|

||||||

Consolidated Balance Sheets.

|

||||||||

| (unaudited and in thousands) | ||||||||

| June 30, 2025 | March 31, 2025 | December 31, 2024 | September 30, 2024 | June 30, 2024 | |||||||||||||||||||||||||

| ASSETS | |||||||||||||||||||||||||||||

| Land | $ | 7,787,021 | $ | 7,797,744 | $ | 7,822,290 | $ | 7,703,232 | $ | 7,650,740 | |||||||||||||||||||

| Buildings and improvements | 4,594,494 | 4,573,881 | 4,611,987 | 4,416,032 | 4,330,709 | ||||||||||||||||||||||||

| Tenant improvements | 186,429 | 181,632 | 188,217 | 181,785 | 178,832 | ||||||||||||||||||||||||

| Furniture, fixtures, and equipment | 132 | 132 | 132 | 132 | 132 | ||||||||||||||||||||||||

| Construction in progress | 431,807 | 386,719 | 333,690 | 370,431 | 343,275 | ||||||||||||||||||||||||

| Total real estate held for investment | 12,999,883 | 12,940,108 | 12,956,316 | 12,671,612 | 12,503,688 | ||||||||||||||||||||||||

| Accumulated depreciation | (1,070,684) | (1,021,151) | (977,133) | (925,373) | (874,413) | ||||||||||||||||||||||||

| Investments in real estate, net | 11,929,199 | 11,918,957 | 11,979,183 | 11,746,239 | 11,629,275 | ||||||||||||||||||||||||

| Cash and cash equivalents | 431,117 | 504,579 | 55,971 | 61,836 | 125,710 | ||||||||||||||||||||||||

| Restricted cash | 130,071 | 50,105 | — | — | — | ||||||||||||||||||||||||

| Loan receivable, net | 123,474 | 123,359 | 123,244 | 123,129 | 123,014 | ||||||||||||||||||||||||

| Rents and other receivables, net | 12,861 | 17,622 | 15,772 | 17,315 | 17,685 | ||||||||||||||||||||||||

| Deferred rent receivable, net | 173,691 | 166,893 | 161,693 | 151,637 | 140,196 | ||||||||||||||||||||||||

| Deferred leasing costs, net | 71,482 | 70,404 | 67,827 | 69,152 | 68,161 | ||||||||||||||||||||||||

| Deferred loan costs, net | 7,892 | 1,642 | 1,999 | 2,356 | 2,713 | ||||||||||||||||||||||||

Acquired lease intangible assets, net(1)

|

169,036 | 182,444 | 201,467 | 205,510 | 220,021 | ||||||||||||||||||||||||

Acquired indefinite-lived intangible asset |

5,156 | 5,156 | 5,156 | 5,156 | 5,156 | ||||||||||||||||||||||||

Interest rate swap assets |

3,586 | 5,580 | 8,942 | 3,880 | 16,510 | ||||||||||||||||||||||||

| Other assets | 15,765 | 20,730 | 26,964 | 34,092 | 18,501 | ||||||||||||||||||||||||

| Acquisition related deposits | — | — | — | — | 1,250 | ||||||||||||||||||||||||

Assets associated with real estate held for sale, net(2)

|

6,282 | 18,386 | — | — | — | ||||||||||||||||||||||||

| Total Assets | $ | 13,079,612 | $ | 13,085,857 | $ | 12,648,218 | $ | 12,420,302 | $ | 12,368,192 | |||||||||||||||||||

| LIABILITIES & EQUITY | |||||||||||||||||||||||||||||

| Liabilities | |||||||||||||||||||||||||||||

| Notes payable | $ | 3,347,575 | $ | 3,348,060 | $ | 3,345,962 | $ | 3,350,190 | $ | 3,348,697 | |||||||||||||||||||

| Interest rate swap liability | 667 | — | — | 295 | — | ||||||||||||||||||||||||

| Accounts payable, accrued expenses and other liabilities | 124,814 | 141,999 | 149,707 | 169,084 | 153,993 | ||||||||||||||||||||||||

| Dividends and distributions payable | 105,594 | 105,285 | 97,823 | 95,288 | 94,582 | ||||||||||||||||||||||||

Acquired lease intangible liabilities, net(3)

|

129,683 | 136,661 | 147,473 | 155,328 | 163,109 | ||||||||||||||||||||||||

| Tenant security deposits | 90,757 | 90,050 | 90,698 | 91,983 | 91,162 | ||||||||||||||||||||||||

Tenant prepaid rents |

85,494 | 88,822 | 90,576 | 93,218 | 101,473 | ||||||||||||||||||||||||

Liabilities associated with real estate held for sale(2)

|

4 | 234 | — | — | — | ||||||||||||||||||||||||

| Total Liabilities | 3,884,588 | 3,911,111 | 3,922,239 | 3,955,386 | 3,953,016 | ||||||||||||||||||||||||

| Equity | |||||||||||||||||||||||||||||

| Series B preferred stock, net ($75,000 liquidation preference) | 72,443 | 72,443 | 72,443 | 72,443 | 72,443 | ||||||||||||||||||||||||

| Series C preferred stock, net ($86,250 liquidation preference) | 83,233 | 83,233 | 83,233 | 83,233 | 83,233 | ||||||||||||||||||||||||

| Preferred stock | 155,676 | 155,676 | 155,676 | 155,676 | 155,676 | ||||||||||||||||||||||||

| Common stock | 2,367 | 2,362 | 2,253 | 2,195 | 2,178 | ||||||||||||||||||||||||

| Additional paid in capital | 9,140,264 | 9,116,069 | 8,601,276 | 8,318,979 | 8,235,484 | ||||||||||||||||||||||||

| Cumulative distributions in excess of earnings | (462,309) | (474,550) | (441,881) | (407,695) | (381,507) | ||||||||||||||||||||||||

| Accumulated other comprehensive income (loss) | 1,092 | 3,582 | 6,746 | 1,474 | 13,834 | ||||||||||||||||||||||||

| Total stockholders’ equity | 8,837,090 | 8,803,139 | 8,324,070 | 8,070,629 | 8,025,665 | ||||||||||||||||||||||||

| Noncontrolling interests | 357,934 | 371,607 | 401,909 | 394,287 | 389,511 | ||||||||||||||||||||||||

| Total Equity | 9,195,024 | 9,174,746 | 8,725,979 | 8,464,916 | 8,415,176 | ||||||||||||||||||||||||

| Total Liabilities and Equity | $ | 13,079,612 | $ | 13,085,857 | $ | 12,648,218 | $ | 12,420,302 | $ | 12,368,192 | |||||||||||||||||||

(1)Includes net above-market tenant lease intangibles of $24,994 (Jun 30, 2025), $27,043 (Mar 31, 2025), $29,530 (Dec 31, 2024), $30,435 (Sep 30, 2024) and $32,936 (Jun 30, 2024), and a net below-market ground lease intangible of $12,436 (Jun 30, 2025), $12,477 (Mar 31, 2025), $12,518 (Dec 31, 2024), $12,559 (Sep 30, 2024) and $12,600 (Jun 30, 2024).

(2)As of June 30, 2025, our property located at 1332 & 1336 Rocky Point was classified as held for sale.

(3)Represents net below-market tenant lease intangibles as of the balance sheet date.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 9

|

|

||||||

Consolidated Statements of Operations.

|

||||||||

| Quarterly Results | (unaudited and in thousands, except share and per share data) | |||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 | Sep 30, 2024 | Jun 30, 2024 | |||||||||||||||||||||||||

| Revenues | |||||||||||||||||||||||||||||

Rental income(1)

|

$ | 241,568 | $ | 248,821 | $ | 239,737 | $ | 238,396 | $ | 232,973 | |||||||||||||||||||

| Management and leasing services | 132 | 142 | 167 | 156 | 156 | ||||||||||||||||||||||||

| Interest income | 7,807 | 3,324 | 2,991 | 3,291 | 4,444 | ||||||||||||||||||||||||

| Total Revenues | 249,507 | 252,287 | 242,895 | 241,843 | 237,573 | ||||||||||||||||||||||||

| Operating Expenses | |||||||||||||||||||||||||||||

| Property expenses | 55,298 | 55,261 | 56,006 | 54,867 | 51,905 | ||||||||||||||||||||||||

| General and administrative | 19,752 | 19,868 | 21,940 | 20,926 | 19,307 | ||||||||||||||||||||||||

| Depreciation and amortization | 71,188 | 86,740 | 71,832 | 69,241 | 67,896 | ||||||||||||||||||||||||

| Total Operating Expenses | 146,238 | 161,869 | 149,778 | 145,034 | 139,108 | ||||||||||||||||||||||||

| Other Expenses | |||||||||||||||||||||||||||||

| Other expenses | 244 | 2,239 | 34 | 492 | 304 | ||||||||||||||||||||||||

| Interest expense | 26,701 | 27,288 | 28,173 | 27,340 | 28,412 | ||||||||||||||||||||||||

| Total Expenses | 173,183 | 191,396 | 177,985 | 172,866 | 167,824 | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | (291) | — | — | — | — | ||||||||||||||||||||||||

| Gains on sale of real estate | 44,361 | 13,157 | — | 1,745 | 16,268 | ||||||||||||||||||||||||

| Net Income | 120,394 | 74,048 | 64,910 | 70,722 | 86,017 | ||||||||||||||||||||||||

| Less: net income attributable to noncontrolling interests | (4,060) | (2,849) | (2,725) | (2,952) | (3,541) | ||||||||||||||||||||||||

| Net income attributable to Rexford Industrial Realty, Inc. | 116,334 | 71,199 | 62,185 | 67,770 | 82,476 | ||||||||||||||||||||||||

| Less: preferred stock dividends | (2,315) | (2,314) | (2,315) | (2,314) | (2,315) | ||||||||||||||||||||||||

| Less: earnings allocated to participating securities | (592) | (539) | (457) | (395) | (409) | ||||||||||||||||||||||||

| Net income attributable to common stockholders | $ | 113,427 | $ | 68,346 | $ | 59,413 | $ | 65,061 | $ | 79,752 | |||||||||||||||||||

| Earnings per Common Share | |||||||||||||||||||||||||||||

| Net income attributable to common stockholders per share - basic | $ | 0.48 | $ | 0.30 | $ | 0.27 | $ | 0.30 | $ | 0.37 | |||||||||||||||||||

| Net income attributable to common stockholders per share - diluted | $ | 0.48 | $ | 0.30 | $ | 0.27 | $ | 0.30 | $ | 0.37 | |||||||||||||||||||

| Weighted average shares outstanding - basic | 236,098,831 | 227,395,984 | 222,516,006 | 218,759,979 | 217,388,908 | ||||||||||||||||||||||||

| Weighted average shares outstanding - diluted | 236,098,831 | 227,395,984 | 222,856,120 | 219,133,037 | 217,388,908 | ||||||||||||||||||||||||

(1)We elected the “non-separation practical expedient” in ASC 842, which allows us to avoid separating lease and non-lease rental income. As a result of this election, all rental income earned pursuant to tenant leases, including tenant reimbursements, is reflected as one line, “Rental income,” in the consolidated statements of operations. Under the section “Rental Income” on page 37 in the definitions section of this report, we include a presentation of rental revenues, tenant reimbursements and other income for all periods because we believe this information is frequently used by management, investors, securities analysts and other interested parties to evaluate our performance.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 10

|

|

||||||

Consolidated Statements of Operations.

|

||||||||

| Quarterly Results (continued) | (unaudited and in thousands, except share and per share data) | |||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | ||||||||||||||||||||

| Revenues | |||||||||||||||||||||||

| Rental income | $ | 241,568 | $ | 232,973 | $ | 490,389 | $ | 443,963 | |||||||||||||||

| Management and leasing services | 132 | 156 | 274 | 288 | |||||||||||||||||||

| Interest income | 7,807 | 4,444 | 11,131 | 7,418 | |||||||||||||||||||

| Total Revenues | 249,507 | 237,573 | 501,794 | 451,669 | |||||||||||||||||||

| Operating Expenses | |||||||||||||||||||||||

| Property expenses | 55,298 | 51,905 | 110,559 | 99,387 | |||||||||||||||||||

| General and administrative | 19,752 | 19,307 | 39,620 | 39,287 | |||||||||||||||||||

| Depreciation and amortization | 71,188 | 67,896 | 157,928 | 134,174 | |||||||||||||||||||

| Total Operating Expenses | 146,238 | 139,108 | 308,107 | 272,848 | |||||||||||||||||||

| Other Expenses | |||||||||||||||||||||||

| Other expenses | 244 | 304 | 2,483 | 1,712 | |||||||||||||||||||

| Interest expense | 26,701 | 28,412 | 53,989 | 43,083 | |||||||||||||||||||

| Total Expenses | 173,183 | 167,824 | 364,579 | 317,643 | |||||||||||||||||||

Debt extinguishment and modification expenses |

(291) | — | (291) | — | |||||||||||||||||||

| Gains on sale of real estate | 44,361 | 16,268 | 57,518 | 16,268 | |||||||||||||||||||

| Net Income | 120,394 | 86,017 | 194,442 | 150,294 | |||||||||||||||||||

| Less: net income attributable to noncontrolling interests | (4,060) | (3,541) | (6,909) | (6,447) | |||||||||||||||||||

| Net income attributable to Rexford Industrial Realty, Inc. | 116,334 | 82,476 | 187,533 | 143,847 | |||||||||||||||||||

| Less: preferred stock dividends | (2,315) | (2,315) | (4,629) | (4,629) | |||||||||||||||||||

| Less: earnings allocated to participating securities | (592) | (409) | (1,131) | (827) | |||||||||||||||||||

| Net income attributable to common stockholders | $ | 113,427 | $ | 79,752 | $ | 181,773 | $ | 138,391 | |||||||||||||||

| Net income attributable to common stockholders per share – basic | $ | 0.48 | $ | 0.37 | $ | 0.78 | $ | 0.64 | |||||||||||||||

| Net income attributable to common stockholders per share – diluted | $ | 0.48 | $ | 0.37 | $ | 0.78 | $ | 0.64 | |||||||||||||||

| Weighted-average shares of common stock outstanding – basic | 236,098,831 | 217,388,908 | 231,771,448 | 215,895,285 | |||||||||||||||||||

| Weighted-average shares of common stock outstanding – diluted | 236,098,831 | 217,388,908 | 231,771,448 | 215,913,411 | |||||||||||||||||||

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 11

|

|

||||||

|

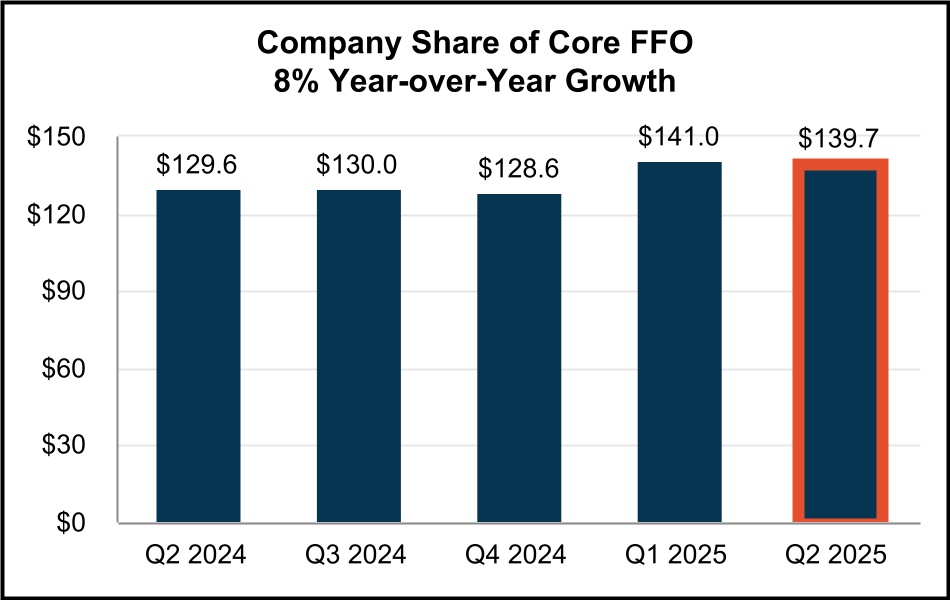

Non-GAAP FFO and Core FFO Reconciliations.(1)

|

||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| June 30, 2025 | March 31, 2025 | December 31, 2024 | September 30, 2024 | June 30, 2024 | |||||||||||||||||||||||||

| Net Income | $ | 120,394 | $ | 74,048 | $ | 64,910 | $ | 70,722 | $ | 86,017 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Depreciation and amortization | 71,188 | 86,740 | 71,832 | 69,241 | 67,896 | ||||||||||||||||||||||||

| Gains on sale of real estate | (44,361) | (13,157) | — | (1,745) | (16,268) | ||||||||||||||||||||||||

NAREIT Defined Funds From Operations (FFO)

|

147,221 | 147,631 | 136,742 | 138,218 | 137,645 | ||||||||||||||||||||||||

| Less: preferred stock dividends | (2,315) | (2,314) | (2,315) | (2,314) | (2,315) | ||||||||||||||||||||||||

Less: FFO attributable to noncontrolling interests(2)

|

(4,962) | (5,394) | (5,283) | (5,389) | (5,410) | ||||||||||||||||||||||||

Less: FFO attributable to participating securities(3)

|

(728) | (750) | (624) | (566) | (582) | ||||||||||||||||||||||||

| Company share of FFO | $ | 139,216 | $ | 139,173 | $ | 128,520 | $ | 129,949 | $ | 129,338 | |||||||||||||||||||

| Company share of FFO per common share‐basic | $ | 0.59 | $ | 0.61 | $ | 0.58 | $ | 0.59 | $ | 0.59 | |||||||||||||||||||

| Company share of FFO per common share‐diluted | $ | 0.59 | $ | 0.61 | $ | 0.58 | $ | 0.59 | $ | 0.59 | |||||||||||||||||||

| FFO | $ | 147,221 | $ | 147,631 | $ | 136,742 | $ | 138,218 | $ | 137,645 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Acquisition expenses | 23 | 79 | 9 | 6 | 58 | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | 291 | — | — | — | — | ||||||||||||||||||||||||

| Amortization of loss on termination of interest rate swaps | — | — | 34 | 59 | 59 | ||||||||||||||||||||||||

| Non-capitalizable demolition costs | — | 365 | — | — | 129 | ||||||||||||||||||||||||

Severance costs associated with workforce reduction(4)

|

199 | 1,483 | — | — | — | ||||||||||||||||||||||||

| Core FFO | 147,734 | 149,558 | 136,785 | 138,283 | 137,891 | ||||||||||||||||||||||||

| Less: preferred stock dividends | (2,315) | (2,314) | (2,315) | (2,314) | (2,315) | ||||||||||||||||||||||||

Less: Core FFO attributable to noncontrolling interests(2)

|

(4,979) | (5,461) | (5,284) | (5,391) | (5,418) | ||||||||||||||||||||||||

Less: Core FFO attributable to participating securities(3)

|

(731) | (760) | (624) | (567) | (583) | ||||||||||||||||||||||||

| Company share of Core FFO | $ | 139,709 | $ | 141,023 | $ | 128,562 | $ | 130,011 | $ | 129,575 | |||||||||||||||||||

| Company share of Core FFO per common share‐basic | $ | 0.59 | $ | 0.62 | $ | 0.58 | $ | 0.59 | $ | 0.60 | |||||||||||||||||||

| Company share of Core FFO per common share‐diluted | $ | 0.59 | $ | 0.62 | $ | 0.58 | $ | 0.59 | $ | 0.60 | |||||||||||||||||||

| Weighted-average shares outstanding-basic | 236,098,831 | 227,395,984 | 222,516,006 | 218,759,979 | 217,388,908 | ||||||||||||||||||||||||

Weighted-average shares outstanding-diluted(5)

|

236,098,831 | 227,395,984 | 222,856,120 | 219,133,037 | 217,388,908 | ||||||||||||||||||||||||

(1)For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 34 of this report.

(2)Noncontrolling interests relate to interests in the Company’s operating partnership, represented by common units and preferred units (Series 1, Series 2 and Series 3 CPOP units) of partnership interests in the operating partnership that are owned by unit holders other than the Company. On April 10, 2024, we exercised our conversion right to convert all Series 1 CPOP units into OP units. On March 6, 2025, we exercised our conversion right to convert all remaining Series 2 CPOP units into OP Units.

(3)Participating securities include unvested shares of restricted stock, unvested LTIP units and unvested performance units.

(4)Amounts are included in the line item “Other expenses” in the consolidated statements of operations.

(5)Weighted-average shares outstanding-diluted includes adjustments for unvested performance units and shares issuable under forward equity sales agreements if the effect is dilutive for the reported period.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 12

|

|

||||||

Non-GAAP FFO and Core FFO Reconciliations.(1)

|

||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | |||||||||||||||||||||||

| Net Income | $ | 120,394 | $ | 86,017 | $ | 194,442 | $ | 150,294 | ||||||||||||||||||

| Adjustments: | ||||||||||||||||||||||||||

| Depreciation and amortization | 71,188 | 67,896 | 157,928 | 134,174 | ||||||||||||||||||||||

| Gains on sale of real estate | (44,361) | (16,268) | (57,518) | (16,268) | ||||||||||||||||||||||

| Funds From Operations (FFO) | 147,221 | 137,645 | 294,852 | 268,200 | ||||||||||||||||||||||

| Less: preferred stock dividends | (2,315) | (2,315) | (4,629) | (4,629) | ||||||||||||||||||||||

| Less: FFO attributable to noncontrolling interests | (4,962) | (5,410) | (10,356) | (10,598) | ||||||||||||||||||||||

| Less: FFO attributable to participating securities | (728) | (582) | (1,478) | (1,152) | ||||||||||||||||||||||

| Company share of FFO | $ | 139,216 | $ | 129,338 | $ | 278,389 | $ | 251,821 | ||||||||||||||||||

| Company share of FFO per common share‐basic | $ | 0.59 | $ | 0.59 | $ | 1.20 | $ | 1.17 | ||||||||||||||||||

| Company share of FFO per common share‐diluted | $ | 0.59 | $ | 0.59 | $ | 1.20 | $ | 1.17 | ||||||||||||||||||

| FFO | $ | 147,221 | $ | 137,645 | $ | 294,852 | $ | 268,200 | ||||||||||||||||||

| Adjustments: | ||||||||||||||||||||||||||

| Acquisition expenses | 23 | 58 | 102 | 108 | ||||||||||||||||||||||

| Debt extinguishment and modification expenses | 291 | — | 291 | — | ||||||||||||||||||||||

| Amortization of loss on termination of interest rate swaps | — | 59 | — | 118 | ||||||||||||||||||||||

| Non-capitalizable demolition costs | — | 129 | 365 | 1,127 | ||||||||||||||||||||||

Severance costs associated with workforce reduction(2)

|

199 | — | 1,682 | — | ||||||||||||||||||||||

| Core FFO | 147,734 | 137,891 | 297,292 | 269,553 | ||||||||||||||||||||||

| Less: preferred stock dividends | (2,315) | (2,315) | (4,629) | (4,629) | ||||||||||||||||||||||

| Less: Core FFO attributable to noncontrolling interests | (4,979) | (5,418) | (10,440) | (10,644) | ||||||||||||||||||||||

| Less: Core FFO attributable to participating securities | (731) | (583) | (1,491) | (1,158) | ||||||||||||||||||||||

| Company share of Core FFO | $ | 139,709 | $ | 129,575 | $ | 280,732 | $ | 253,122 | ||||||||||||||||||

| Company share of Core FFO per common share‐basic | $ | 0.59 | $ | 0.60 | $ | 1.21 | $ | 1.17 | ||||||||||||||||||

| Company share of Core FFO per common share‐diluted | $ | 0.59 | $ | 0.60 | $ | 1.21 | $ | 1.17 | ||||||||||||||||||

| Weighted-average shares outstanding-basic | 236,098,831 | 217,388,908 | 231,771,448 | 215,895,285 | ||||||||||||||||||||||

| Weighted-average shares outstanding-diluted | 236,098,831 | 217,388,908 | 231,771,448 | 215,913,411 | ||||||||||||||||||||||

(1)For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 34 of this report.

(2)Amounts are included in the line item “Other expenses” in the consolidated statements of operations.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 13

|

|

||||||

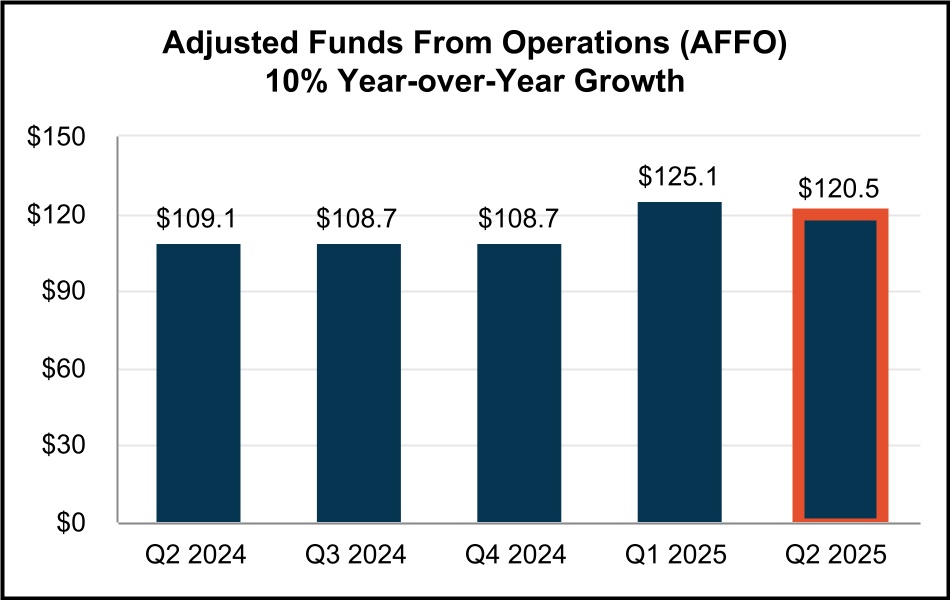

Non-GAAP AFFO Reconciliation.(1)

|

||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| June 30, 2025 |

March 31, 2025 |

December 31, 2024 |

September 30, 2024 |

June 30, 2024 |

|||||||||||||||||||||||||

Funds From Operations(2)

|

$ | 147,221 | $ | 147,631 | $ | 136,742 | $ | 138,218 | $ | 137,645 | |||||||||||||||||||

| Adjustments: | |||||||||||||||||||||||||||||

| Amortization of deferred financing costs | 1,255 | 1,134 | 1,246 | 1,252 | 1,266 | ||||||||||||||||||||||||

| Non-cash stock compensation | 10,091 | 9,699 | 11,539 | 9,918 | 11,057 | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | 291 | — | — | — | — | ||||||||||||||||||||||||

| Amortization related to termination/settlement of interest rate derivatives | 76 | 77 | 112 | 136 | 137 | ||||||||||||||||||||||||

| Note payable (discount) premium amortization, net | 1,579 | 1,560 | 1,534 | 1,511 | 1,491 | ||||||||||||||||||||||||

| Non-capitalizable demolition costs | — | 365 | — | — | 129 | ||||||||||||||||||||||||

| Severance costs associated with workforce reduction | 199 | 1,483 | — | — | — | ||||||||||||||||||||||||

| Deduct: | |||||||||||||||||||||||||||||

| Preferred stock dividends | (2,315) | (2,314) | (2,315) | (2,314) | (2,315) | ||||||||||||||||||||||||

Straight line rental revenue adjustment(3)

|

(6,918) | (5,517) | (10,057) | (11,441) | (9,567) | ||||||||||||||||||||||||

| Above/(below) market lease revenue adjustments | (5,788) | (9,186) | (6,159) | (6,635) | (7,268) | ||||||||||||||||||||||||

Capitalized payments(4)

|

(14,368) | (13,321) | (12,102) | (13,900) | (12,280) | ||||||||||||||||||||||||

| Accretion of net loan origination fees | (115) | (115) | (115) | (115) | (115) | ||||||||||||||||||||||||

Recurring capital expenditures(5)

|

(5,887) | (1,311) | (7,882) | (5,254) | (3,502) | ||||||||||||||||||||||||

2nd generation tenant improvements(6)

|

(663) | (162) | (296) | (18) | (123) | ||||||||||||||||||||||||

2nd generation leasing commissions(7)

|

(4,162) | (4,879) | (3,520) | (2,660) | (7,436) | ||||||||||||||||||||||||

| Adjusted Funds From Operations (AFFO) | $ | 120,496 | $ | 125,144 | $ | 108,727 | $ | 108,698 | $ | 109,119 | |||||||||||||||||||

(1)For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 34 of this report.

(2)A quarterly reconciliation of net income to Funds From Operations is set forth on page 12 of this report.

(3)The straight line rental revenue adjustment includes concessions of $5,844, $7,035, $8,504, $7,600 and $4,586 for the three months ended June 30, 2025, March 31, 2025, December 31, 2024, September 30, 2024 and June 30, 2024, respectively.

(4)Includes capitalized interest, taxes, insurance and construction-related compensation costs.

(5)Excludes nonrecurring capital expenditures of $65,376, $43,361, 67,594, 94,436 and $89,120 for the three months ended June 30, 2025, March 31, 2025, December 31, 2024, September 30, 2024 and June 30, 2024, respectively.

(6)Excludes 1st generation tenant improvements of $292, $798, $189, $470 and $681 for the three months ended June 30, 2025, March 31, 2025, December 31, 2024, September 30, 2024 and June 30, 2024, respectively.

(7)Excludes 1st generation leasing commissions of $1,879, $3,058, $290, $2,776 and $3,921 for the three months ended June 30, 2025, March 31, 2025, December 31, 2024, September 30, 2024 and June 30, 2024, respectively.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 14

|

|

||||||

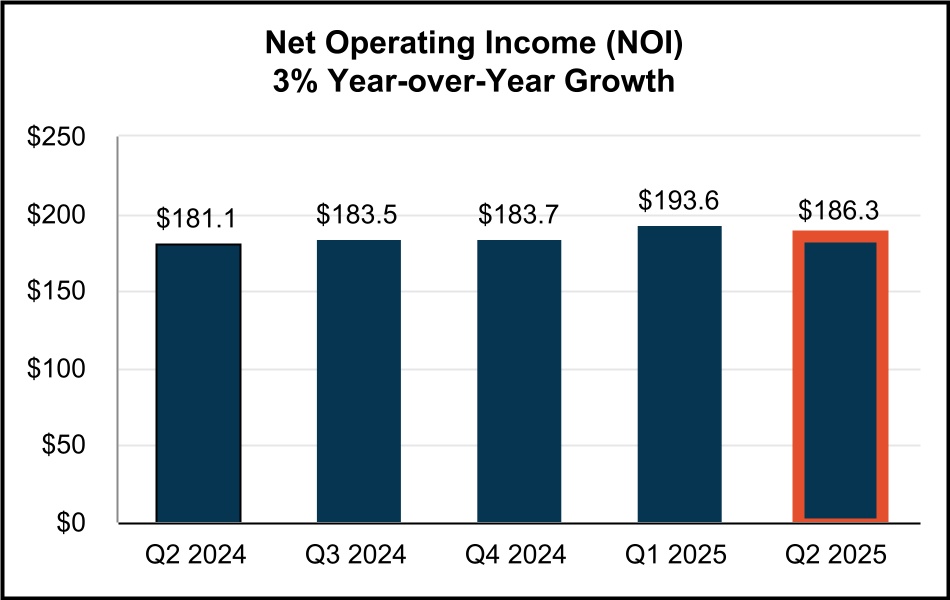

Statement of Operations Reconciliations - NOI, Cash NOI, EBITDAre and Adjusted EBITDAre.(1)

| ||||||||

| (unaudited and in thousands) | ||||||||

| NOI and Cash NOI | |||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 | Sep 30, 2024 | Jun 30, 2024 | |||||||||||||||||||||||||

Rental income(2)(3)(4)

|

$ | 241,568 | $ | 248,821 | $ | 239,737 | $ | 238,396 | $ | 232,973 | |||||||||||||||||||

| Less: Property expenses | 55,298 | 55,261 | 56,006 | 54,867 | 51,905 | ||||||||||||||||||||||||

| Net Operating Income (NOI) | $ | 186,270 | $ | 193,560 | $ | 183,731 | $ | 183,529 | $ | 181,068 | |||||||||||||||||||

Above/(below) market lease revenue adjustments |

(5,788) | (9,186) | (6,159) | (6,635) | (7,268) | ||||||||||||||||||||||||

| Straight line rental revenue adjustment | (6,918) | (5,517) | (10,057) | (11,441) | (9,567) | ||||||||||||||||||||||||

| Cash NOI | $ | 173,564 | $ | 178,857 | $ | 167,515 | $ | 165,453 | $ | 164,233 | |||||||||||||||||||

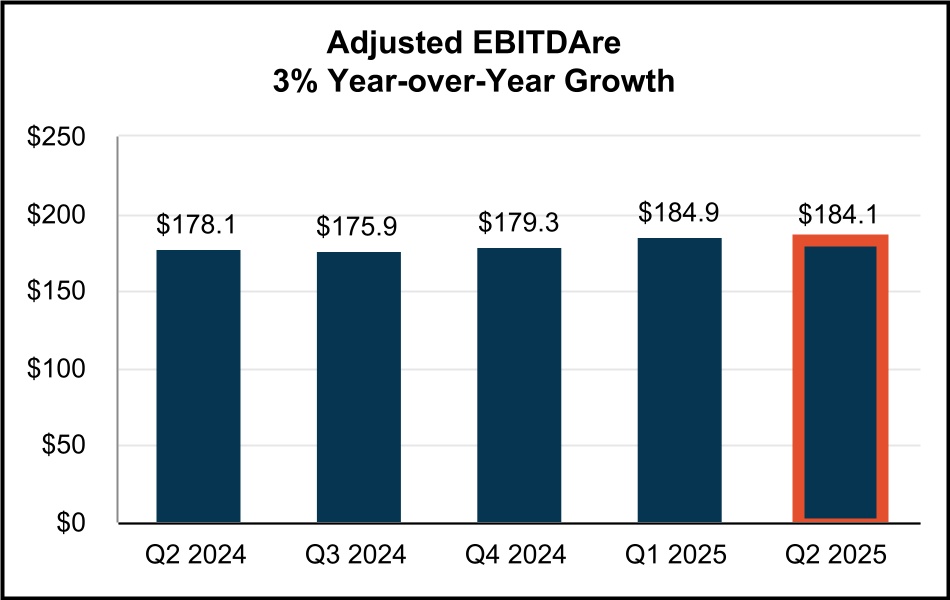

EBITDAre and Adjusted EBITDAre

|

|||||||||||||||||||||||||||||

| Three Months Ended | |||||||||||||||||||||||||||||

| Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 | Sep 30, 2024 | Jun 30, 2024 | |||||||||||||||||||||||||

| Net income | $ | 120,394 | $ | 74,048 | $ | 64,910 | $ | 70,722 | $ | 86,017 | |||||||||||||||||||

| Interest expense | 26,701 | 27,288 | 28,173 | 27,340 | 28,412 | ||||||||||||||||||||||||

| Depreciation and amortization | 71,188 | 86,740 | 71,832 | 69,241 | 67,896 | ||||||||||||||||||||||||

| Gains on sale of real estate | (44,361) | (13,157) | — | (1,745) | (16,268) | ||||||||||||||||||||||||

EBITDAre

|

$ | 173,922 | $ | 174,919 | $ | 164,915 | $ | 165,558 | $ | 166,057 | |||||||||||||||||||

| Stock-based compensation amortization | 10,091 | 9,699 | 11,539 | 9,918 | 11,057 | ||||||||||||||||||||||||

| Debt extinguishment and modification expenses | 291 | — | — | — | — | ||||||||||||||||||||||||

| Acquisition expenses | 23 | 79 | 9 | 6 | 58 | ||||||||||||||||||||||||

Pro forma effect of acquisitions(5)

|

— | — | 2,884 | 426 | 1,058 | ||||||||||||||||||||||||

Pro forma effect of dispositions(6)

|

(216) | 162 | — | 21 | (124) | ||||||||||||||||||||||||

Adjusted EBITDAre

|

$ | 184,111 | $ | 184,859 | $ | 179,347 | $ | 175,929 | $ | 178,106 | |||||||||||||||||||

(1)For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 34 of this report.

(2)See footnote (1) on page 10 for details related to our presentation of “Rental income” in the consolidated statements of operations for all periods presented.

(3)Reflects (decrease) increase to rental income due to changes in the Company’s assessment of lease payment collectability as follows (in thousands): $(141), $(2,303), $(200), $(730) and $(804) for the three months ended June 30, 2025, March 31, 2025, December 31, 2024, September 30, 2024 and June 30, 2024, respectively.

(4)Rental income includes net lease termination income (in thousands) of $0, $8,935, $614, $0 and $103 for the three months ended June 30, 2025, March 31, 2025, December 31, 2024, September 30, 2024 and June 30, 2024, respectively. Amounts include lease termination fees and write-offs of straight-line rent and above/(below) market lease intangibles associated with lease terminations.

(5)Represents the estimated impact on Q4'24 EBITDAre of Q4'24 acquisitions as if they had been acquired on October 1, 2024, the impact on Q3'24 EBITDAre of Q3'24 acquisitions as if they had been acquired on July 1, 2024 and the impact on Q2'24 EBITDAre of Q2'24 acquisitions as if they had been acquired on April 1, 2024. We have made a number of assumptions in such estimates and there can be no assurance that we would have generated the projected levels of EBITDAre had we acquired these as of the beginning of each period.

(6)Represents the estimated impact on Q2'25 EBITDAre of Q2'25 dispositions as if they had been sold as of April 1, 2025, the impact on Q1'25 EBITDAre of Q1'25 dispositions as if they had been sold as of January 1, 2025, the impact on Q3'24 EBITDAre of Q3'24 dispositions as if they had been sold as of July 1, 2024 and the impact on Q2'24 EBITDAre of Q2'24 dispositions as if they had been sold as of April 1, 2024.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 15

|

|

||||||

Same Property Portfolio Performance.(1)

|

||||||||

| (unaudited and dollars in thousands) | ||||||||

| Same Property Portfolio: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Number of properties | 289 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Square Feet | 37,991,248 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Same Property Portfolio NOI and Cash NOI: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||||||||||||||||||||||||||||||

| 2025 | 2024 | $ Change | % Change | 2025 | 2024 | $ Change | % Change | |||||||||||||||||||||||||||||||||||||||||||

Rental income(2)(3)(4)

|

$ | 191,653 | $ | 188,183 | $ | 3,470 | 1.8% | $ | 380,012 | $ | 374,370 | $ | 5,642 | 1.5% | ||||||||||||||||||||||||||||||||||||

| Property expenses | 42,060 | 40,242 | 1,818 | 4.5% | 83,534 | 80,500 | 3,034 | 3.8% | ||||||||||||||||||||||||||||||||||||||||||

| Same Property Portfolio NOI | $ | 149,593 | $ | 147,941 | $ | 1,652 | 1.1% | (4) |

$ | 296,478 | $ | 293,870 | $ | 2,608 | 0.9% | (4) |

||||||||||||||||||||||||||||||||||

Straight-line rental revenue adjustment |

(4,804) | (7,503) | 2,699 | (36.0)% | (7,959) | (14,758) | 6,799 | (46.1)% | ||||||||||||||||||||||||||||||||||||||||||

Above/(below) market lease revenue adjustments |

(5,129) | (6,034) | 905 | (15.0)% | (10,001) | (12,471) | 2,470 | (19.8)% | ||||||||||||||||||||||||||||||||||||||||||

| Same Property Portfolio Cash NOI | $ | 139,660 | $ | 134,404 | $ | 5,256 | 3.9% | (4) |

$ | 278,518 | $ | 266,641 | $ | 11,877 | 4.5% | (4) |

||||||||||||||||||||||||||||||||||

| Same Property Portfolio Occupancy: | |||||||||||||||||||||||||||||

| Three Months Ended June 30, | |||||||||||||||||||||||||||||

| 2025 | 2024 | Year-over-Year Change (basis points) |

Three Months Ended March 31, 2025(5)

|

Sequential Change (basis points) |

|||||||||||||||||||||||||

Quarterly Weighted Average Occupancy:(5)

|

|||||||||||||||||||||||||||||

| Los Angeles County | 95.6% | 97.1% | (150) bps | 95.6% | — bps | ||||||||||||||||||||||||

| Orange County | 99.0% | 99.7% | (70) bps | 99.1% | (10) bps | ||||||||||||||||||||||||

| Riverside / San Bernardino County | 96.6% | 96.7% | (10) bps | 96.7% | (10) bps | ||||||||||||||||||||||||

| San Diego County | 96.1% | 96.0% | 10 bps | 96.1% | — bps | ||||||||||||||||||||||||

| Ventura County | 91.4% | 94.4% | (300) bps | 91.4% | — bps | ||||||||||||||||||||||||

| Quarterly Weighted Average Occupancy | 95.9% | 97.0% | (110) bps | 95.9% | — bps | ||||||||||||||||||||||||

| Ending Occupancy: | 96.1% | 97.4% | (130) bps | 95.7% | 40 bps | ||||||||||||||||||||||||

(1)For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 34 of this report.

(2)See “Same Property Portfolio Rental Income” on page 37 of the definitions section of this report for a breakdown of rental income into rental revenues, tenant reimbursements and other income for the three and six months ended June 30, 2025 and 2024.

(3)Reflects (decrease) increase to rental income due to changes in the Company’s assessment of lease payment collectability as follows: $(65) thousand and $(571) thousand for the three months ended June 30, 2025 and 2024, respectively, and $(2,372) thousand and $(1,976) thousand for the six months ended June 30, 2025 and 2024.

(4)Rental income includes lease termination fees of $0 thousand and $122 thousand for the three months ended June 30, 2025 and 2024, respectively, and $20 thousand and $131 thousand for the six months ended June 30, 2025 and 2024, respectively. Excluding these lease termination fees, Same Property Portfolio NOI increased by approximately 1.2% and 0.9% and Same Property Portfolio Cash NOI increased by approximately 4.0% and 4.5% during the three and six months ended June 30, 2025, compared to the three and six months ended June 30, 2024, respectively.

(5)Calculated by averaging the occupancy rate at the end of each month in 2Q-2025 and March 2025 (for 2Q-2025), the end of each month in 2Q-2024 and March 2024 (for 2Q-2024) and the end of each month in 1Q-2025 and December 2024 (for 1Q-2025).

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 16

|

|

||||||

Capitalization Summary.

|

||||||||

| (unaudited and in thousands, except share and per share data) | ||||||||

| Capitalization as of June 30, 2025 | ||||||||

| Description | June 30, 2025 | March 31, 2025 | December 31, 2024 | September 30, 2024 | June 30, 2024 | ||||||||||||||||||||||||

Common shares outstanding(1)

|

236,151,829 | 235,610,472 | 224,868,888 | 219,102,342 | 217,404,848 | ||||||||||||||||||||||||

Operating partnership units outstanding(2)

|

8,182,445 | 8,700,301 | 8,426,905 | 8,175,868 | 8,218,426 | ||||||||||||||||||||||||

| Total shares and units outstanding at period end | 244,334,274 | 244,310,773 | 233,295,793 | 227,278,210 | 225,623,274 | ||||||||||||||||||||||||

| Share price at end of quarter | $ | 35.57 | $ | 39.15 | $ | 38.66 | $ | 50.31 | $ | 44.59 | |||||||||||||||||||

| Common Stock and Operating Partnership Units - Capitalization | $ | 8,690,970 | $ | 9,564,767 | $ | 9,019,215 | $ | 11,434,367 | $ | 10,060,542 | |||||||||||||||||||

Series B and C Cumulative Redeemable Preferred Stock(3)

|

$ | 161,250 | $ | 161,250 | $ | 161,250 | $ | 161,250 | $ | 161,250 | |||||||||||||||||||

4.00% Series 2 Cumulative Redeemable Convertible Preferred Units(4)

|

— | — | 40,706 | 40,706 | 40,750 | ||||||||||||||||||||||||

3.00% Series 3 Cumulative Redeemable Convertible Preferred Units(4)

|

12,000 | 12,000 | 12,000 | 12,000 | 12,000 | ||||||||||||||||||||||||

| Preferred Equity | $ | 173,250 | $ | 173,250 | $ | 213,956 | $ | 213,956 | $ | 214,000 | |||||||||||||||||||

| Total Equity Market Capitalization | $ | 8,864,220 | $ | 9,738,017 | $ | 9,233,171 | $ | 11,648,323 | $ | 10,274,542 | |||||||||||||||||||

| Total Debt | $ | 3,379,141 | $ | 3,379,383 | $ | 3,379,622 | $ | 3,386,273 | $ | 3,386,559 | |||||||||||||||||||

| Less: Cash and cash equivalents | (431,117) | (504,579) | (55,971) | (61,836) | (125,710) | ||||||||||||||||||||||||

| Net Debt | $ | 2,948,024 | $ | 2,874,804 | $ | 3,323,651 | $ | 3,324,437 | $ | 3,260,849 | |||||||||||||||||||

| Total Combined Market Capitalization (Net Debt plus Equity) | $ | 11,812,244 | $ | 12,612,821 | $ | 12,556,822 | $ | 14,972,760 | $ | 13,535,391 | |||||||||||||||||||

| Net debt to total combined market capitalization | 25.0 | % | 22.8 | % | 26.5 | % | 22.2 | % | 24.1 | % | |||||||||||||||||||

Net debt to Adjusted EBITDAre (quarterly results annualized)(5)

|

4.0x | 3.9x | 4.6x | 4.7x | 4.6x | ||||||||||||||||||||||||

Net debt & preferred equity to Adjusted EBITDAre (quarterly results annualized)(5)

|

4.2x | 4.1x | 4.9x | 5.0x | 4.9x | ||||||||||||||||||||||||

(1)Excludes the following number of shares of unvested restricted stock: 542,922 (Jun 30, 2025), 560,382 (Mar 31, 2025), 416,123 (Dec 31, 2024), 405,003 (Sep 30, 2024) and 435,225 (Jun 30, 2024).

(2)Represents outstanding common units of the Company’s operating partnership (“OP”), Rexford Industrial Realty, LP, that are owned by unitholders other than Rexford Industrial Realty, Inc. Represents the noncontrolling interest in our OP. As of Jun 30, 2025, includes 1,260,083 vested LTIP Units & 1,262,969 vested performance units & excludes 463,555 unvested LTIP Units & 2,278,110 unvested performance units.

(3)Values based on liquidation preference of $25 per share and the following number of outstanding shares of preferred stock: 5.875% Series B (3,000,000); 5.625% Series C (3,450,000).

(4)Value based on 904,583 outstanding Series 2 preferred units at a liquidation preference of $45 per unit and 164,998 outstanding Series 3 preferred units at a liquidation preference of $72.72825 per unit. On March 6, 2025, we exercised our conversion right to convert all remaining 904,583 Series 2 preferred units into OP Units.

(5)For definition/discussion of non-GAAP financial measures and reconciliations to their nearest GAAP equivalents, see the definitions section & reconciliation section beginning on page 34 and page 12 of this report, respectively.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 17

|

|

||||||

Debt Summary.

|

||||||||

| (unaudited and dollars in thousands) | ||||||||

| Debt Detail: | ||||||||||||||||||||||||||

| As of June 30, 2025 | ||||||||||||||||||||||||||

| Debt Description | Maturity Date | Stated Interest Rate |

Effective

Interest Rate(1)

|

Principal

Balance(2)

|

||||||||||||||||||||||

| Unsecured Debt: | ||||||||||||||||||||||||||

$1.25 Billion Revolving Credit Facility(3)

|

5/30/2029(4)

|

SOFR+0.725%(5)

|

5.175% | $ | — | |||||||||||||||||||||

| $100M Senior Notes | 8/6/2025 | 4.290% | 4.290% | 100,000 | ||||||||||||||||||||||

$575M Exchangeable 2027 Senior Notes(6)

|

3/15/2027 | 4.375% | 4.375% | 575,000 | ||||||||||||||||||||||

| $300M Term Loan Facility | 5/26/2027 |

SOFR+0.80%(5)

|

3.717%(7)

|

300,000 | ||||||||||||||||||||||

| $125M Senior Notes | 7/13/2027 | 3.930% | 3.930% | 125,000 | ||||||||||||||||||||||

| $300M Senior Notes | 6/15/2028 | 5.000% | 5.000% | 300,000 | ||||||||||||||||||||||

$575M Exchangeable 2029 Senior Notes(6)

|

3/15/2029 | 4.125% | 4.125% | 575,000 | ||||||||||||||||||||||

| $25M Series 2019A Senior Notes | 7/16/2029 | 3.880% | 3.880% | 25,000 | ||||||||||||||||||||||

| $400M Senior Notes | 12/1/2030 | 2.125% | 2.125% | 400,000 | ||||||||||||||||||||||

| $400M Term Loan Facility | 5/30/2030 |

SOFR+0.80%(5)

|

4.214%(8)

|

400,000 | ||||||||||||||||||||||

| $400M Senior Notes - Green Bond | 9/1/2031 | 2.150% | 2.150% | 400,000 | ||||||||||||||||||||||

| $75M Series 2019B Senior Notes | 7/16/2034 | 4.030% | 4.030% | 75,000 | ||||||||||||||||||||||

| Secured Debt: | ||||||||||||||||||||||||||

| $60M Term Loan Facility |

10/27/2026(9)

|

SOFR+1.250%(9)

|

5.060%(10)

|

60,000 | ||||||||||||||||||||||

| 701-751 Kingshill Place | 1/5/2026 | 3.900% | 3.900% | 6,784 | ||||||||||||||||||||||

| 13943-13955 Balboa Boulevard | 7/1/2027 | 3.930% | 3.930% | 14,015 | ||||||||||||||||||||||

| 2205 126th Street | 12/1/2027 | 3.910% | 3.910% | 5,200 | ||||||||||||||||||||||

| 2410-2420 Santa Fe Avenue | 1/1/2028 | 3.700% | 3.700% | 10,300 | ||||||||||||||||||||||

| 11832-11954 La Cienega Boulevard | 7/1/2028 | 4.260% | 4.260% | 3,731 | ||||||||||||||||||||||

| 1100-1170 Gilbert Street (Gilbert/La Palma) | 3/1/2031 | 5.125% | 5.125% | 1,432 | ||||||||||||||||||||||

| 7817 Woodley Avenue | 8/1/2039 | 4.140% | 4.140% | 2,679 | ||||||||||||||||||||||

| Total Debt | 3.757% | $ | 3,379,141 | |||||||||||||||||||||||

Debt Composition: |

||||||||||||||||||||||||||||||||

| Category | Weighted Average Term Remaining (yrs) |

Stated Interest Rate | Effective Interest Rate | Balance | % of Total | |||||||||||||||||||||||||||

| Fixed | 3.7 | 3.757% (See Table Above) |

3.757% | $ | 3,379,141 | 100% | ||||||||||||||||||||||||||

| Variable | — | — | —% | $ | — | 0% | ||||||||||||||||||||||||||

| Secured | 2.5 | 4.589% | $ | 104,141 | 3% | |||||||||||||||||||||||||||

| Unsecured | 3.7 | 3.731% | $ | 3,275,000 | 97% | |||||||||||||||||||||||||||

*See footnotes on the following page*

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 18

|

|

||||||

Debt Summary (Continued).

|

||||||||

| (unaudited and dollars in thousands) | ||||||||

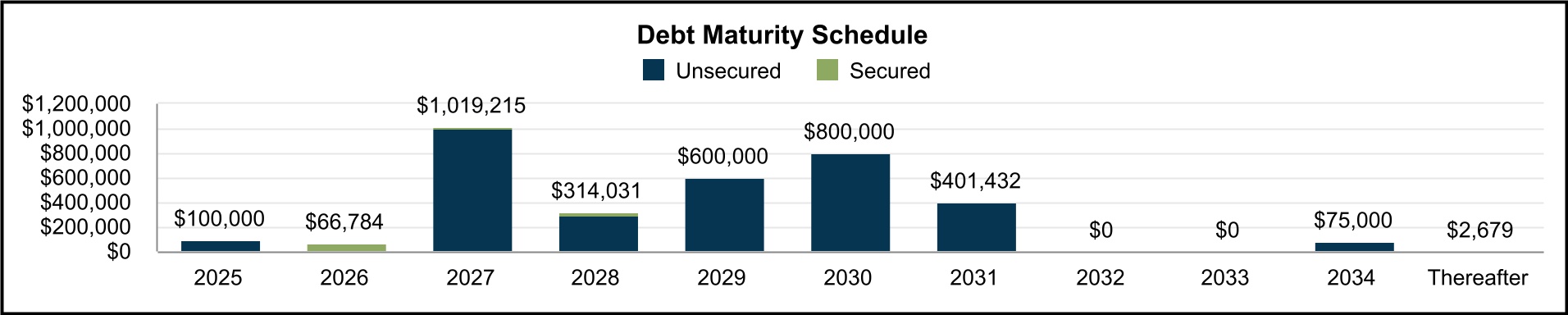

Debt Maturity Schedule(11):

|

||||||||||||||||||||||||||||||||

| Year | Secured |

Unsecured | Total | % Total |

Effective Interest Rate(1)

|

|||||||||||||||||||||||||||

| 2025 | $ | — | $ | 100,000 | $ | 100,000 | 3 | % | 4.290 | % | ||||||||||||||||||||||

| 2026 | 66,784 | — | 66,784 | 2 | % | 4.942 | % | |||||||||||||||||||||||||

| 2027 | 19,215 | 1,000,000 | 1,019,215 | 30 | % | 4.118 | % | |||||||||||||||||||||||||

| 2028 | 14,031 | 300,000 | 314,031 | 9 | % | 4.949 | % | |||||||||||||||||||||||||

| 2029 | — | 600,000 | 600,000 | 18 | % | 4.115 | % | |||||||||||||||||||||||||

| 2030 | — | 800,000 | 800,000 | 24 | % | 3.169 | % | |||||||||||||||||||||||||

| 2031 | 1,432 | 400,000 | 401,432 | 12 | % | 2.161 | % | |||||||||||||||||||||||||

| 2032 | — | — | — | — | % | — | % | |||||||||||||||||||||||||

| 2033 | — | — | — | — | % | — | % | |||||||||||||||||||||||||

| 2034 | — | 75,000 | 75,000 | 2 | % | 4.030 | % | |||||||||||||||||||||||||

| Thereafter | 2,679 | — | 2,679 | 0 | % | 4.140 | % | |||||||||||||||||||||||||

| Total | $ | 104,141 | $ | 3,275,000 | $ | 3,379,141 | 100 | % | 3.757 | % | ||||||||||||||||||||||

(1)Includes the effect of interest rate swaps that were active as of June 30, 2025, including the interest rate swaps with a combined notional value of $400M that were executed on June 30, 2025 with an effective date of July 1, 2025. See notes (6), (8) & (10) below. Excludes the effect of premiums/discounts, deferred loan costs and the credit facility fee.

(2)Excludes unamortized debt issuance costs, premiums and discounts aggregating $31.6 million as of June 30, 2025.

(3)The $1.25B revolving credit facility (the “Revolver”) is subject to a facility fee which is calculated as a percentage of the total commitment amount, regardless of usage. The facility fee ranges from 0.125% to 0.300% depending on our credit ratings. There are also two sustainability-linked pricing components that can periodically change the facility fee by -/+ 0.01% (or zero) depending on our achievement of the annual sustainability performance metric. The sustainability-linked pricing adjustment for the facility fee is currently zero.

(4)The Revolver has two six-month extensions, subject to certain terms and conditions.

(5)The interest rates on these loans are comprised of Daily SOFR for the Revolver and $400M term loan facility and 1M SOFR for the $300M term loan facility (plus a 0.10% SOFR adjustment for the $300M term loan facility), and an applicable margin ranging from 0.725% to 1.40% for the Revolver and 0.80% to 1.60% for the $300M and $400M term loan facilities depending on our credit ratings and leverage ratio. There is also a sustainability-linked pricing component that can periodically change the margin by -/+ 0.04% (or zero) depending on our achievement of the annual sustainability performance metric. The sustainability-linked pricing adjustment for the margin is currently zero.

(6)Noteholders have the right to exchange their notes upon the occurrence of certain events. Exchanges will be settled in cash or in a combination of cash and shares of our common stock, at our option.

(7)We effectively fixed 1M SOFR related to our $300M term loan facility at a weighted average rate of 2.81725%, commencing on July 27, 2022 through May 26, 2027, through the use of interest rate swaps. The all-in fixed rate on the $300M term loan facility is 3.717% after adding the SOFR adjustment, applicable margin and sustainability-related rate adjustment.

(8)We effectively fixed Daily SOFR related to our $400M term loan facility at a weighted average rate of 3.41375%, commencing on July 1, 2025 through May 30, 2030, through the use of three new interest rate swaps that we executed on June 30, 2025. These swaps take the place of the swaps that were previously in place from April 3, 2023 through June 30, 2025, which fixed Daily SOFR at 3.97231%. The all-in fixed rate of 4.214% disclosed in the table reflects the impact of the new swaps (assuming they were effective as of June 30, 2025) after adding the applicable margin and sustainability-related rate adjustment.

(9)The $60M term loan facility has interest-only payment terms (1M SOFR + 0.10% SOFR adjustment + margin of 1.250%) and three one-year extensions available at the borrower’s option, subject to certain terms & conditions. On July 11, 2025, we exercised the second extension option, extending the loan’s maturity date by one additional year to October 27, 2026, which has been reflected in the table.

(10)We effectively fixed 1M SOFR related to our $60M term loan facility at 3.710%, commencing on April 3, 2023 through July 30, 2026, through the use of an interest rate swap. The all-in fixed rate on the $60M term loan facility is 5.060% after adding the SOFR adjustment and applicable margin.

(11)Excludes potential exercise of extension options and excludes the effect of scheduled monthly principal payments on amortizing secured loans.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 19

|

|

||||||

Operations.

|

||||||||

| Quarterly Results | ||||||||

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 20

|

|

||||||

Portfolio Overview.

|

||||||||

| At June 30, 2025 | (unaudited results) | |||||||

| Consolidated Portfolio: | ||||||||

| Rentable Square Feet | Ending Occupancy % |

In-Place ABR(3)

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Market | # of Properties |

Same Property Portfolio |

Non-Same Property Portfolio |

Total Portfolio |

Same Property Portfolio |

Non-Same Property Portfolio |

Total

Portfolio(1)

|

Total Portfolio

Excluding

Repo/Redev(2)

|

Total (in 000’s) |

Per Square Foot |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Central LA | 21 | 2,803,152 | 451,803 | 3,254,955 | 96.2 | % | 61.7 | % | 91.4 | % | 99.0 | % | $ | 40,126 | $13.49 | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Greater San Fernando Valley | 74 | 5,485,235 | 1,698,421 | 7,183,656 | 96.3 | % | 64.5 | % | 88.8 | % | 96.4 | % | 110,490 | $17.32 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Mid-Counties | 39 | 2,984,698 | 1,669,792 | 4,654,490 | 98.8 | % | 67.9 | % | 87.7 | % | 98.8 | % | 68,519 | $16.78 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| San Gabriel Valley | 47 | 3,407,578 | 2,642,777 | 6,050,355 | 93.4 | % | 66.8 | % | 81.8 | % | 86.1 | % | 70,825 | $14.32 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| South Bay | 81 | 6,303,325 | 1,573,663 | 7,876,988 | 96.9 | % | 64.0 | % | 90.3 | % | 97.7 | % | 162,544 | $22.84 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Los Angeles County | 262 | 20,983,988 | 8,036,456 | 29,020,444 | 96.4 | % | 65.7 | % | 87.9 | % | 95.2 | % | 452,504 | $17.75 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| North Orange County | 25 | 1,094,646 | 1,580,440 | 2,675,086 | 97.9 | % | 75.0 | % | 84.4 | % | 92.6 | % | 43,378 | $19.21 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| OC Airport | 10 | 1,099,985 | 106,604 | 1,206,589 | 99.2 | % | 100.0 | % | 99.3 | % | 99.3 | % | 23,309 | $19.46 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| South Orange County | 9 | 346,463 | 183,098 | 529,561 | 100.0 | % | 88.9 | % | 96.2 | % | 100.0 | % | 8,796 | $17.27 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| West Orange County | 10 | 852,079 | 436,759 | 1,288,838 | 100.0 | % | 81.0 | % | 93.6 | % | 98.1 | % | 19,929 | $16.52 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Orange County | 54 | 3,393,173 | 2,306,901 | 5,700,074 | 99.1 | % | 78.4 | % | 90.7 | % | 96.1 | % | 95,412 | $18.45 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Inland Empire East | 1 | 33,258 | — | 33,258 | 100.0 | % | — | % | 100.0 | % | 100.0 | % | 660 | $19.86 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Inland Empire West | 53 | 8,490,725 | 1,051,523 | 9,542,248 | 95.5 | % | 80.9 | % | 93.9 | % | 95.9 | % | 136,550 | $15.25 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Riverside / San Bernardino County | 54 | 8,523,983 | 1,051,523 | 9,575,506 | 95.5 | % | 80.9 | % | 93.9 | % | 96.0 | % | 137,210 | $15.27 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Central San Diego | 21 | 1,349,009 | 779,311 | 2,128,320 | 98.8 | % | 51.8 | % | 81.6 | % | 90.9 | % | 36,280 | $20.89 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| North County San Diego | 13 | 1,230,247 | 143,663 | 1,373,910 | 94.1 | % | 100.0 | % | 94.7 | % | 94.7 | % | 19,565 | $15.04 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| San Diego County | 34 | 2,579,256 | 922,974 | 3,502,230 | 96.5 | % | 59.3 | % | 86.7 | % | 92.5 | % | 55,845 | $18.39 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Ventura | 18 | 2,510,848 | 712,795 | 3,223,643 | 91.5 | % | 73.4 | % | 87.5 | % | 90.9 | % | 37,858 | $13.42 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Ventura County | 18 | 2,510,848 | 712,795 | 3,223,643 | 91.5 | % | 73.4 | % | 87.5 | % | 90.9 | % | 37,858 | $13.42 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| CONSOLIDATED TOTAL / WTD AVG | 422 | 37,991,248 | 13,030,649 | 51,021,897 | 96.1 | % | 69.1 | % | 89.2 | % | 95.0 | % | $ | 778,829 | $17.11 | (4) |

|||||||||||||||||||||||||||||||||||||||||||||||||

(1)See page 38 for historical occupancy by County.

(2)Excludes space aggregating 3,094,182 square feet at our properties that were in various stages of repositioning, redevelopment or lease-up as of June 30, 2025. See pages 26-31 for additional details on these properties.

(3)See page 34 for definitions and details on how these amounts are calculated.

(4)Excluding in-place ABR associated with Land/IOS properties ($45.349M) and cellular tower, solar and parking lot leases ($2.698M ABR), in-place building ABR per building SF was $16.14.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 21

|

|

||||||

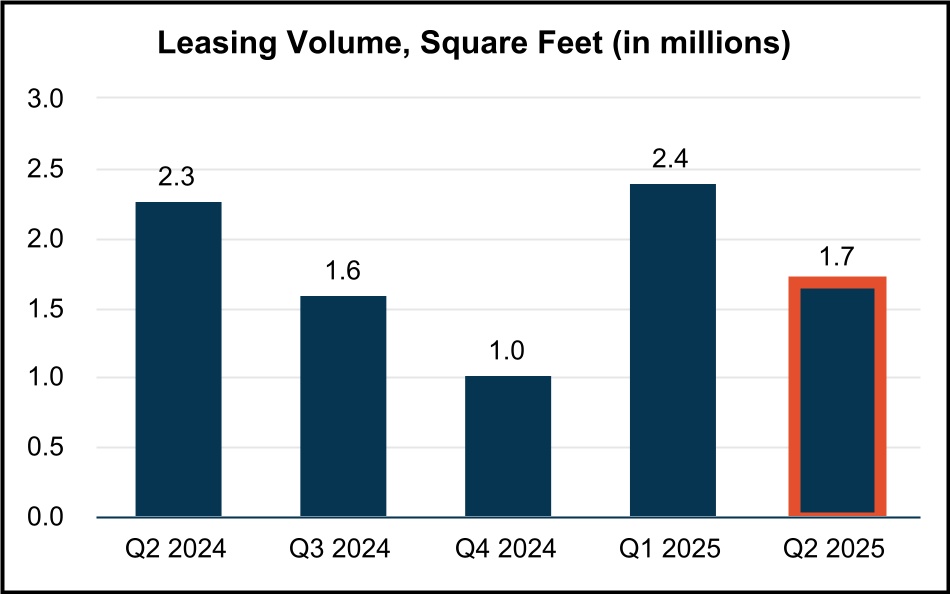

Executed Leasing Statistics and Trends.

|

||||||||

| (unaudited results) | ||||||||

| Executed Leasing Activity and Weighted Average New / Renewal Leasing Spreads: | ||||||||

| Three Months Ended | ||||||||||||||||||||||||||||||||

| Jun 30, 2025 | Mar 31, 2025 | Dec 31, 2024 | Sep 30, 2024 | Jun 30, 2024 | ||||||||||||||||||||||||||||

| Leasing Spreads: | ||||||||||||||||||||||||||||||||

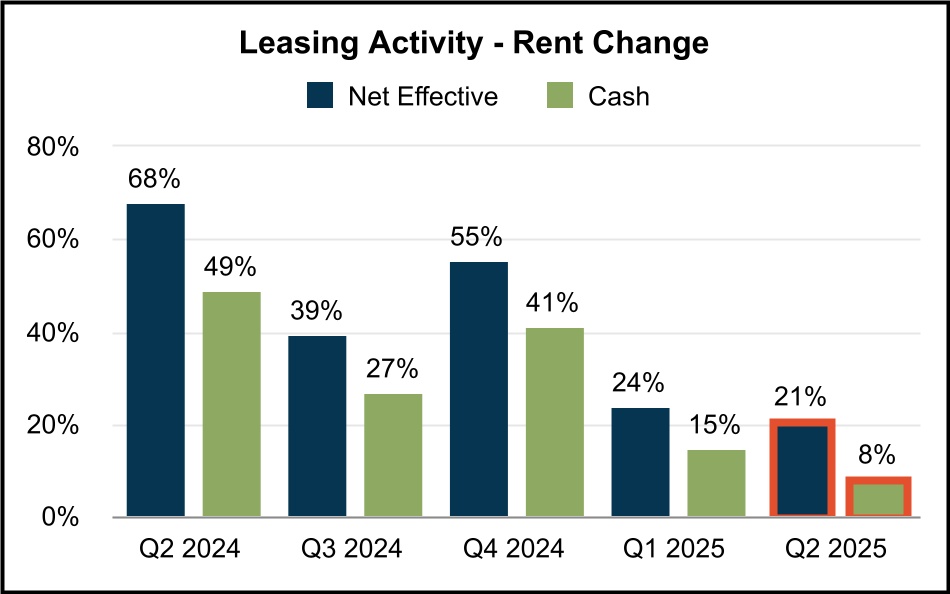

| Net Effective Rent Change | 20.9 | % | 23.8 | % | 55.4 | % | 39.2 | % | 67.7 | % | ||||||||||||||||||||||

| Cash Rent Change | 8.1 | % | 14.7 | % | 41.0 | % | 26.7 | % | 49.0 | % | ||||||||||||||||||||||

Leasing Activity (Building SF):(1)(2)

|

||||||||||||||||||||||||||||||||

| New leases | 678,727 | 882,403 | 330,334 | 994,566 | 1,033,006 | |||||||||||||||||||||||||||

| Renewal leases | 1,020,266 | 1,511,946 | 684,961 | 599,529 | 1,228,905 | |||||||||||||||||||||||||||

| Total leasing activity | 1,698,993 | 2,394,349 | 1,015,295 | 1,594,095 | 2,261,911 | |||||||||||||||||||||||||||

| Total expiring leases | (1,786,814) | (3,102,514) | (2,436,160) | (1,677,064) | (2,038,430) | |||||||||||||||||||||||||||

| Expiring leases - placed into repositioning/redevelopment | 304,776 | 833,218 | 996,035 | 476,821 | 175,533 | |||||||||||||||||||||||||||

Net absorption(3)

|

216,955 | 125,053 | (424,830) | 393,852 | 399,014 | |||||||||||||||||||||||||||

Retention rate(4)

|

69 | % | 68 | % | 51 | % | 52 | % | 68 | % | ||||||||||||||||||||||

Retention + Backfill rate(5)

|

74 | % | 82 | % | 62 | % | 72 | % | 80 | % | ||||||||||||||||||||||

Executed Leasing Activity and Change in Annual Rental Rates and Turnover Costs for Current Quarter Leases:(6)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Net Effective Rent |

Cash Rent |

Turnover Costs(8)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Second Quarter 2025: | # Leases Signed |

SF of Leasing |

Wtd. Avg. Lease Term (Years) |

Current Lease |

Prior Lease |

Rent Change |

Current Lease |

Prior Lease |

Rent Change |

Wtd. Avg. Abatement (Months) |

Tenant

Improvements

per SF

|

Leasing

Commissions

per SF

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

New(7)

|

41 | 678,727 | 4.8 | $15.31 | $18.57 | (17.6)% | $15.46 | $20.05 | (22.9)% | 4.0 | $2.42 | $4.16 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Renewal | 58 | 1,020,266 | 4.2 | $17.49 | $13.33 | 31.2% | $17.11 | $14.72 | 16.3% | 2.2 | $0.54 | $2.40 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total / Wtd. Average | 99 | 1,698,993 | 4.5 | $17.14 | $14.18 | 20.9% | $16.85 | $15.58 | 8.1% | 2.5 | $0.85 | $2.68 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

(1)Represents all executed leases, including those in our Repositioning, Redevelopment, or “Other Repositioning” classifications, but excludes month-to-month tenants and leases with terms less than 12 months.

(2)Leasing activity for Q2-2025 excludes the following land lease activity: (i) one new land lease deal with 14,370 land SF and (ii) three renewal land lease deals with a combined 292,870 land SF and (iii) three expiring land leases with 292,870 land SF. The weighted average net effective rent and cash rent changes for the three renewal land leases were 110.3% and 25.6%, respectively. The one new lease did not have any comparable lease data.

(3)Net absorption represents total leasing activity, less expiring leases adjusted for square footage placed into Repositioning, Redevelopment or “Other Repositioning.”

(4)Retention rate is calculated as renewal lease square footage plus relocation/expansion square footage, divided by expiring lease square footage. Retention excludes square footage related to the following: (i) expiring leases associated with space that is placed into repositioning/redevelopment (including “Other Repositioning” projects) after the tenant vacates, (ii) early terminations with prenegotiated replacement leases and (iii) move outs where space is directly leased by subtenants.

(5)Retention + Backfill rate represents square feet retained (per Retention rate definition in footnote (4)) plus the square footage of move outs in the quarter which were re-leased prior to or during the same quarter, divided by expiring lease square footage.

(6)Net effective and cash rent statistics and turnover costs exclude 43 new leases aggregating 482,297 RSF for which there was no comparable lease data. Comparable leases generally exclude: (i) space that has never been occupied under our ownership, (ii) repositioned/redeveloped space, including space in pre-development/entitlement process, (iii) space that has been vacant for greater than 1 year or (iv) lease terms less than 12 months. Net effective and cash rent statistics and turnover costs for building leases also exclude land lease deals noted in footnote (2) above.

(7)The net effective and cash releasing spreads for new leases were disproportionately impacted by a 106,251-square-foot lease with a net effective and cash releasing spread of (31.6%) and (36.9%), respectively. This lease represented approximately 54% of the 196,430 square feet of comparable new leases signed during the quarter. Excluding this lease, net effective and cash releasing spreads for new leases would have been (0.5%) and 4.2%, respectively.

(8)Turnover costs include estimated tenant improvement and leasing costs associated with leases executed during the current period. Excludes costs for 1st generation leases.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 22

|

|

||||||

Leasing Statistics (Continued).

|

||||||||

| (unaudited results) | ||||||||

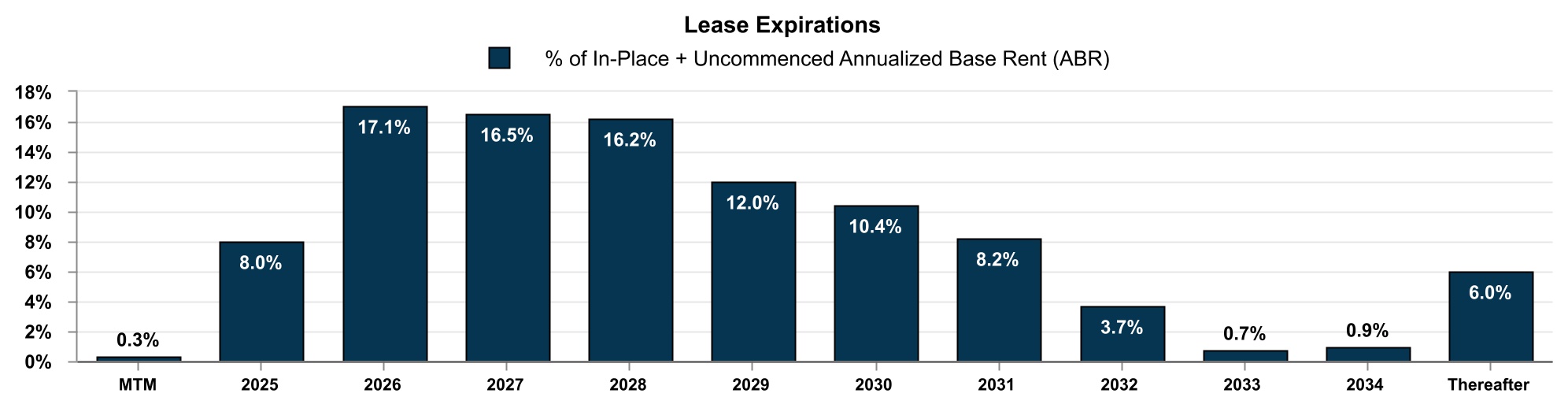

| Lease Expiration Schedule as of June 30, 2025: | ||||||||

| Year of Lease Expiration | # of Leases Expiring |

Total Rentable Square Feet |

In-Place + Uncommenced ABR (in thousands) |

In-Place + Uncommenced ABR per SF |

||||||||||||||||||||||

| Available | — | 2,335,464 | $ | — | $— | |||||||||||||||||||||

Repositioning/Redevelopment(1)

|

— | 2,871,961 | — | $— | ||||||||||||||||||||||

| MTM Tenants | 4 | 131,415 | 2,172 | $16.53 | ||||||||||||||||||||||

| 2025 | 194 | 4,122,156 | 62,790 | $15.23 | ||||||||||||||||||||||

| 2026 | 420 | 8,657,602 | 134,289 | $15.51 | ||||||||||||||||||||||

| 2027 | 343 | 7,439,877 | 129,504 | $17.41 | ||||||||||||||||||||||

| 2028 | 252 | 6,753,145 | 126,904 | $18.79 | ||||||||||||||||||||||

| 2029 | 168 | 4,958,782 | 94,085 | $18.97 | ||||||||||||||||||||||

| 2030 | 119 | 5,079,934 | 81,958 | $16.13 | ||||||||||||||||||||||

| 2031 | 38 | 4,408,532 | 64,651 | $14.66 | ||||||||||||||||||||||

| 2032 | 23 | 1,392,533 | 28,229 | $20.27 | ||||||||||||||||||||||

| 2033 | 9 | 296,735 | 5,832 | $19.66 | ||||||||||||||||||||||

| 2034 | 7 | 355,445 | 6,980 | $19.64 | ||||||||||||||||||||||

| Thereafter | 36 | 2,218,316 | 46,943 | $21.16 | ||||||||||||||||||||||

| Total Portfolio | 1,613 | 51,021,897 | $ | 784,337 |

$17.12(2)

|

|||||||||||||||||||||

(1)Represents vacant space at properties that were classified as repositioning (including “Other Repositionings”), redevelopment or lease-up as of June 30, 2025. See pages 26-31 for additional details on these properties.

(2)Excluding in-place + uncommenced ABR associated with Land/IOS properties ($45.349M) and cellular tower, solar and parking lot leases ($2.698M ABR), in-place + uncommenced ABR per building SF was $16.15.

|

Second Quarter 2025

Supplemental Financial Reporting Package

|

Page 23

|

|

||||||

Top Tenants and Lease Segmentation.

|

||||||||

| (unaudited results) | ||||||||

Top 20 Tenants as of June 30, 2025 |

||||||||

| Tenant | Submarket | Leased Rentable SF |

In-Place + Uncommenced

ABR (in 000’s)(1)

|

% of In-Place +

Uncommenced ABR(1)

|

In-Place + Uncommenced

ABR per SF(1)

|

Lease Expiration |

||||||||||||||||||||||||||||||||

| Tireco, Inc. | Inland Empire West | 1,101,840 | $19,251 | 2.5% | $17.47 | 1/31/2027 | ||||||||||||||||||||||||||||||||

| L3 Technologies, Inc. |

Multiple Submarkets(2)

|

595,267 | $12,967 | 1.6% | $21.78 | 9/30/2031 | ||||||||||||||||||||||||||||||||

| Zenith Energy West Coast Terminals LLC | South Bay |

—(3)

|

$11,675 | 1.5% |

$3.34(3)

|

9/29/2041 | ||||||||||||||||||||||||||||||||

| Cubic Corporation | Central San Diego | 515,382 | $11,443 | 1.5% | $22.20 |

3/31/2038(4)

|

||||||||||||||||||||||||||||||||

| IBY, LLC | San Gabriel Valley | 1,178,021 | $11,322 | 1.4% | $9.61 |

4/5/2031(5)

|

||||||||||||||||||||||||||||||||

| Federal Express Corporation |

Multiple Submarkets(6)

|