EX-99.2

Published on May 6, 2015

Exhibit 99.2

Supplemental Financial Reporting Package First Quarter 2015 Rexford Industrial Realty, Inc. NYSE: REXR 11620 Wilshire Blvd Suite 1000 Los Angeles, CA 90025 310-966-1680 www.RexfordIndustrial.com

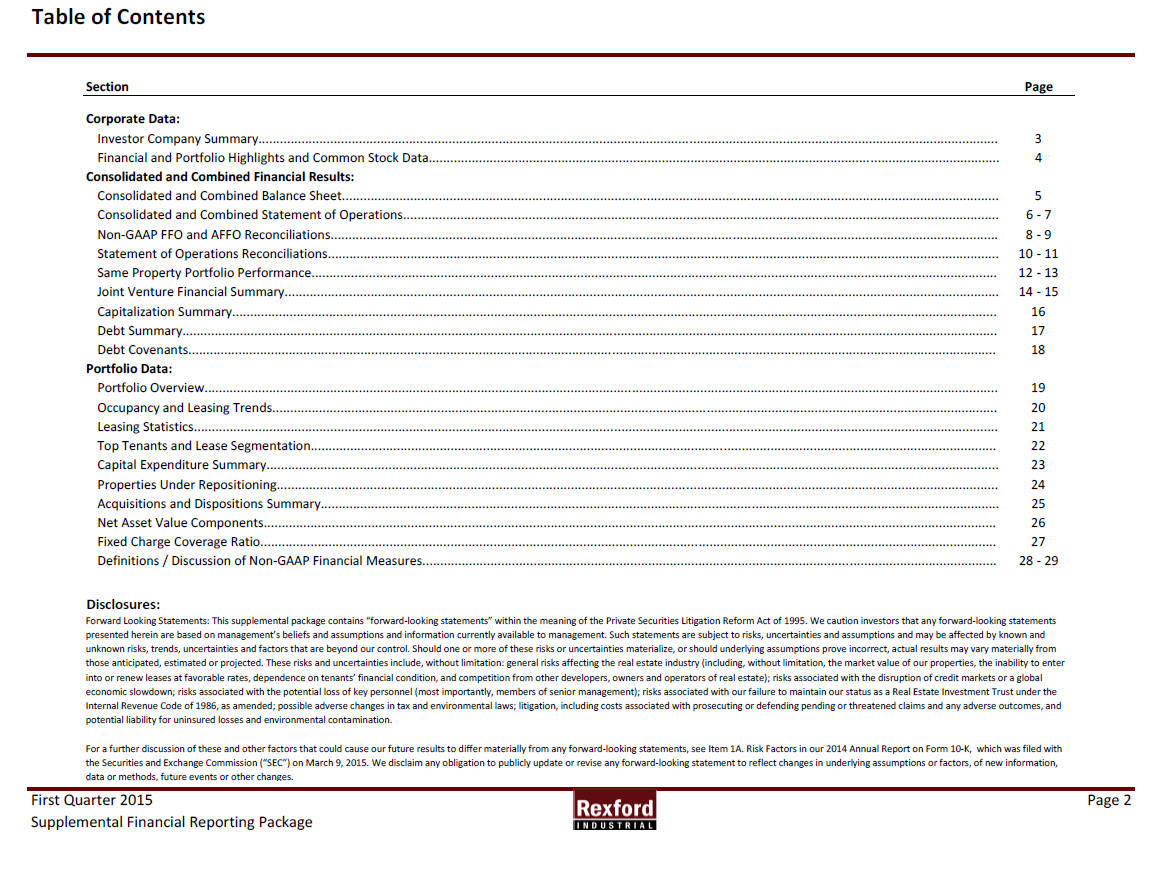

Table of Contents Section Page Corporate Data: Investor Company Summary.............................................................................................................................................................................................................. 3 Financial and Portfolio Highlights and Common Stock Data............................................................................................................................................................... 4 Consolidated and Combined Financial Results: Consolidated and Combined Balance Sheet....................................................................................................................................................................................... 5 Consolidated and Combined Statement of Operations...................................................................................................................................................................... 6 - 7 Non-GAAP FFO and AFFO Reconciliations.......................................................................................................................................................................................... 8 - 9 Statement of Operations Reconciliations........................................................................................................................................................................................... 10 - 11 Same Property Portfolio Performance............................................................................................................................................................................................... 12 - 13 Joint Venture Financial Summary....................................................................................................................................................................................................... 14 - 15 Capitalization Summary..................................................................................................................................................................................................................... 16 Debt Summary................................................................................................................................................................................................................................... 17 Debt Covenants................................................................................................................................................................................................................................. 18 Portfolio Data: Portfolio Overview............................................................................................................................................................................................................................. 19 Occupancy and Leasing Trends.......................................................................................................................................................................................................... 20 Leasing Statistics................................................................................................................................................................................................................................ 21 Top Tenants and Lease Segmentation............................................................................................................................................................................................... 22 Capital Expenditure Summary............................................................................................................................................................................................................ 23 Properties Under Repositioning......................................................................................................................................................................................................... 24 Acquisitions and Dispositions Summary............................................................................................................................................................................................. 25 Net Asset Value Components............................................................................................................................................................................................................ 26 Fixed Charge Coverage Ratio............................................................................................................................................................................................................. 27 Definitions / Discussion of Non-GAAP Financial Measures................................................................................................................................................................ 28 - 29 Disclosures: First Quarter 2015 Page 2 Supplemental Financial Reporting Package Forward Looking Statements: This supplemental package contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. We caution investors that any forward-looking statements presented herein are based on management’s beliefs and assumptions and information currently available to management. Such statements are subject to risks, uncertainties and assumptions and may be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. These risks and uncertainties include, without limitation: general risks affecting the real estate industry (including, without limitation, the market value of our properties, the inability to enter into or renew leases at favorable rates, dependence on tenants’ financial condition, and competition from other developers, owners and operators of real estate); risks associated with the disruption of credit markets or a global economic slowdown; risks associated with the potential loss of key personnel (most importantly, members of senior management); risks associated with our failure to maintain our status as a Real Estate Investment Trust under the Internal Revenue Code of 1986, as amended; possible adverse changes in tax and environmental laws; litigation, including costs associated with prosecuting or defending pending or threatened claims and any adverse outcomes, and potential liability for uninsured losses and environmental contamination. For a further discussion of these and other factors that could cause our future results to differ materially from any forward-looking statements, see Item 1A. Risk Factors in our 2014 Annual Report on Form 10-K, which was filed with the Securities and Exchange Commission (“SEC”) on March 9, 2015. We disclaim any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, of new information, data or methods, future events or other changes.

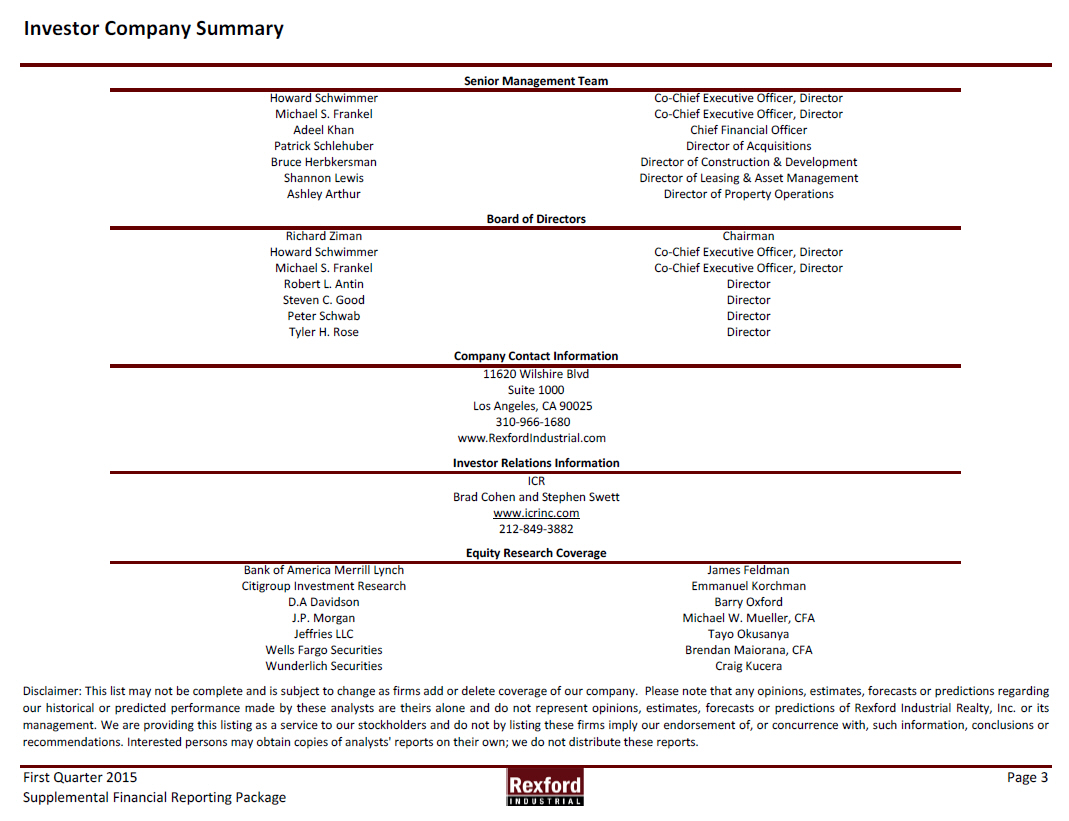

Investor Company Summary Senior Management Team Howard Schwimmer Co-Chief Executive Officer, Director Michael S. Frankel Co-Chief Executive Officer, Director Adeel Khan Chief Financial Officer Patrick Schlehuber Director of Acquisitions Bruce Herbkersman Director of Construction & Development Shannon Lewis Director of Leasing & Asset Management Ashley Arthur Director of Property Operations Board of Directors Richard Ziman Chairman Howard Schwimmer Co-Chief Executive Officer, Director Michael S. Frankel Co-Chief Executive Officer, Director Robert L. Antin Director Steven C. Good Director Peter Schwab Director Tyler H. Rose Director Company Contact Information 11620 Wilshire Blvd Suite 1000 Los Angeles, CA 90025 310-966-1680 www.RexfordIndustrial.com Investor Relations Information ICR Brad Cohen and Stephen Swett www.icrinc.com 212-849-3882 Equity Research Coverage Bank of America Merrill Lynch James Feldman Citigroup Investment Research Emmanuel Korchman D.A Davidson Barry Oxford J.P. Morgan Michael W. Mueller, CFA Jeffries LLC Tayo Okusanya Wells Fargo Securities Brendan Maiorana, CFA Wunderlich Securities Craig Kucera First Quarter 2015 Page 3 Supplemental Financial Reporting Package Disclaimer: This list may not be complete and is subject to change as firms add or delete coverage of our company. Please note that any opinions, estimates, forecasts or predictions regarding our historical or predicted performance made by these analysts are theirs alone and do not represent opinions, estimates, forecasts or predictions of Rexford Industrial Realty, Inc. or its management. We are providing this listing as a service to our stockholders and do not by listing these firms imply our endorsement of, or concurrence with, such information, conclusions or recommendations. Interested persons may obtain copies of analysts' reports on their own; we do not distribute these reports.

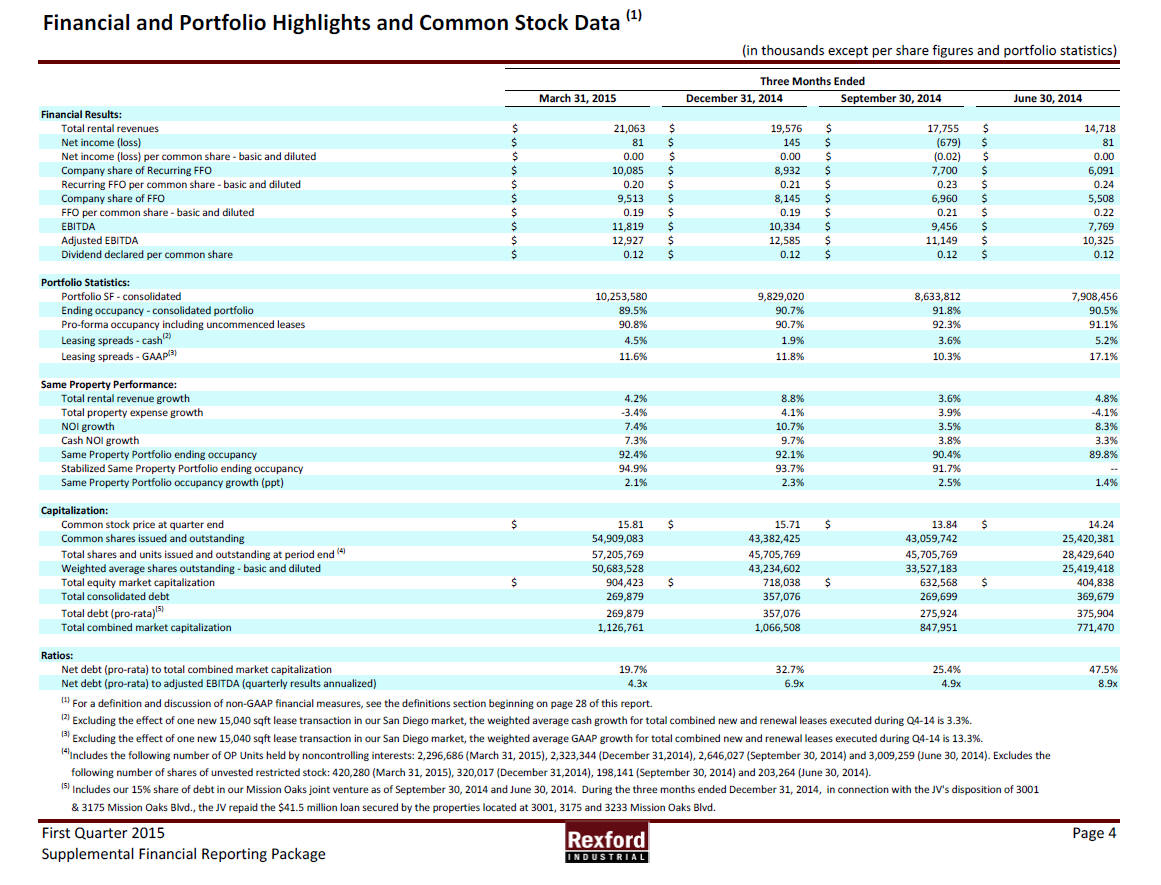

Financial and Portfolio Highlights and Common Stock Data (1) (in thousands except per share figures and portfolio statistics) March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 Financial Results: Total rental revenues $ 21,063 $ 19,576 $ 17,755 $ 14,718 Net income (loss) $ 81 $ 145 $ (679) $ 81 Net income (loss) per common share - basic and diluted $ 0.00 $ 0.00 $ (0.02) $ 0 .00 Company share of Recurring FFO $ 10,085 $ 8,932 $ 7,700 $ 6,091 Recurring FFO per common share - basic and diluted $ 0.20 $ 0.21 $ 0.23 $ 0.24 Company share of FFO $ 9,513 $ 8,145 $ 6,960 $ 5,508 FFO per common share - basic and diluted $ 0.19 $ 0.19 $ 0.21 $ 0.22 EBITDA $ 11,819 $ 10,334 $ 9,456 $ 7,769 Adjusted EBITDA $ 12,927 $ 12,585 $ 11,149 $ 10,325 Dividend declared per common share $ 0.12 $ 0.12 $ 0.12 $ 0.12 Portfolio Statistics: Portfolio SF - consolidated 10,253,580 9,829,020 8,633,812 7,908,456 Ending occupancy - consolidated portfolio 89.5% 90.7% 91.8% 90.5% Pro-forma occupancy including uncommenced leases 90.8% 90.7% 92.3% 91.1% Leasing spreads - cash(2) 4.5% 1.9% 3.6% 5.2% Leasing spreads - GAAP(3) 11.6% 11.8% 10.3% 17.1% Same Property Performance: Total rental revenue growth 4.2% 8.8% 3.6% 4.8% Total property expense growth -3.4% 4.1% 3.9% -4.1% NOI growth 7.4% 10.7% 3.5% 8.3% Cash NOI growth 7.3% 9.7% 3.8% 3.3% Same Property Portfolio ending occupancy 92.4% 92.1% 90.4% 89.8% Stabilized Same Property Portfolio ending occupancy 94.9% 93.7% 91.7% -- Same Property Portfolio occupancy growth (ppt) 2.1% 2.3% 2.5% 1.4% Capitalization: Common stock price at quarter end $ 15.81 $ 15.71 $ 13.84 $ 14.24 Common shares issued and outstanding 54,909,083 43,382,425 43,059,742 25,420,381 Total shares and units issued and outstanding at period end (4) 57,205,769 45,705,769 45,705,769 28,429,640 Weighted average shares outstanding - basic and diluted 50,683,528 43,234,602 33,527,183 25,419,418 Total equity market capitalization $ 904,423 $ 718,038 $ 632,568 $ 404,838 Total consolidated debt 269,879 357,076 269,699 369,679 Total debt (pro-rata)(5) 269,879 357,076 275,924 375,904 Total combined market capitalization 1,126,761 1,066,508 847,951 771,470 Ratios: Net debt (pro-rata) to total combined market capitalization 19.7% 32.7% 25.4% 47.5% Net debt (pro-rata) to adjusted EBITDA (quarterly results annualized) 4.3x 6.9x 4.9x 8.9x (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. (2) Excluding the effect of one new 15,040 sqft lease transaction in our San Diego market, the weighted average cash growth for total combined new and renewal leases executed during Q4-14 is 3.3%. (3) Excluding the effect of one new 15,040 sqft lease transaction in our San Diego market, the weighted average GAAP growth for total combined new and renewal leases executed during Q4-14 is 13.3%. (4)Includes the following number of OP Units held by noncontrolling interests: 2,296,686 (March 31, 2015), 2,323,344 (December 31,2014), 2,646,027 (September 30, 2014) and 3,009,259 (June 30, 2014). Excludes the following number of shares of unvested restricted stock: 420,280 (March 31, 2015), 320,017 (December 31,2014), 198,141 (September 30, 2014) and 203,264 (June 30, 2014). (5) Includes our 15% share of debt in our Mission Oaks joint venture as of September 30, 2014 and June 30, 2014. During the three months ended December 31, 2014, in connection with the JV's disposition of 3001 & 3175 Mission Oaks Blvd., the JV repaid the $41.5 million loan secured by the properties located at 3001, 3175 and 3233 Mission Oaks Blvd. First Quarter 2015 Page 4 Supplemental Financial Reporting Package Three Months Ended

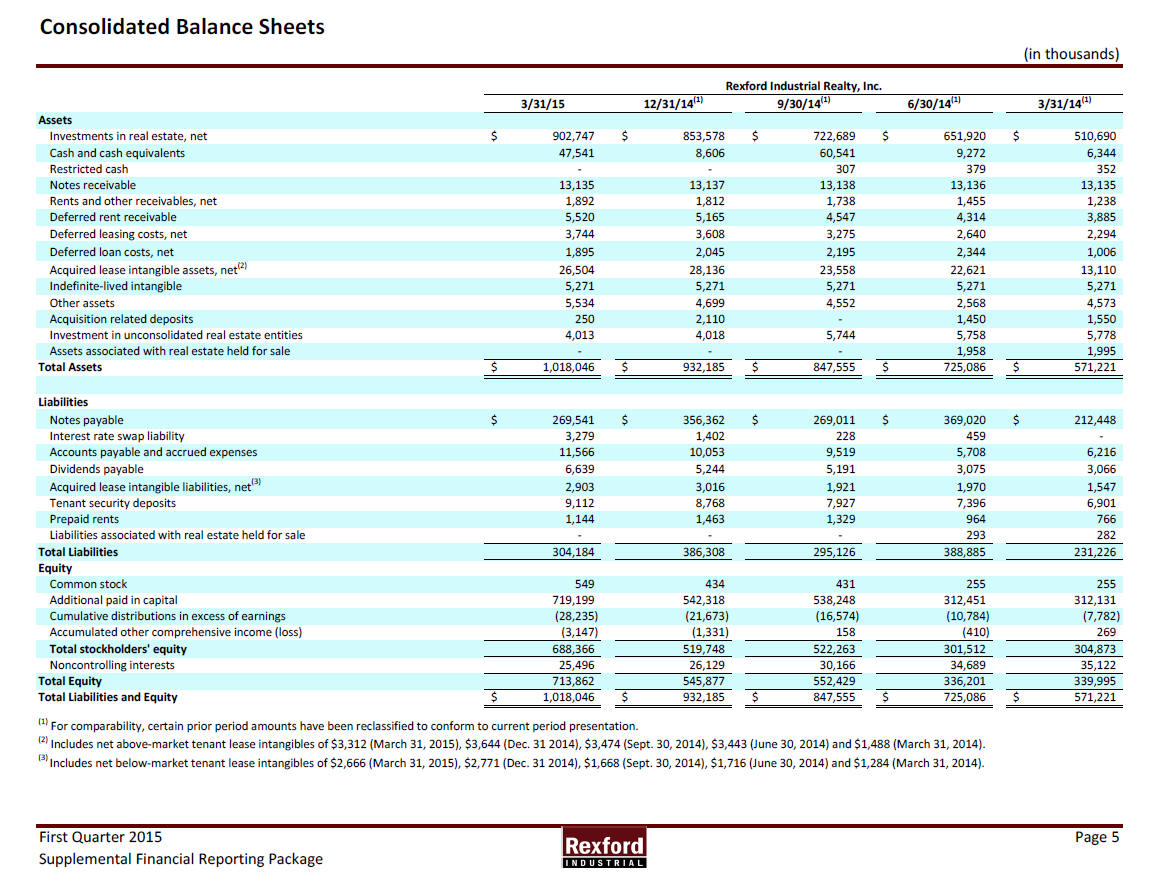

Consolidated Balance Sheets (in thousands) 3/31/15 12/31/14(1) 9/30/14(1) 6/30/14(1) 3/31/14(1) Assets Investments in real estate, net $ 902,747 $ 853,578 $ 722,689 $ 651,920 $ 510,690 Cash and cash equivalents 47,541 8,606 60,541 9,272 6,344 Restricted cash - - 307 379 352 Notes receivable 13,135 13,137 13,138 13,136 13,135 Rents and other receivables, net 1,892 1,812 1,738 1,455 1,238 Deferred rent receivable 5,520 5,165 4,547 4,314 3,885 Deferred leasing costs, net 3,744 3,608 3,275 2,640 2,294 Deferred loan costs, net 1,895 2,045 2,195 2,344 1,006 Acquired lease intangible assets, net(2) 26,504 28,136 23,558 22,621 13,110 Indefinite-lived intangible 5,271 5,271 5,271 5,271 5,271 Other assets 5,534 4,699 4,552 2,568 4,573 Acquisition related deposits 250 2,110 - 1,450 1,550 Investment in unconsolidated real estate entities 4,013 4,018 5,744 5,758 5,778 Assets associated with real estate held for sale - - - 1,958 1,995 Total Assets $ 1,018,046 $ 932,185 $ 847,555 $ 725,086 $ 571,221 Liabilities Notes payable $ 269,541 $ 356,362 $ 269,011 $ 369,020 $ 212,448 Interest rate swap liability 3,279 1,402 228 459 - Accounts payable and accrued expenses 11,566 10,053 9,519 5,708 6,216 Dividends payable 6,639 5,244 5,191 3,075 3,066 Acquired lease intangible liabilities, net(3) 2,903 3,016 1,921 1,970 1,547 Tenant security deposits 9,112 8,768 7,927 7,396 6,901 Prepaid rents 1,144 1,463 1,329 964 766 Liabilities associated with real estate held for sale - - - 293 282 Total Liabilities 304,184 386,308 295,126 388,885 231,226 Equity Common stock 549 434 431 255 255 Additional paid in capital 719,199 542,318 538,248 312,451 312,131 Cumulative distributions in excess of earnings (28,235) (21,673) (16,574) (10,784) (7,782) Accumulated other comprehensive income (loss) (3,147) (1,331) 158 (410) 269 Total stockholders' equity 688,366 519,748 522,263 301,512 304,873 Noncontrolling interests 25,496 26,129 30,166 34,689 35,122 Total Equity 713,862 545,877 552,429 336,201 339,995 Total Liabilities and Equity $ 1,018,046 $ 932,185 $ 847,555 $ 725,086 $ 571,221 (1) For comparability, certain prior period amounts have been reclassified to conform to current period presentation. (2) Includes net above-market tenant lease intangibles of $3,312 (March 31, 2015), $3,644 (Dec. 31 2014), $3,474 (Sept. 30, 2014), $3,443 (June 30, 2014) and $1,488 (March 31, 2014). (3) Includes net below-market tenant lease intangibles of $2,666 (March 31, 2015), $2,771 (Dec. 31 2014), $1,668 (Sept. 30, 2014), $1,716 (June 30, 2014) and $1,284 (March 31, 2014). First Quarter 2015 Page 5 Supplemental Financial Reporting Package Rexford Industrial Realty, Inc.

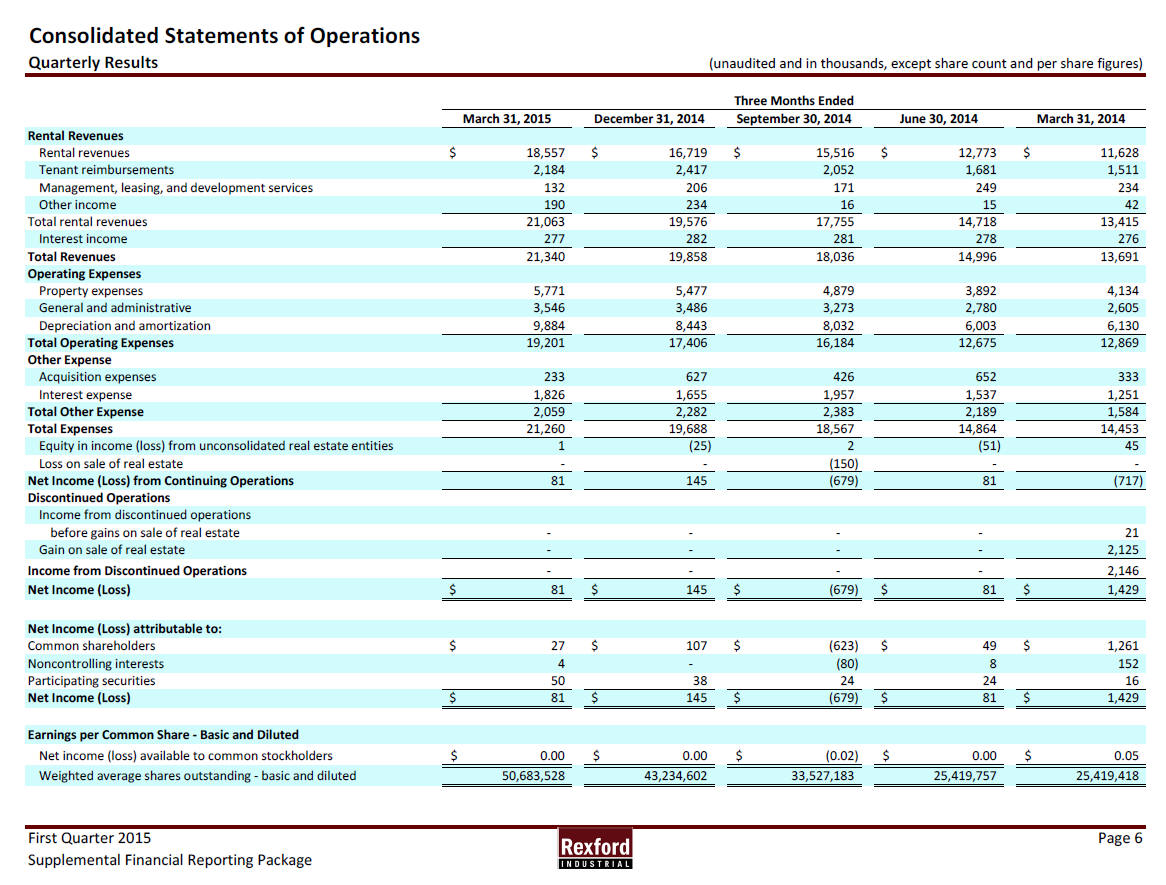

Consolidated Statements of Operations Quarterly Results (unaudited and in thousands, except share count and per share figures) March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 March 31, 2014 Rental Revenues Rental revenues $ 18,557 $ 16,719 $ 15,516 $ 12,773 $ 11,628 Tenant reimbursements 2,184 2,417 2,052 1,681 1,511 Management, leasing, and development services 132 206 171 249 234 Other income 190 234 16 15 42 Total rental revenues 21,063 19,576 17,755 14,718 13,415 Interest income 277 282 281 278 276 Total Revenues 21,340 19,858 18,036 14,996 13,691 Operating Expenses Property expenses 5,771 5,477 4,879 3,892 4,134 General and administrative 3,546 3,486 3,273 2,780 2,605 Depreciation and amortization 9,884 8,443 8,032 6,003 6,130 Total Operating Expenses 19,201 17,406 16,184 12,675 12,869 Other Expense Acquisition expenses 233 627 426 652 333 Interest expense 1,826 1,655 1,957 1,537 1,251 Total Other Expense 2,059 2,282 2,383 2,189 1,584 Total Expenses 21,260 19,688 18,567 14,864 14,453 Equity in income (loss) from unconsolidated real estate entities 1 ( 25) 2 (51) 45 Loss on sale of real estate - - (150) - - Net Income (Loss) from Continuing Operations 81 145 (679) 81 (717) Discontinued Operations Income from discontinued operations before gains on sale of real estate - - - - 21 Gain on sale of real estate - - - - 2,125 Income from Discontinued Operations - - - - 2,146 Net Income (Loss) $ 81 $ 145 $ ( 679) $ 81 $ 1,429 Net Income (Loss) attributable to: Common shareholders $ 27 $ 107 $ (623) $ 49 $ 1,261 Noncontrolling interests 4 - (80) 8 152 Participating securities 50 38 24 24 16 Net Income (Loss) $ 81 $ 145 $ (679) $ 81 $ 1,429 Earnings per Common Share - Basic and Diluted Net income (loss) available to common stockholders $ 0.00 $ 0.00 $ (0.02) $ 0.00 $ 0.05 Weighted average shares outstanding - basic and diluted 50,683,528 43,234,602 3 3,527,183 25,419,757 25,419,418 First Quarter 2015 Page 6 Supplemental Financial Reporting Package Three Months Ended

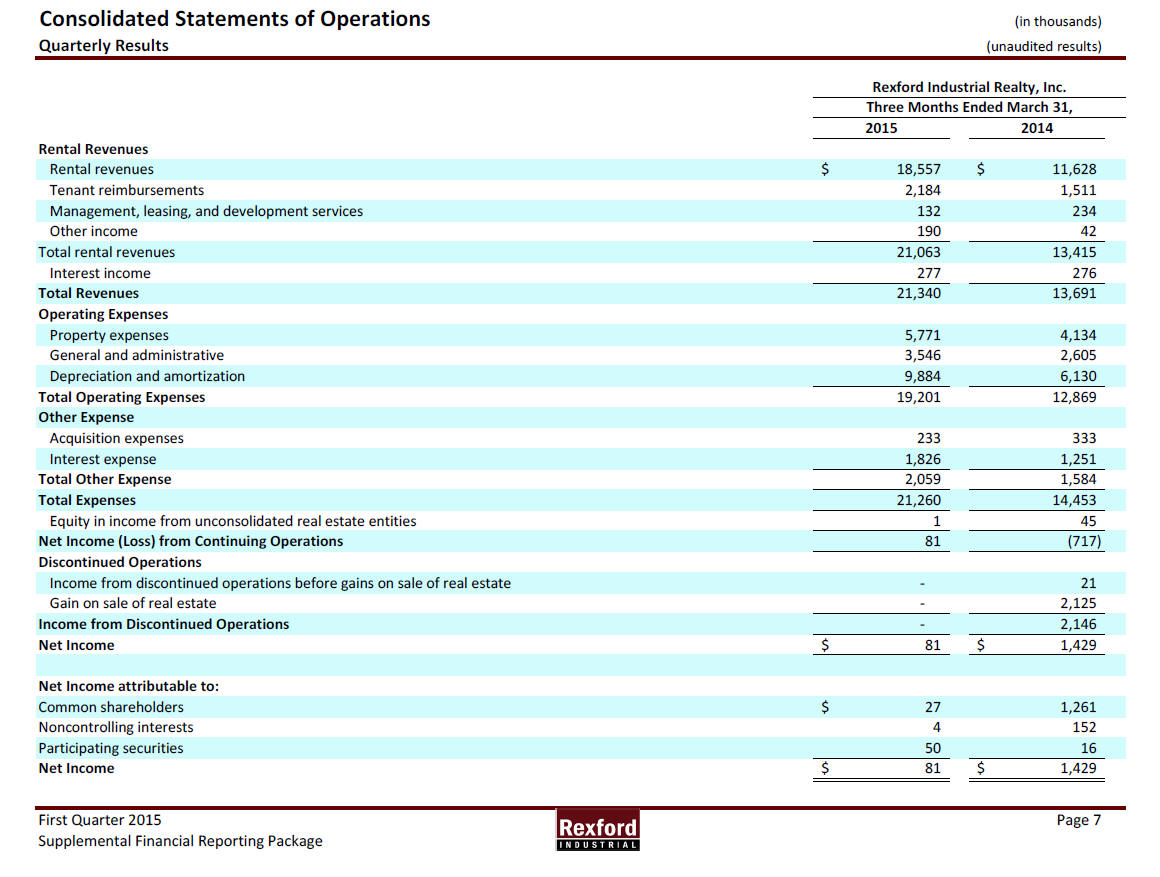

Consolidated Statements of Operations (in thousands) Quarterly Results (unaudited results) 2015 2014 Rental Revenues Rental revenues $ 18,557 $ 11,628 Tenant reimbursements 2,184 1,511 Management, leasing, and development services 132 234 Other income 190 42 Total rental revenues 21,063 13,415 Interest income 277 276 Total Revenues 21,340 13,691 Operating Expenses Property expenses 5,771 4,134 General and administrative 3,546 2,605 Depreciation and amortization 9,884 6,130 Total Operating Expenses 19,201 12,869 Other Expense Acquisition expenses 233 333 Interest expense 1,826 1,251 Total Other Expense 2,059 1,584 Total Expenses 21,260 14,453 Equity in income from unconsolidated real estate entities 1 45 Net Income (Loss) from Continuing Operations 81 (717) Discontinued Operations Income from discontinued operations before gains on sale of real estate - 21 Gain on sale of real estate - 2,125 Income from Discontinued Operations - 2,146 Net Income $ 81 $ 1,429 Net Income attributable to: Common shareholders $ 27 1,261 Noncontrolling interests 4 152 Participating securities 50 16 Net Income $ 81 $ 1,429 First Quarter 2015 Page 7 Supplemental Financial Reporting Package Rexford Industrial Realty, Inc. Three Months Ended March 31,

Non-GAAP FFO (1) (in thousands) (unaudited results) March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 March 31, 2014 Funds From Operations (FFO) Net Income (loss) $ 81 $ 145 $ (679) $ 81 $ 1,429 Add: Depreciation and amortization, including amounts in discontinued operations 9,884 8,443 8,032 6,003 6,137 Depreciation and amortization from unconsolidated joint ventures 2 8 66 103 103 8 5 Loss on sale of real estate - - 150 - - Deduct: Gain on sale of real estate - - - - 2,125 Gain on sale of real estate from unconsolidated joint ventures - 3 - - - FFO 9,993 8,651 7,606 6,187 5,526 Company share of FFO (2) $ 9,513 $ 8,145 $ 6,960 $ 5,508 $ 4,925 FFO per share - basic and diluted $ 0.19 $ 0.19 $ 0.21 $ 0.22 $ 0.19 FFO $ 9,993 $ 8,651 $ 7,606 $ 6,187 $ 5,526 Add: Non-recurring legal fees(3) 369 205 380 - - Acquisition Expenses 233 627 426 652 333 Recurring FFO $ 10,595 $ 9,483 $ 8,412 $ 6,839 $ 5,859 Company share of Recurring FFO (2) $ 10,085 $ 8,932 $ 7,700 $ 6,091 $ 5,223 Recurring FFO per share - basic and diluted $ 0.20 $ 0.21 $ 0.23 $ 0.24 $ 0.21 Weighted-average shares outstanding - basic and diluted 50,683,528 43,234,602 33,527,183 25,419,757 25,419,418 Weighted-average diluted shares and units 52,989,102 45,705,769 36,511,737 28,429,016 28,428,677 (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. (2) Company share of FFO is based on the weighted average interest in our operating partnership of 95.6%, 94.6%, 91.8%, 89.4% and 89.4% for the three months ended March 31, 2015, December 31, 2014, September 30, 2014, June 30, 2014 and March 31, 2014, respectively. Company share of FFO excludes FFO allocated to participating securities of $71, $38, $24, $24 and $16 for the three months ended March 31, 2015, December 31, 2014, September 30, 2014, June 30, 2014 and March 31, 2014, respectively. (3) Non-recurring legal fees relate to litigation. For more information, see Item 3. Legal Proceedings in our 2014 Annual Report on Form 10-K. First Quarter 2015 Page 8 Supplemental Financial Reporting Package Rexford Industrial Realty, Inc. Three Months Ended

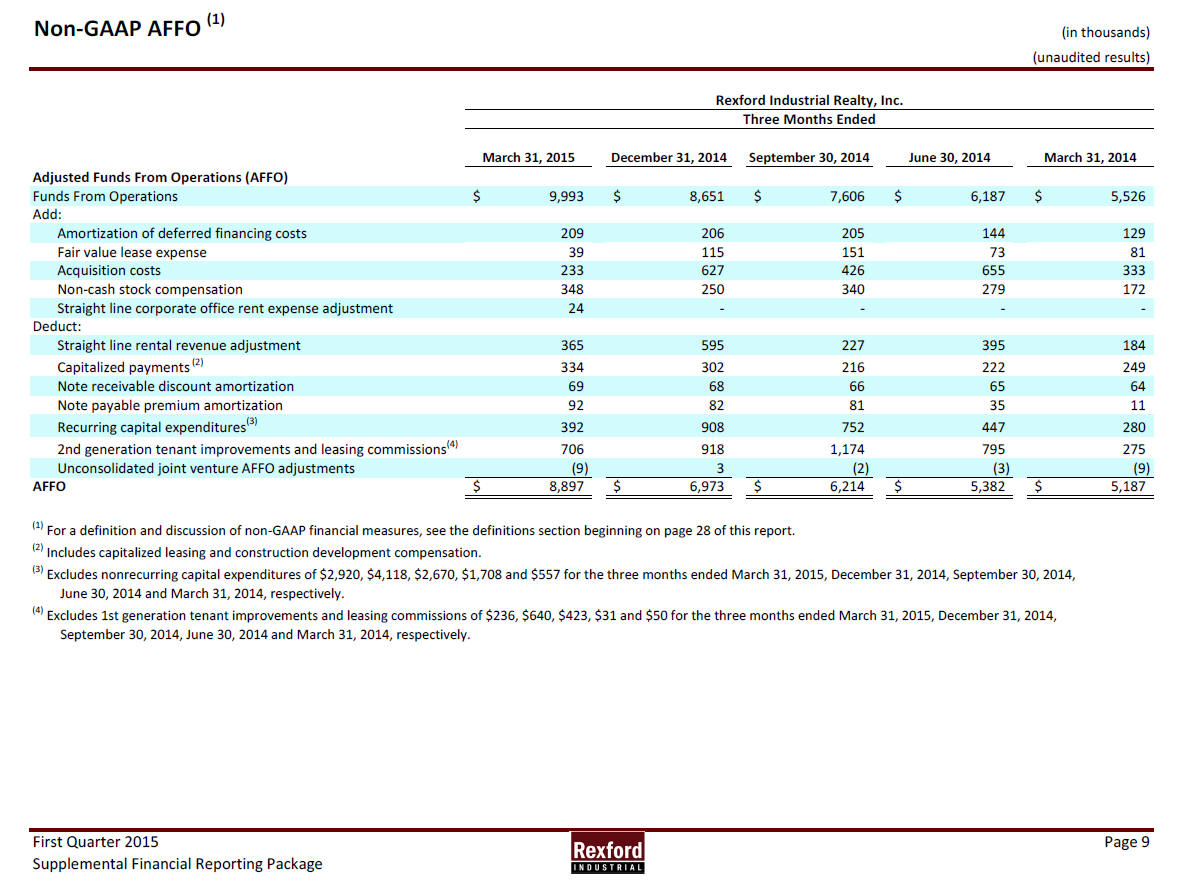

Non-GAAP AFFO (1) (in thousands) (unaudited results) March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 March 31, 2014 Adjusted Funds From Operations (AFFO) Funds From Operations $ 9,993 $ 8,651 $ 7,606 $ 6,187 $ 5,526 Add: Amortization of deferred financing costs 209 206 205 144 129 Fair value lease expense 39 115 151 73 81 Acquisition costs 233 627 426 655 333 Non-cash stock compensation 348 250 340 279 172 Straight line corporate office rent expense adjustment 24 - - - - Deduct: Straight line rental revenue adjustment 365 595 227 395 184 Capitalized payments (2) 334 302 216 222 249 Note receivable discount amortization 69 68 66 65 64 Note payable premium amortization 92 82 81 35 11 Recurring capital expenditures(3) 392 908 752 447 280 2nd generation tenant improvements and leasing commissions(4) 706 918 1,174 795 275 Unconsolidated joint venture AFFO adjustments (9) 3 (2) (3) (9) AFFO $ 8,897 $ 6,973 $ 6,214 $ 5,382 $ 5,187 (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. (2) Includes capitalized leasing and construction development compensation. (3) Excludes nonrecurring capital expenditures of $2,920, $4,118, $2,670, $1,708 and $557 for the three months ended March 31, 2015, December 31, 2014, September 30, 2014, June 30, 2014 and March 31, 2014, respectively. (4) Excludes 1st generation tenant improvements and leasing commissions of $236, $640, $423, $31 and $50 for the three months ended March 31, 2015, December 31, 2014, September 30, 2014, June 30, 2014 and March 31, 2014, respectively. First Quarter 2015 Page 9 Supplemental Financial Reporting Package Rexford Industrial Realty, Inc. Three Months Ended

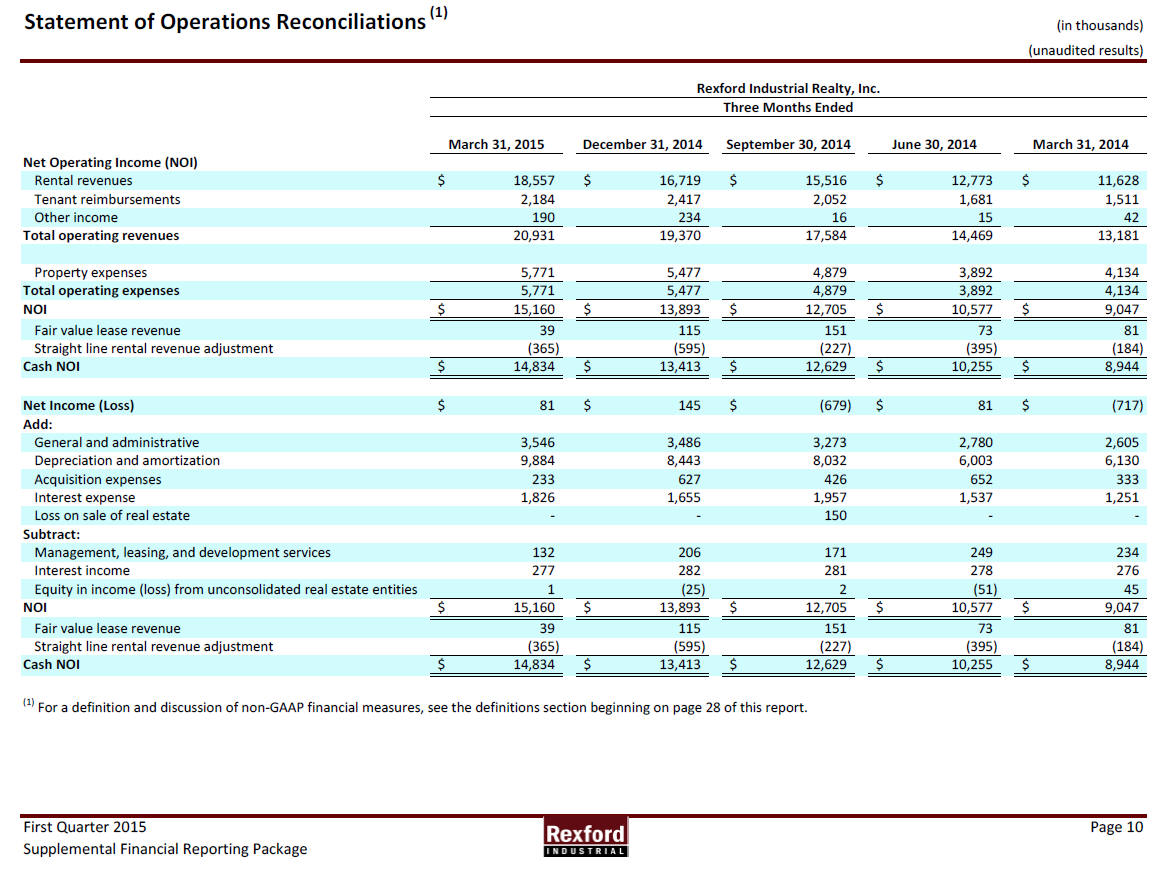

Statement of Operations Reconciliations (1) (in thousands) (unaudited results) March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 March 31, 2014 Net Operating Income (NOI) Rental revenues $ 18,557 $ 16,719 $ 15,516 $ 12,773 $ 1 1,628 Tenant reimbursements 2,184 2,417 2,052 1,681 1,511 Other income 190 234 16 15 4 2 Total operating revenues 20,931 19,370 17,584 14,469 13,181 Property expenses 5,771 5,477 4,879 3,892 4,134 Total operating expenses 5,771 5,477 4,879 3,892 4,134 NOI $ 15,160 $ 13,893 $ 12,705 $ 10,577 $ 9,047 Fair value lease revenue 3 9 115 151 7 3 8 1 Straight line rental revenue adjustment (365) (595) (227) (395) (184) Cash NOI $ 14,834 $ 13,413 $ 12,629 $ 10,255 $ 8,944 Net Income (Loss) $ 81 $ 145 $ (679) $ 81 $ (717) Add: General and administrative 3,546 3,486 3,273 2,780 2,605 Depreciation and amortization 9,884 8,443 8,032 6,003 6,130 Acquisition expenses 233 627 426 652 333 Interest expense 1,826 1,655 1,957 1,537 1,251 Loss on sale of real estate - - 150 - - Subtract: Management, leasing, and development services 132 206 171 249 234 Interest income 277 282 281 278 276 Equity in income (loss) from unconsolidated real estate entities 1 (25) 2 (51) 4 5 NOI $ 15,160 $ 13,893 $ 12,705 $ 10,577 $ 9,047 Fair value lease revenue 3 9 115 151 7 3 8 1 Straight line rental revenue adjustment (365) (595) (227) (395) (184) Cash NOI $ 14,834 $ 13,413 $ 12,629 $ 10,255 $ 8,944 (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. First Quarter 2015 Page 10 Supplemental Financial Reporting Package Rexford Industrial Realty, Inc. Three Months Ended

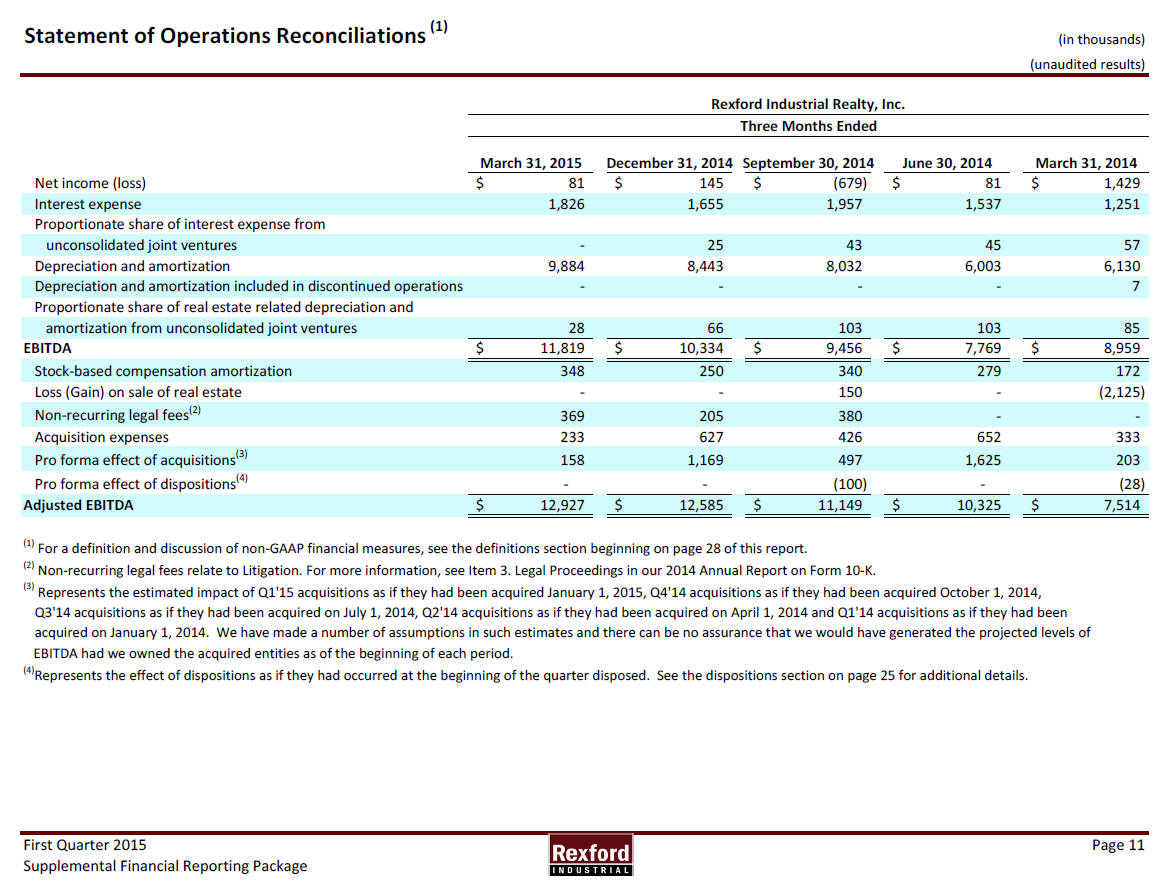

Statement of Operations Reconciliations (1) (in thousands) (unaudited results) March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 March 31, 2014 Net income (loss) $ 81 $ 145 $ (679) $ 81 $ 1 ,429 Interest expense 1,826 1,655 1,957 1,537 1,251 Proportionate share of interest expense from unconsolidated joint ventures - 25 43 45 57 Depreciation and amortization 9,884 8,443 8,032 6,003 6,130 Depreciation and amortization included in discontinued operations - - - - 7 Proportionate share of real estate related depreciation and amortization from unconsolidated joint ventures 28 66 103 103 85 EBITDA $ 11,819 $ 10,334 $ 9,456 $ 7,769 $ 8 ,959 Stock-based compensation amortization 348 250 340 279 172 Loss (Gain) on sale of real estate - - 150 - (2,125) Non-recurring legal fees(2) 369 205 380 - - Acquisition expenses 233 627 426 652 333 Pro forma effect of acquisitions(3) 158 1,169 497 1,625 203 Pro forma effect of dispositions(4) - - (100) - (28) Adjusted EBITDA $ 12,927 $ 12,585 $ 11,149 $ 10,325 $ 7 ,514 (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. (2) Non-recurring legal fees relate to Litigation. For more information, see Item 3. Legal Proceedings in our 2014 Annual Report on Form 10-K. (3) Represents the estimated impact of Q1'15 acquisitions as if they had been acquired January 1, 2015, Q4'14 acquisitions as if they had been acquired October 1, 2014, Q3'14 acquisitions as if they had been acquired on July 1, 2014, Q2'14 acquisitions as if they had been acquired on April 1, 2014 and Q1'14 acquisitions as if they had been acquired on January 1, 2014. We have made a number of assumptions in such estimates and there can be no assurance that we would have generated the projected levels of EBITDA had we owned the acquired entities as of the beginning of each period. (4)Represents the effect of dispositions as if they had occurred at the beginning of the quarter disposed. See the dispositions section on page 25 for additional details. First Quarter 2015 Page 11 Supplemental Financial Reporting Package Rexford Industrial Realty, Inc. Three Months Ended

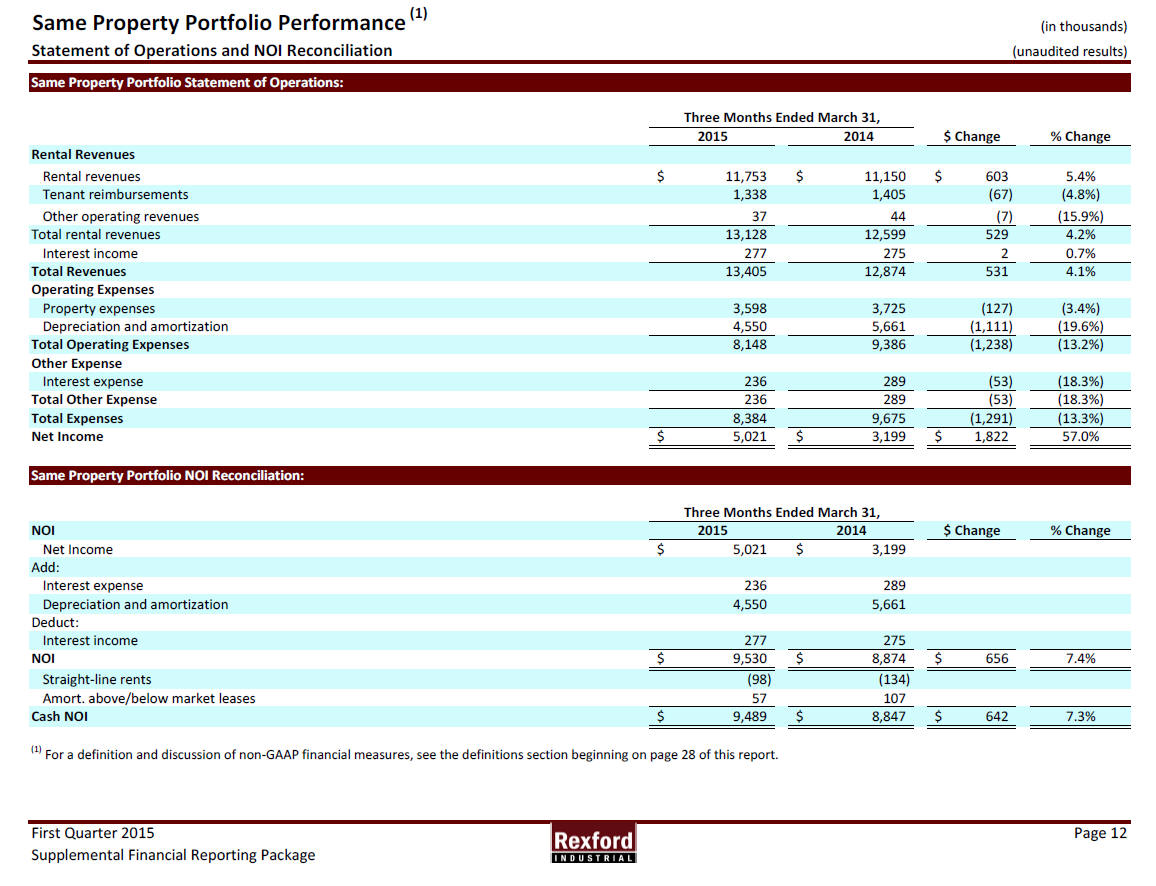

Same Property Portfolio Performance (1) (in thousands) Statement of Operations and NOI Reconciliation (unaudited results) Same Property Portfolio Statement of Operations: 2015 2014 $ Change % Change Rental Revenues Rental revenues $ 11,753 $ 11,150 $ 603 5.4% Tenant reimbursements 1,338 1,405 (67) (4.8%) Other operating revenues 37 44 (7) (15.9%) Total rental revenues 13,128 12,599 529 4.2% Interest income 277 275 2 0.7% Total Revenues 13,405 12,874 531 4.1% Operating Expenses Property expenses 3,598 3,725 (127) (3.4%) Depreciation and amortization 4,550 5,661 (1,111) (19.6%) Total Operating Expenses 8,148 9,386 (1,238) (13.2%) Other Expense Interest expense 236 289 (53) (18.3%) Total Other Expense 236 289 (53) (18.3%) Total Expenses 8,384 9,675 (1,291) (13.3%) Net Income $ 5,021 $ 3,199 $ 1,822 57.0% Same Property Portfolio NOI Reconciliation: NOI 2015 2014 $ Change % Change Net Income $ 5,021 $ 3,199 Add: Interest expense 236 289 Depreciation and amortization 4,550 5,661 Deduct: Interest income 277 275 NOI $ 9,530 $ 8,874 $ 656 7.4% Straight-line rents (98) (134) Amort. above/below market leases 57 107 Cash NOI $ 9,489 $ 8,847 $ 642 7.3% (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. First Quarter 2015 Page 12 Supplemental Financial Reporting Package Three Months Ended March 31, Three Months Ended March 31,

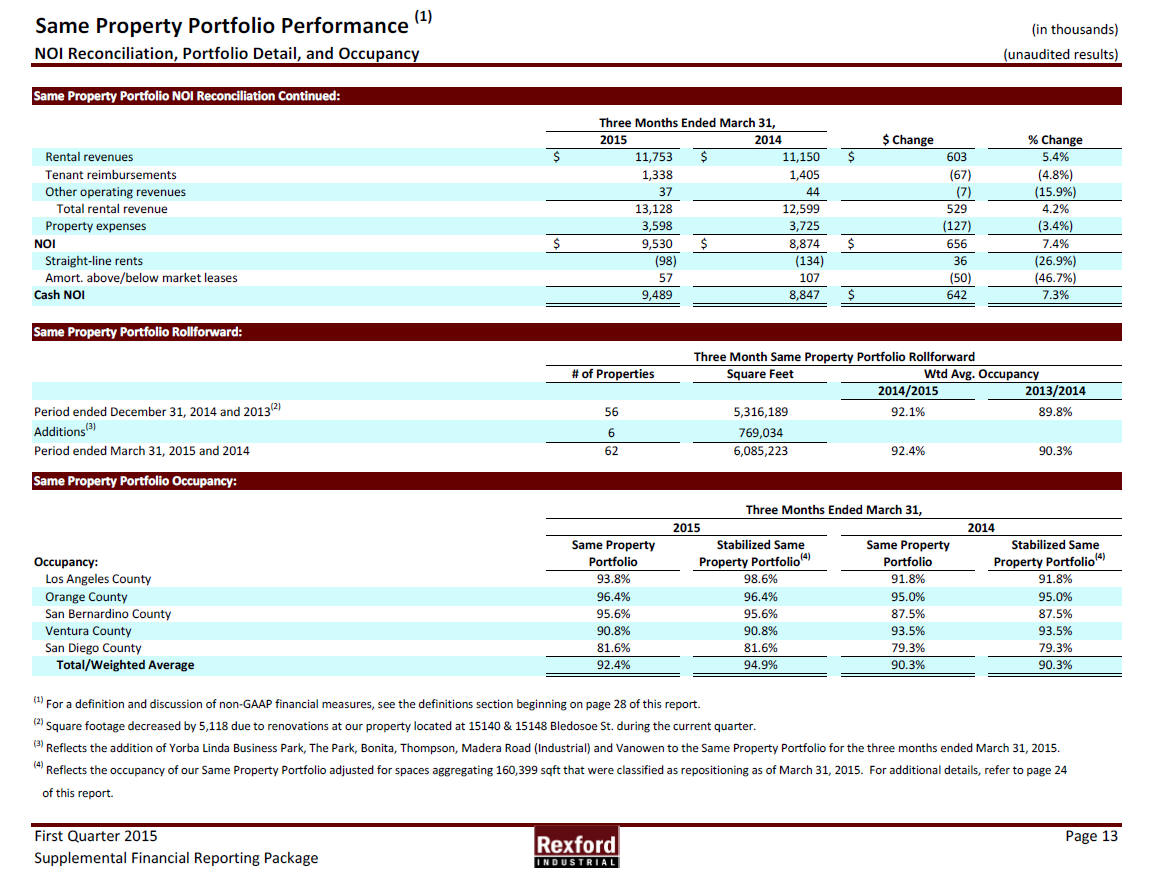

Same Property Portfolio Performance (1) (in thousands) NOI Reconciliation, Portfolio Detail, and Occupancy (unaudited results) Same Property Portfolio NOI Reconciliation Continued: 2015 2014 $ Change % Change Rental revenues $ 11,753 $ 11,150 $ 603 5.4% Tenant reimbursements 1,338 1,405 (67) (4.8%) Other operating revenues 37 44 (7) (15.9%) Total rental revenue 13,128 12,599 529 4.2% Property expenses 3,598 3,725 (127) (3.4%) NOI $ 9,530 $ 8,874 $ 656 7.4% Straight-line rents (98) (134) 36 (26.9%) Amort. above/below market leases 57 107 (50) (46.7%) Cash NOI 9,489 8,847 $ 642 7.3% Same Property Portfolio Rollforward: # of Properties Square Feet 2014/2015 2013/2014 Period ended December 31, 2014 and 2013(2) 56 5,316,189 92.1% 89.8% Additions(3) 6 769,034 Period ended March 31, 2015 and 2014 62 6,085,223 92.4% 90.3% Same Property Portfolio Occupancy: Same Property Stabilized Same Same Property Stabilized Same Occupancy: Portfolio Portfolio Los Angeles County 93.8% 98.6% 91.8% 91.8% Orange County 96.4% 96.4% 95.0% 95.0% San Bernardino County 95.6% 95.6% 87.5% 87.5% Ventura County 90.8% 90.8% 93.5% 93.5% San Diego County 81.6% 81.6% 79.3% 79.3% Total/Weighted Average 92.4% 94.9% 90.3% 90.3% (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. (2) Square footage decreased by 5,118 due to renovations at our property located at 15140 & 15148 Bledosoe St. during the current quarter. (3) Reflects the addition of Yorba Linda Business Park, The Park, Bonita, Thompson, Madera Road (Industrial) and Vanowen to the Same Property Portfolio for the three months ended March 31, 2015. (4) Reflects the occupancy of our Same Property Portfolio adjusted for spaces aggregating 160,399 sqft that were classified as repositioning as of March 31, 2015. For additional details, refer to page 24 of this report. First Quarter 2015 Page 13 Supplemental Financial Reporting Package Property Portfolio(4) Property Portfolio(4) 2014 Three Months Ended March 31, 2015 Three Months Ended March 31, Three Month Same Property Portfolio Rollforward Wtd Avg. Occupancy

Joint Venture Financial Summary (in thousands) Balance Sheet (unaudited results) March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 Assets: Investments in real estate, net $ 20,635 $ 20,268 $ 56,488 56,439 Cash and cash equivalents 2,573 2,331 1,105 427 Rents and other receivables, net 220 231 309 182 Deferred rent receivable - - 251 212 Deferred leasing costs and acquisition related intangible assets, net 164 290 4,211 4,569 Deferred loan costs, net - - 79 106 Acquired above-market leases, net 44 110 557 646 Other assets 28 19 54 64 Total Assets $ 23,664 $ 23,249 $ 63,054 62,645 Liabilities: Notes payable $ - $ - $ 41,500 $ 41,500 Accounts payable, accrued expenses and other liabilities 930 678 930 727 Deferred rent payable 4 11 - - Tenant security deposits 292 292 277 277 Prepaid rents 129 - 127 124 Total Liabilities 1,355 981 42,834 42,628 Equity: Equity 8,202 8,202 19,462 19,462 Accumulated deficit and distributions 14,107 14,066 758 555 Total Equity 22,309 22,268 20,220 20,017 Total Liabilities and Equity $ 23,664 $ 23,249 $ 63,054 $ 62,645 Rexford Industrial Realty, Inc. Ownership %: 15% 15% 15% 15% (1) These financials represent amounts attributable to the entities and do not represent our proportionate share. First Quarter 2015 Page 14 Supplemental Financial Reporting Package Mission Oaks (1)

Joint Venture Financial Summary (1) (in thousands) Statement of Operations (unaudited results) Statement of Operations: March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 Income Statement Rental revenues $ 348 $ 807 $ 1,300 $ 1,291 Tenant reimbursements 315 355 823 630 Other operating revenues - - - - Total revenue 663 1,162 2,123 1,921 Total operating expense 425 555 934 745 NOI 238 607 1,189 1,176 General and administrative 12 11 14 28 Depreciation and amortization 185 442 687 686 Interest expense - 165 285 299 Loss on Extinguishment of Debt - 70 - - Gain on sale of assets/investments - (13,389) - - Total expense 622 (12,146) 1,920 1,758 Net Income $ 41 $ 13,308 $ 203 $ 163 EBITDA Net income $ 41 $ 13,308 $ 203 $ 163 Interest expense - 165 285 299 Depreciation and amortization 185 442 687 686 EBITDA $ 226 $ 13,915 $ 1,175 $ 1,148 Rexford Industrial Realty, Inc. Ownership %: 15% 15% 15% 15% Reconciliation - Equity Income in Joint Venture: Net income $ 41 $ 13,308 $ 203 $ 163 Rexford Industrial Realty, Inc. Ownership %: 15% 15% 15% 15% Company share 6 1,996 30 24 Intercompany eliminations/basis adjustments (5) (2,021) (28) (75) Equity in net income from unconsolidated real estate entities $ 1 $ (25) $ 2 $ (51) (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. (2) These financials represent amounts attributable to the entities and do not represent our proportionate share. First Quarter 2015 Page 15 Supplemental Financial Reporting Package Mission Oaks (2) Three Months Ended

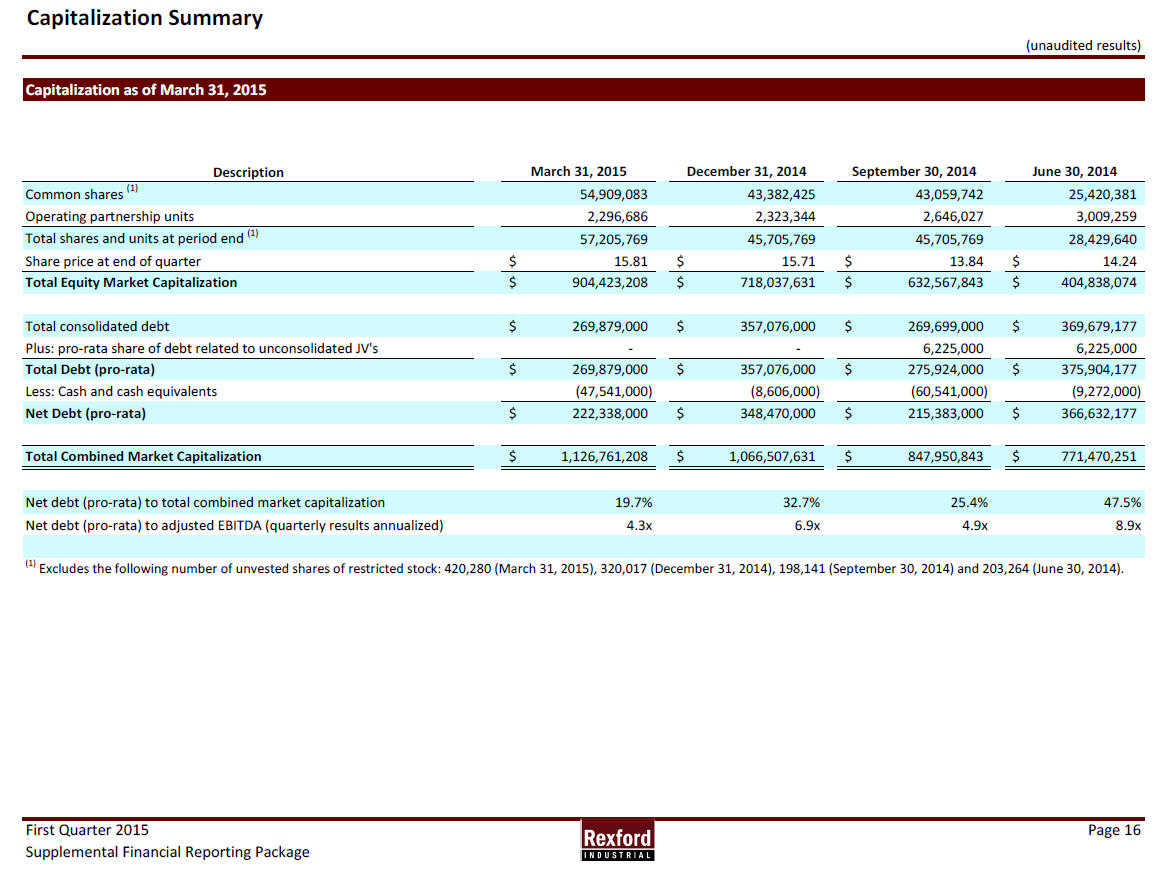

Capitalization Summary (unaudited results) Capitalization as of March 31, 2015 Description March 31, 2015 December 31, 2014 September 30, 2014 June 30, 2014 Common shares (1) 54,909,083 43,382,425 43,059,742 25,420,381 Operating partnership units 2 ,296,686 2,323,344 2,646,027 3,009,259 Total shares and units at period end (1) 57,205,769 45,705,769 45,705,769 28,429,640 Share price at end of quarter $ 15.81 $ 15.71 $ 13.84 $ 14.24 Total Equity Market Capitalization $ 904,423,208 $ 718,037,631 $ 632,567,843 $ 404,838,074 Total consolidated debt $ 269,879,000 $ 357,076,000 $ 269,699,000 $ 369,679,177 Plus: pro-rata share of debt related to unconsolidated JV's - - 6,225,000 6,225,000 Total Debt (pro-rata) $ 269,879,000 $ 357,076,000 $ 275,924,000 $ 375,904,177 Less: Cash and cash equivalents (47,541,000) (8,606,000) (60,541,000) (9,272,000) Net Debt (pro-rata) $ 222,338,000 $ 348,470,000 $ 215,383,000 $ 366,632,177 Total Combined Market Capitalization $ 1,126,761,208 $ 1,066,507,631 $ 847,950,843 $ 771,470,251 Net debt (pro-rata) to total combined market capitalization 19.7% 32.7% 25.4% 47.5% Net debt (pro-rata) to adjusted EBITDA (quarterly results annualized) 4.3x 6.9x 4.9x 8.9x (1) Excludes the following number of unvested shares of restricted stock: 420,280 (March 31, 2015), 320,017 (December 31, 2014), 198,141 (September 30, 2014) and 203,264 (June 30, 2014). First Quarter 2015 Page 16 Supplemental Financial Reporting Package

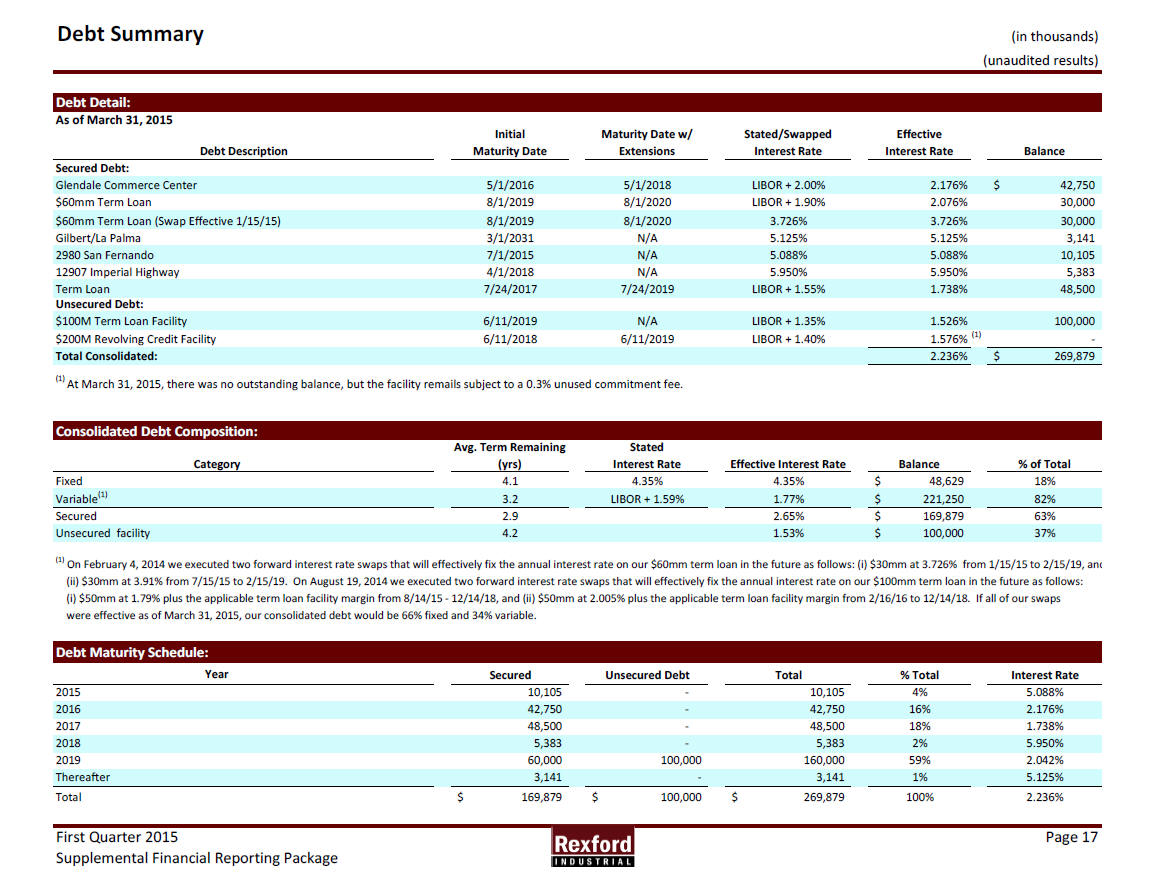

Debt Summary (in thousands) (unaudited results) Debt Detail: As of March 31, 2015 Debt Description Initial Maturity Date Maturity Date w/ Extensions Stated/Swapped Interest Rate Effective Interest Rate Balance Secured Debt: Glendale Commerce Center 5/1/2016 5/1/2018 LIBOR + 2.00% 2.176% $ 42,750 $60mm Term Loan 8/1/2019 8/1/2020 LIBOR + 1.90% 2.076% 30,000 $60mm Term Loan (Swap Effective 1/15/15) 8/1/2019 8/1/2020 3.726% 3.726% 30,000 Gilbert/La Palma 3/1/2031 N/A 5.125% 5.125% 3,141 2980 San Fernando 7/1/2015 N/A 5.088% 5.088% 10,105 12907 Imperial Highway 4/1/2018 N/A 5.950% 5.950% 5,383 Term Loan 7/24/2017 7/24/2019 LIBOR + 1.55% 1.738% 48,500 Unsecured Debt: $100M Term Loan Facility 6/11/2019 N/A LIBOR + 1.35% 1.526% 100,000 $200M Revolving Credit Facility 6/11/2018 6/11/2019 LIBOR + 1.40% 1.576% (1) - Total Consolidated: 2.236% $ 269,879 (1) At March 31, 2015, there was no outstanding balance, but the facility remails subject to a 0.3% unused commitment fee. Consolidated Debt Composition: Category Avg. Term Remaining (yrs) Stated Interest Rate Effective Interest Rate Balance % of Total Fixed 4.1 4.35% 4.35% $ 4 8,629 18% Variable(1) 3.2 LIBOR + 1.59% 1.77% $ 221,250 82% Secured 2.9 2.65% $ 169,879 63% Unsecured facility 4.2 1.53% $ 100,000 37% (1) On February 4, 2014 we executed two forward interest rate swaps that will effectively fix the annual interest rate on our $60mm term loan in the future as follows: (i) $30mm at 3.726% from 1/15/15 to 2/15/19, and (ii) $30mm at 3.91% from 7/15/15 to 2/15/19. On August 19, 2014 we executed two forward interest rate swaps that will effectively fix the annual interest rate on our $100mm term loan in the future as follows: (i) $50mm at 1.79% plus the applicable term loan facility margin from 8/14/15 - 12/14/18, and (ii) $50mm at 2.005% plus the applicable term loan facility margin from 2/16/16 to 12/14/18. If all of our swaps were effective as of March 31, 2015, our consolidated debt would be 66% fixed and 34% variable. Debt Maturity Schedule: Year Secured Unsecured Debt Total % Total Interest Rate 2015 10,105 - 10,105 4% 5.088% 2016 42,750 - 42,750 16% 2.176% 2017 48,500 - 48,500 18% 1.738% 2018 5,383 - 5,383 2% 5.950% 2019 60,000 100,000 160,000 59% 2.042% Thereafter 3,141 - 3,141 1% 5.125% Total $ 169,879 $ 100,000 $ 2 69,879 100% 2.236% First Quarter 2015 Page 17 Supplemental Financial Reporting Package

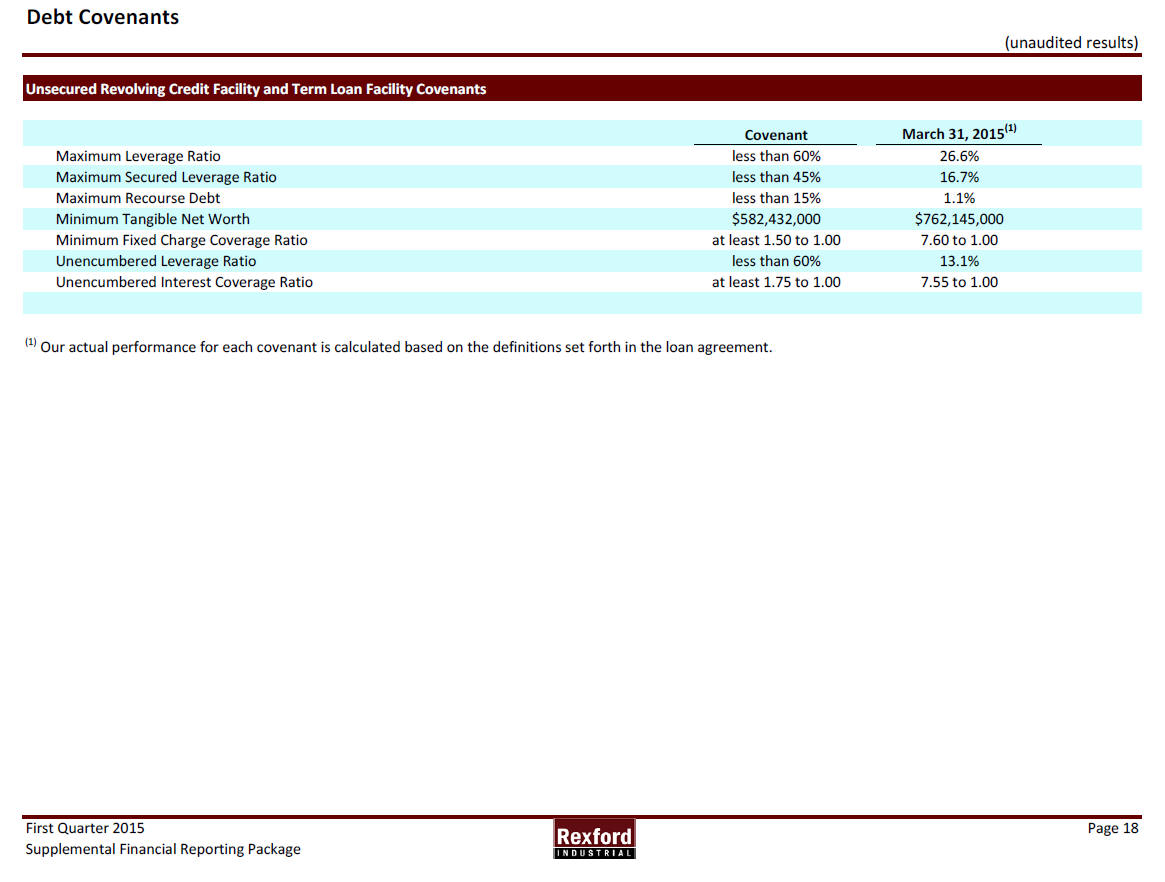

Debt Covenants (unaudited results) Unsecured Revolving Credit Facility and Term Loan Facility Covenants Covenant March 31, 2015(1) Maximum Leverage Ratio less than 60% 26.6% Maximum Secured Leverage Ratio less than 45% 16.7% Maximum Recourse Debt less than 15% 1.1% Minimum Tangible Net Worth $582,432,000 $762,145,000 Minimum Fixed Charge Coverage Ratio at least 1.50 to 1.00 7.60 to 1.00 Unencumbered Leverage Ratio less than 60% 13.1% Unencumbered Interest Coverage Ratio at least 1.75 to 1.00 7.55 to 1.00 (1) Our actual performance for each covenant is calculated based on the definitions set forth in the loan agreement. First Quarter 2015 Page 18 Supplemental Financial Reporting Package

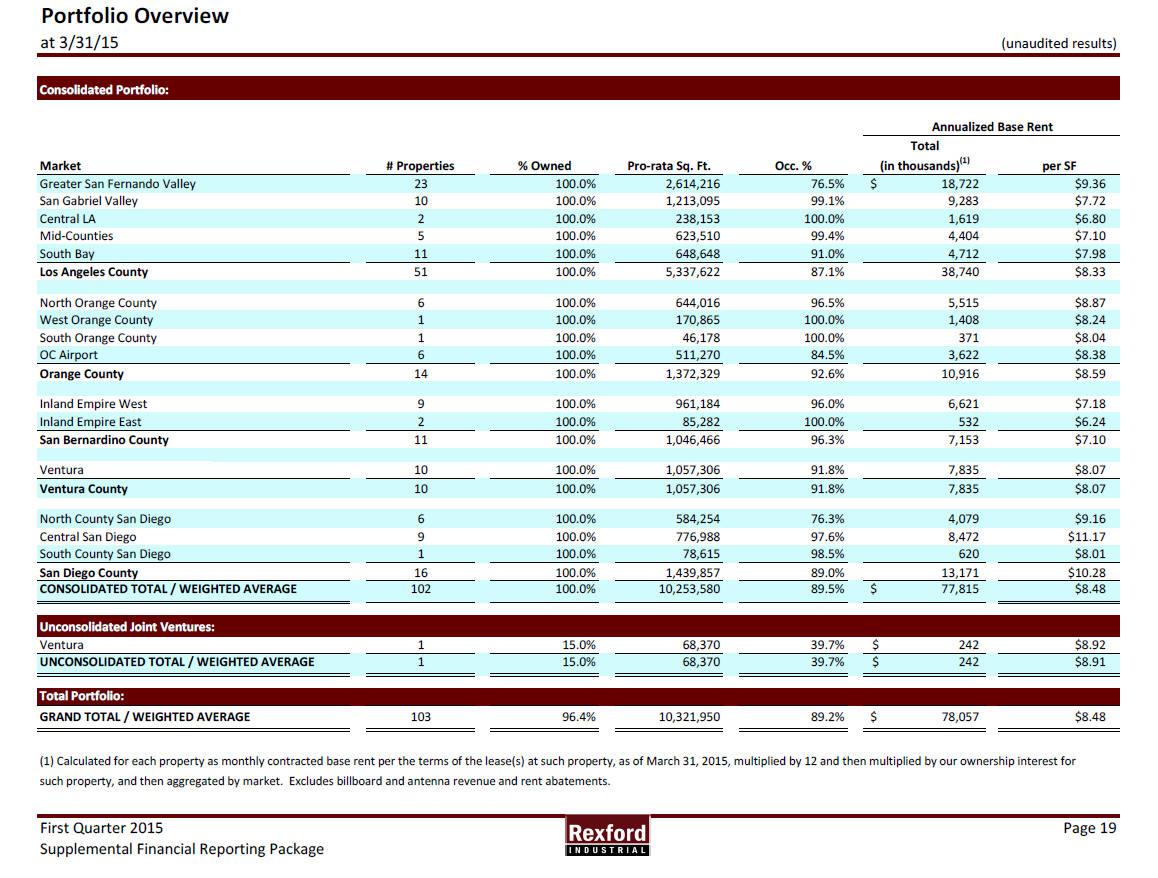

Portfolio Overview at 3/31/15 (unaudited results) Consolidated Portfolio: Annualized Base Rent Market # Properties % Owned Pro-rata Sq. Ft. Occ. % Total (in thousands)(1) per SF Greater San Fernando Valley 23 100.0% 2,614,216 76.5% $ 18,722 $9.36 San Gabriel Valley 10 100.0% 1,213,095 99.1% 9,283 $7.72 Central LA 2 100.0% 238,153 100.0% 1,619 $6.80 Mid-Counties 5 100.0% 623,510 99.4% 4,404 $7.10 South Bay 11 100.0% 648,648 91.0% 4,712 $7.98 Los Angeles County 51 100.0% 5,337,622 87.1% 38,740 $8.33 North Orange County 6 100.0% 644,016 96.5% 5,515 $8.87 West Orange County 1 100.0% 170,865 100.0% 1,408 $8.24 South Orange County 1 100.0% 46,178 100.0% 371 $8.04 OC Airport 6 100.0% 511,270 84.5% 3,622 $8.38 Orange County 14 100.0% 1,372,329 92.6% 10,916 $8.59 Inland Empire West 9 100.0% 961,184 96.0% 6,621 $7.18 Inland Empire East 2 100.0% 85,282 100.0% 532 $6.24 San Bernardino County 11 100.0% 1,046,466 96.3% 7,153 $7.10 Ventura 10 100.0% 1,057,306 91.8% 7,835 $8.07 Ventura County 10 100.0% 1,057,306 91.8% 7,835 $8.07 North County San Diego 6 100.0% 584,254 76.3% 4,079 $9.16 Central San Diego 9 100.0% 776,988 97.6% 8,472 $11.17 South County San Diego 1 100.0% 78,615 98.5% 620 $8.01 San Diego County 16 100.0% 1,439,857 89.0% 13,171 $10.28 CONSOLIDATED TOTAL / WEIGHTED AVERAGE 102 100.0% 10,253,580 89.5% $ 77,815 $8.48 Unconsolidated Joint Ventures: Ventura 1 15.0% 68,370 39.7% $ 242 $8.92 UNCONSOLIDATED TOTAL / WEIGHTED AVERAGE 1 15.0% 68,370 39.7% $ 242 $8.91 Total Portfolio: GRAND TOTAL / WEIGHTED AVERAGE 103 96.4% 10,321,950 89.2% $ 78,057 $8.48 (1) Calculated for each property as monthly contracted base rent per the terms of the lease(s) at such property, as of March 31, 2015, multiplied by 12 and then multiplied by our ownership interest for such property, and then aggregated by market. Excludes billboard and antenna revenue and rent abatements. First Quarter 2015 Page 19 Supplemental Financial Reporting Package

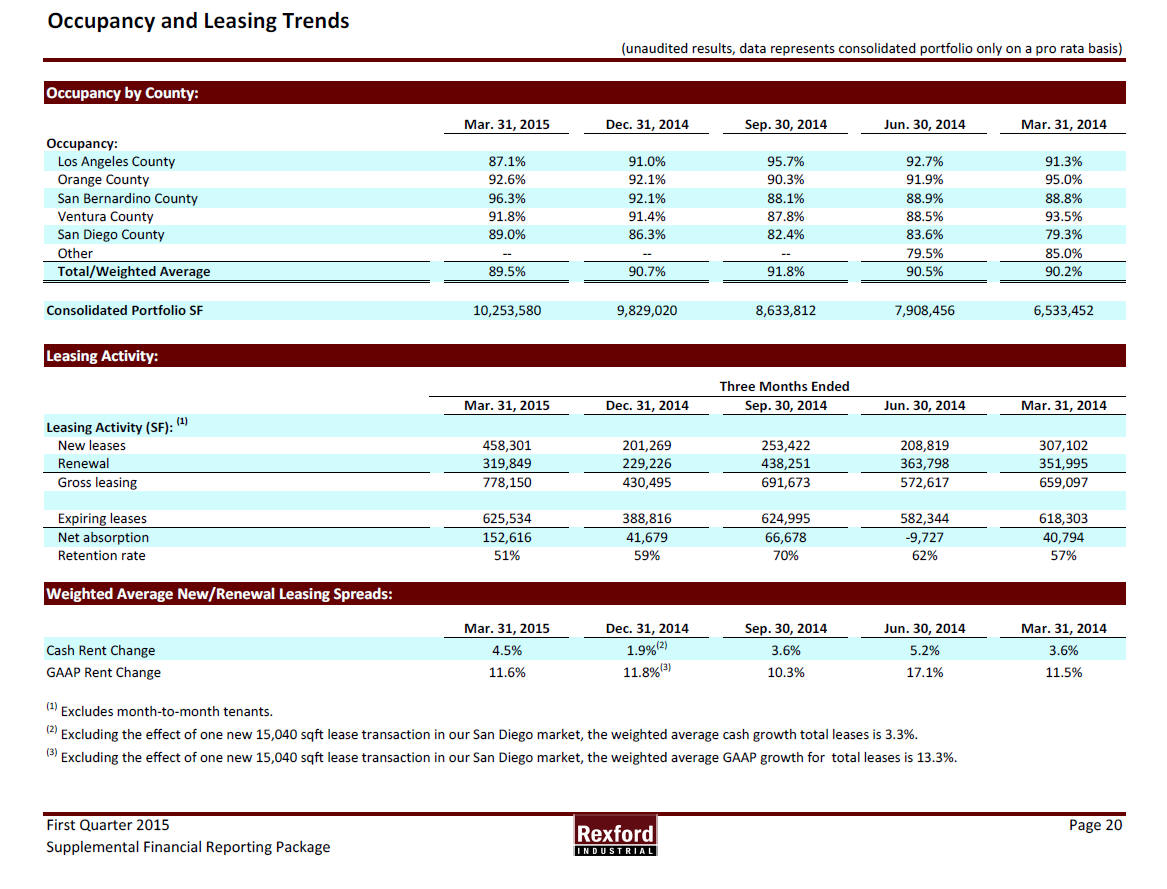

Occupancy and Leasing Trends (unaudited results, data represents consolidated portfolio only on a pro rata basis) Occupancy by County: Mar. 31, 2015 Dec. 31, 2014 Sep. 30, 2014 Jun. 30, 2014 Mar. 31, 2014 Occupancy: Los Angeles County 87.1% 91.0% 95.7% 92.7% 91.3% Orange County 92.6% 92.1% 90.3% 91.9% 95.0% San Bernardino County 96.3% 92.1% 88.1% 88.9% 88.8% Ventura County 91.8% 91.4% 87.8% 88.5% 93.5% San Diego County 89.0% 86.3% 82.4% 83.6% 79.3% Other -- -- -- 79.5% 85.0% Total/Weighted Average 89.5% 90.7% 91.8% 90.5% 90.2% Consolidated Portfolio SF 10,253,580 9,829,020 8,633,812 7,908,456 6,533,452 Leasing Activity: Mar. 31, 2015 Dec. 31, 2014 Sep. 30, 2014 Jun. 30, 2014 Mar. 31, 2014 Leasing Activity (SF): (1) New leases 458,301 201,269 253,422 208,819 307,102 Renewal 319,849 229,226 438,251 363,798 351,995 Gross leasing 778,150 430,495 691,673 572,617 659,097 Expiring leases 625,534 388,816 624,995 582,344 618,303 Net absorption 152,616 41,679 66,678 -9,727 40,794 Retention rate 51% 59% 70% 62% 57% Weighted Average New/Renewal Leasing Spreads: Mar. 31, 2015 Dec. 31, 2014 Sep. 30, 2014 Jun. 30, 2014 Mar. 31, 2014 Cash Rent Change 4.5% 1.9%(2) 3.6% 5.2% 3.6% GAAP Rent Change 11.6% 11.8%(3) 10.3% 17.1% 11.5% (1) Excludes month-to-month tenants. (2) Excluding the effect of one new 15,040 sqft lease transaction in our San Diego market, the weighted average cash growth total leases is 3.3%. (3) Excluding the effect of one new 15,040 sqft lease transaction in our San Diego market, the weighted average GAAP growth for total leases is 13.3%. First Quarter 2015 Page 20 Supplemental Financial Reporting Package Three Months Ended

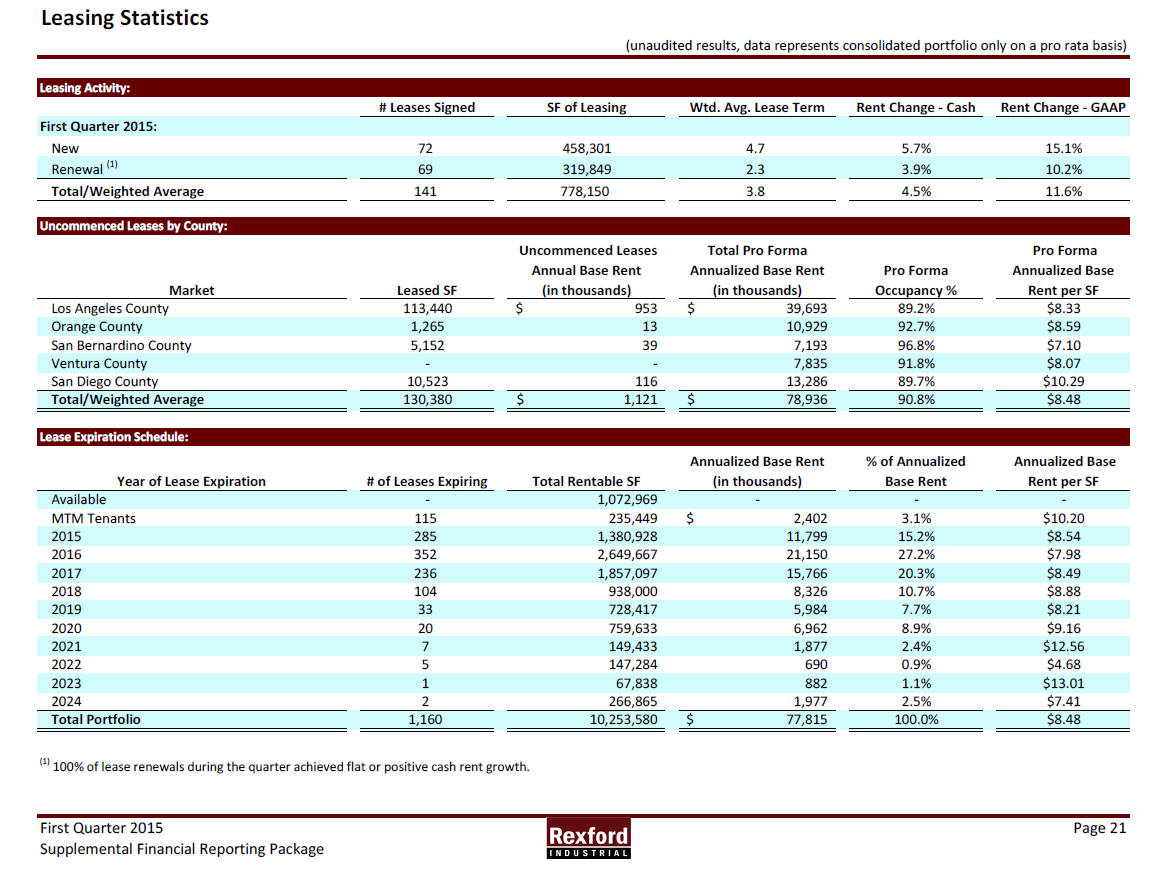

Leasing Statistics (unaudited results, data represents consolidated portfolio only on a pro rata basis) Leasing Activity: # Leases Signed SF of Leasing Wtd. Avg. Lease Term Rent Change - Cash Rent Change - GAAP First Quarter 2015: New 72 458,301 4.7 5.7% 15.1% Renewal (1) 69 319,849 2.3 3.9% 10.2% Total/Weighted Average 141 778,150 3.8 4.5% 11.6% Uncommenced Leases by County: Market Leased SF Uncommenced Leases Annual Base Rent (in thousands) Total Pro Forma Annualized Base Rent (in thousands) Pro Forma Occupancy % Pro Forma Annualized Base Rent per SF Los Angeles County 113,440 $ 953 $ 39,693 89.2% $8.33 Orange County 1,265 13 10,929 92.7% $8.59 San Bernardino County 5,152 39 7,193 96.8% $7.10 Ventura County - - 7,835 91.8% $8.07 San Diego County 10,523 116 13,286 89.7% $10.29 Total/Weighted Average 130,380 $ 1,121 $ 78,936 90.8% $8.48 Lease Expiration Schedule: Year of Lease Expiration # of Leases Expiring Total Rentable SF Annualized Base Rent (in thousands) % of Annualized Base Rent Annualized Base Rent per SF Available - 1,072,969 - - - MTM Tenants 115 235,449 $ 2,402 3.1% $10.20 2015 285 1,380,928 11,799 15.2% $8.54 2016 352 2,649,667 21,150 27.2% $7.98 2017 236 1,857,097 15,766 20.3% $8.49 2018 104 938,000 8,326 10.7% $8.88 2019 33 728,417 5,984 7.7% $8.21 2020 20 759,633 6,962 8.9% $9.16 2021 7 149,433 1,877 2.4% $12.56 2022 5 147,284 690 0.9% $4.68 2023 1 67,838 882 1.1% $13.01 2024 2 266,865 1,977 2.5% $7.41 Total Portfolio 1,160 10,253,580 $ 77,815 100.0% $8.48 (1) 100% of lease renewals during the quarter achieved flat or positive cash rent growth. First Quarter 2015 Page 21 Supplemental Financial Reporting Package

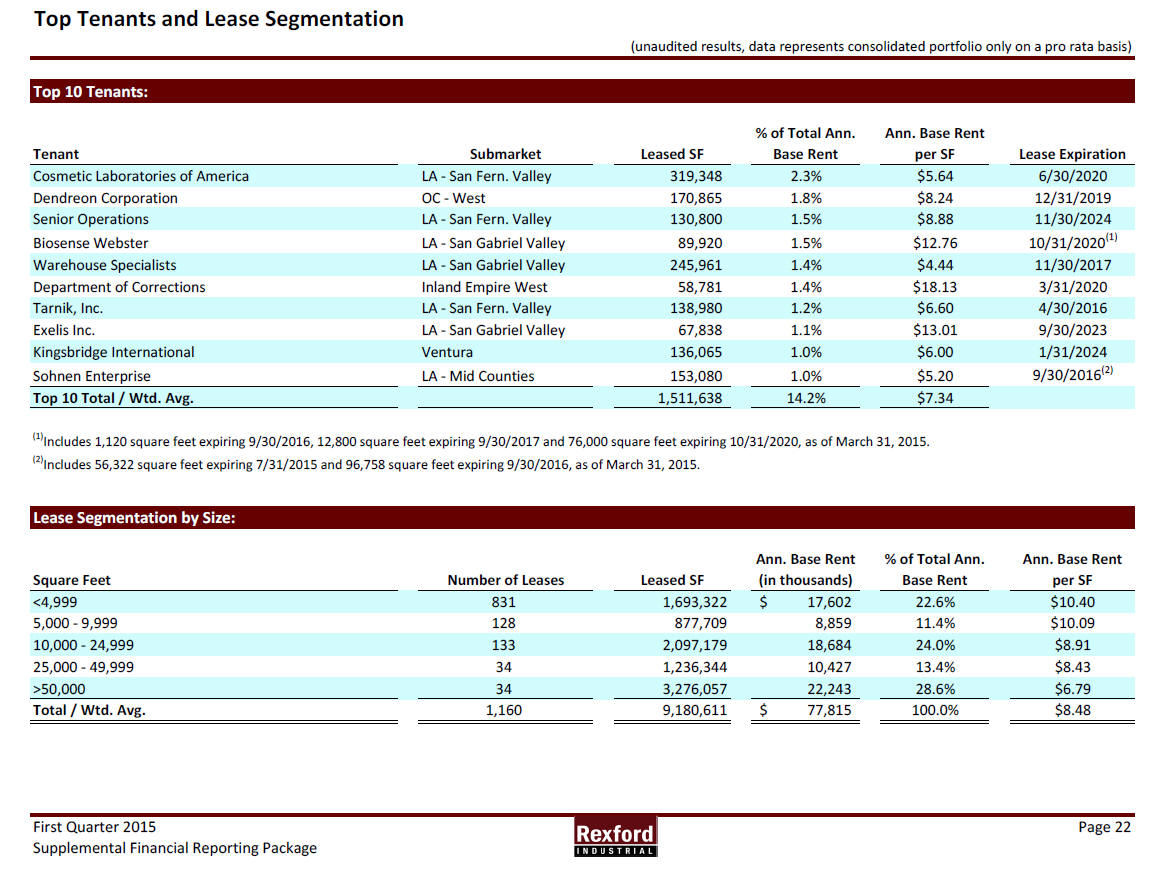

Top Tenants and Lease Segmentation (unaudited results, data represents consolidated portfolio only on a pro rata basis) Top 10 Tenants: Tenant Submarket Leased SF % of Total Ann. Base Rent Ann. Base Rent per SF Lease Expiration Cosmetic Laboratories of America LA - San Fern. Valley 319,348 2.3% $5.64 6/30/2020 Dendreon Corporation OC - West 170,865 1.8% $8.24 12/31/2019 Senior Operations LA - San Fern. Valley 130,800 1.5% $8.88 11/30/2024 Biosense Webster LA - San Gabriel Valley 89,920 1.5% $12.76 10/31/2020(1) Warehouse Specialists LA - San Gabriel Valley 245,961 1.4% $4.44 11/30/2017 Department of Corrections Inland Empire West 58,781 1.4% $18.13 3/31/2020 Tarnik, Inc. LA - San Fern. Valley 138,980 1.2% $6.60 4/30/2016 Exelis Inc. LA - San Gabriel Valley 67,838 1.1% $13.01 9/30/2023 Kingsbridge International Ventura 136,065 1.0% $6.00 1/31/2024 Sohnen Enterprise LA - Mid Counties 153,080 1.0% $5.20 9/30/2016(2) Top 10 Total / Wtd. Avg. 1,511,638 14.2% $7.34 (1)Includes 1,120 square feet expiring 9/30/2016, 12,800 square feet expiring 9/30/2017 and 76,000 square feet expiring 10/31/2020, as of March 31, 2015. (2)Includes 56,322 square feet expiring 7/31/2015 and 96,758 square feet expiring 9/30/2016, as of March 31, 2015. Lease Segmentation by Size: Square Feet Number of Leases Leased SF Ann. Base Rent (in thousands) % of Total Ann. Base Rent Ann. Base Rent per SF <4,999 831 1,693,322 $ 17,602 22.6% $10.40 5,000 - 9,999 128 877,709 8,859 11.4% $10.09 10,000 - 24,999 133 2,097,179 18,684 24.0% $8.91 25,000 - 49,999 34 1,236,344 10,427 13.4% $8.43 >50,000 34 3,276,057 22,243 28.6% $6.79 Total / Wtd. Avg. 1,160 9,180,611 $ 77,815 100.0% $8.48 First Quarter 2015 Page 22 Supplemental Financial Reporting Package

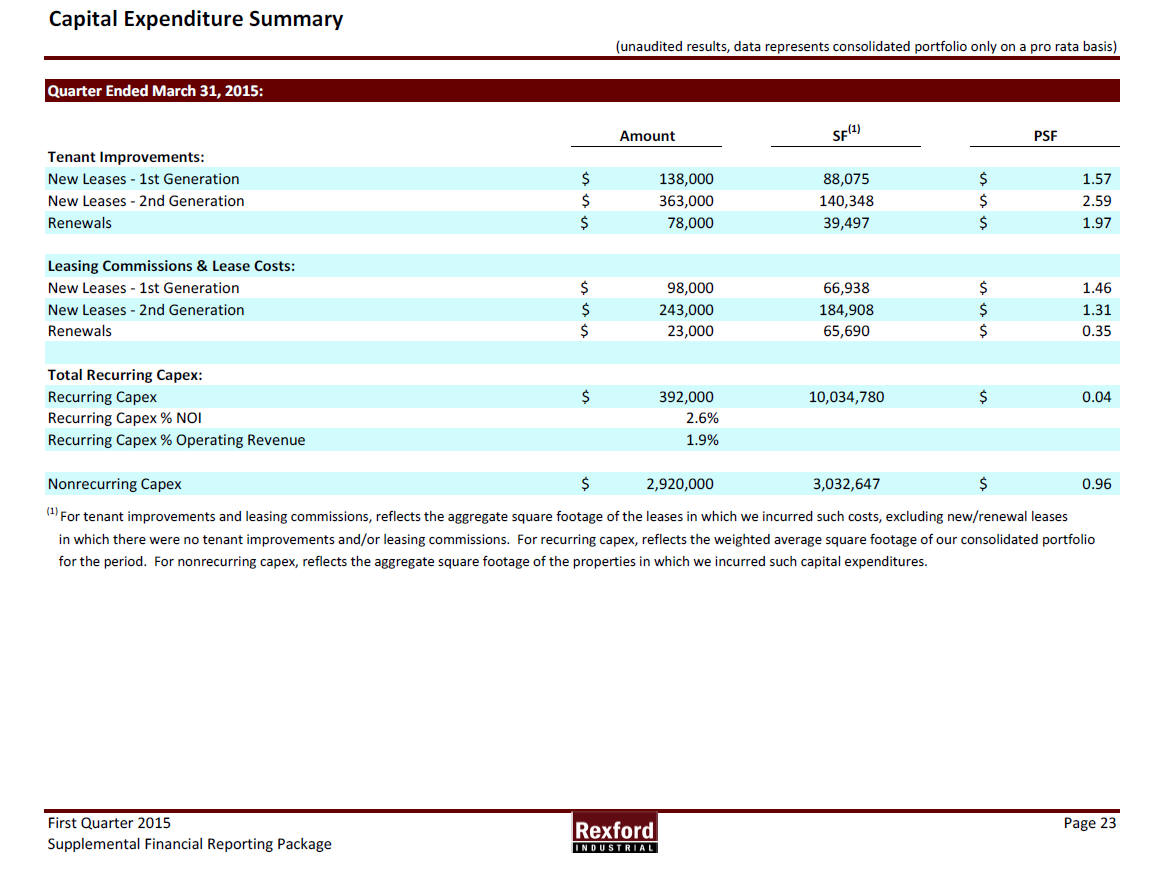

Capital Expenditure Summary (unaudited results, data represents consolidated portfolio only on a pro rata basis) Quarter Ended March 31, 2015: Amount SF(1) PSF Tenant Improvements: New Leases - 1st Generation $ 138,000 88,075 $ 1.57 New Leases - 2nd Generation $ 363,000 140,348 $ 2.59 Renewals $ 78,000 39,497 $ 1.97 Leasing Commissions & Lease Costs: New Leases - 1st Generation $ 98,000 66,938 $ 1.46 New Leases - 2nd Generation $ 243,000 184,908 $ 1.31 Renewals $ 23,000 65,690 $ 0.35 Total Recurring Capex: Recurring Capex $ 392,000 10,034,780 $ 0.04 Recurring Capex % NOI 2.6% Recurring Capex % Operating Revenue 1.9% Nonrecurring Capex $ 2,920,000 3,032,647 $ 0.96 (1) For tenant improvements and leasing commissions, reflects the aggregate square footage of the leases in which we incurred such costs, excluding new/renewal leases in which there were no tenant improvements and/or leasing commissions. For recurring capex, reflects the weighted average square footage of our consolidated portfolio for the period. For nonrecurring capex, reflects the aggregate square footage of the properties in which we incurred such capital expenditures. First Quarter 2015 Page 23 Supplemental Financial Reporting Package

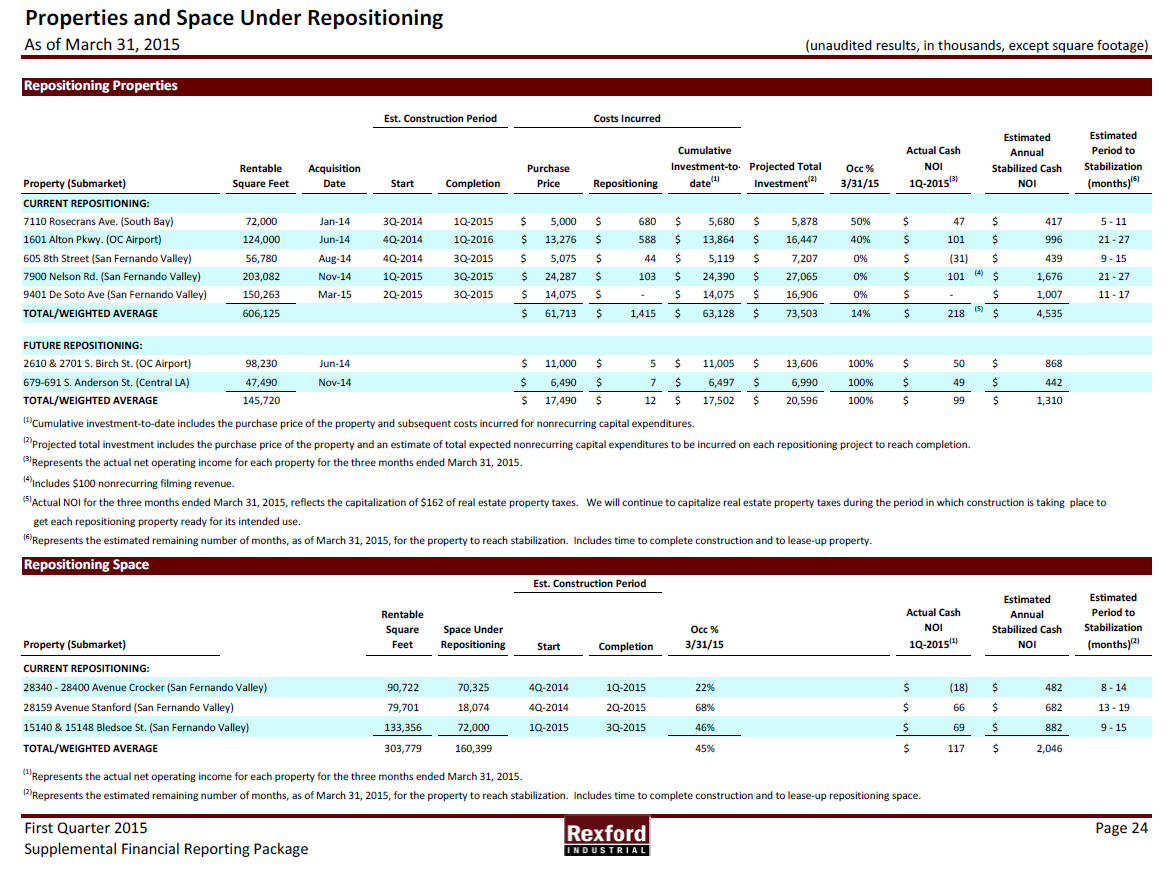

Properties and Space Under Repositioning As of March 31, 2015 (unaudited results, in thousands, except square footage) Repositioning Properties Property (Submarket) Rentable Square Feet Acquisition Date Start Completion Purchase Price Repositioning Cumulative Investment-todate( 1) Projected Total Investment(2) Occ % 3/31/15 Actual Cash NOI 1Q-2015(3) Estimated Annual Stabilized Cash NOI Estimated Period to Stabilization (months)(6) CURRENT REPOSITIONING: 7110 Rosecrans Ave. (South Bay) 72,000 Jan-14 3Q-2014 1Q-2015 $ 5 ,000 $ 6 80 $ 5 ,680 $ 5 ,878 50% $ 4 7 $ 4 17 5 - 11 1601 Alton Pkwy. (OC Airport) 124,000 Jun-14 4Q-2014 1Q-2016 $ 13,276 $ 5 88 $ 1 3,864 $ 1 6,447 40% $ 101 $ 9 96 21 - 27 605 8th Street (San Fernando Valley) 56,780 Aug-14 4Q-2014 3Q-2015 $ 5 ,075 $ 44 $ 5 ,119 $ 7 ,207 0% $ (31) $ 4 39 9 - 15 7900 Nelson Rd. (San Fernando Valley) 203,082 Nov-14 1Q-2015 3Q-2015 $ 24,287 $ 1 03 $ 2 4,390 $ 2 7,065 0% $ 101 (4) $ 1,676 21 - 27 9401 De Soto Ave (San Fernando Valley) 150,263 Mar-15 2Q-2015 3Q-2015 $ 14,075 $ - $ 1 4,075 $ 1 6,906 0% $ - $ 1,007 11 - 17 TOTAL/WEIGHTED AVERAGE 606,125 $ 61,713 $ 1,415 $ 6 3,128 $ 7 3,503 14% $ 218 (5) $ 4,535 FUTURE REPOSITIONING: 2610 & 2701 S. Birch St. (OC Airport) 98,230 Jun-14 $ 11,000 $ 5 $ 1 1,005 $ 1 3,606 100% $ 5 0 $ 8 68 679-691 S. Anderson St. (Central LA) 47,490 Nov-14 $ 6 ,490 $ 7 $ 6 ,497 $ 6 ,990 100% $ 4 9 $ 4 42 TOTAL/WEIGHTED AVERAGE 145,720 $ 17,490 $ 12 $ 1 7,502 $ 2 0,596 100% $ 9 9 $ 1,310 (1)Cumulative investment-to-date includes the purchase price of the property and subsequent costs incurred for nonrecurring capital expenditures. (2)Projected total investment includes the purchase price of the property and an estimate of total expected nonrecurring capital expenditures to be incurred on each repositioning project to reach completion. (3)Represents the actual net operating income for each property for the three months ended March 31, 2015. (4)Includes $100 nonrecurring filming revenue. (5)Actual NOI for the three months ended March 31, 2015, reflects the capitalization of $162 of real estate property taxes. We will continue to capitalize real estate property taxes during the period in which construction is taking place to get each repositioning property ready for its intended use. (6)Represents the estimated remaining number of months, as of March 31, 2015, for the property to reach stabilization. Includes time to complete construction and to lease-up property. Repositioning Space Property (Submarket) Rentable Square Feet Space Under Repositioning Start Completion Occ % 3/31/15 Actual Cash NOI 1Q-2015(1) Estimated Annual Stabilized Cash NOI Estimated Period to Stabilization (months)(2) CURRENT REPOSITIONING: 28340 - 28400 Avenue Crocker (San Fernando Valley) 90,722 70,325 4Q-2014 1Q-2015 22% $ (18) $ 4 82 8 - 14 28159 Avenue Stanford (San Fernando Valley) 79,701 18,074 4Q-2014 2Q-2015 68% $ 6 6 $ 6 82 13 - 19 15140 & 15148 Bledsoe St. (San Fernando Valley) 133,356 72,000 1Q-2015 3Q-2015 46% $ 6 9 $ 8 82 9 - 15 TOTAL/WEIGHTED AVERAGE 303,779 160,399 45% $ 117 $ 2,046 (1)Represents the actual net operating income for each property for the three months ended March 31, 2015. (2)Represents the estimated remaining number of months, as of March 31, 2015, for the property to reach stabilization. Includes time to complete construction and to lease-up repositioning space. First Quarter 2015 Page 24 Supplemental Financial Reporting Package Est. Construction Period Est. Construction Period Costs Incurred

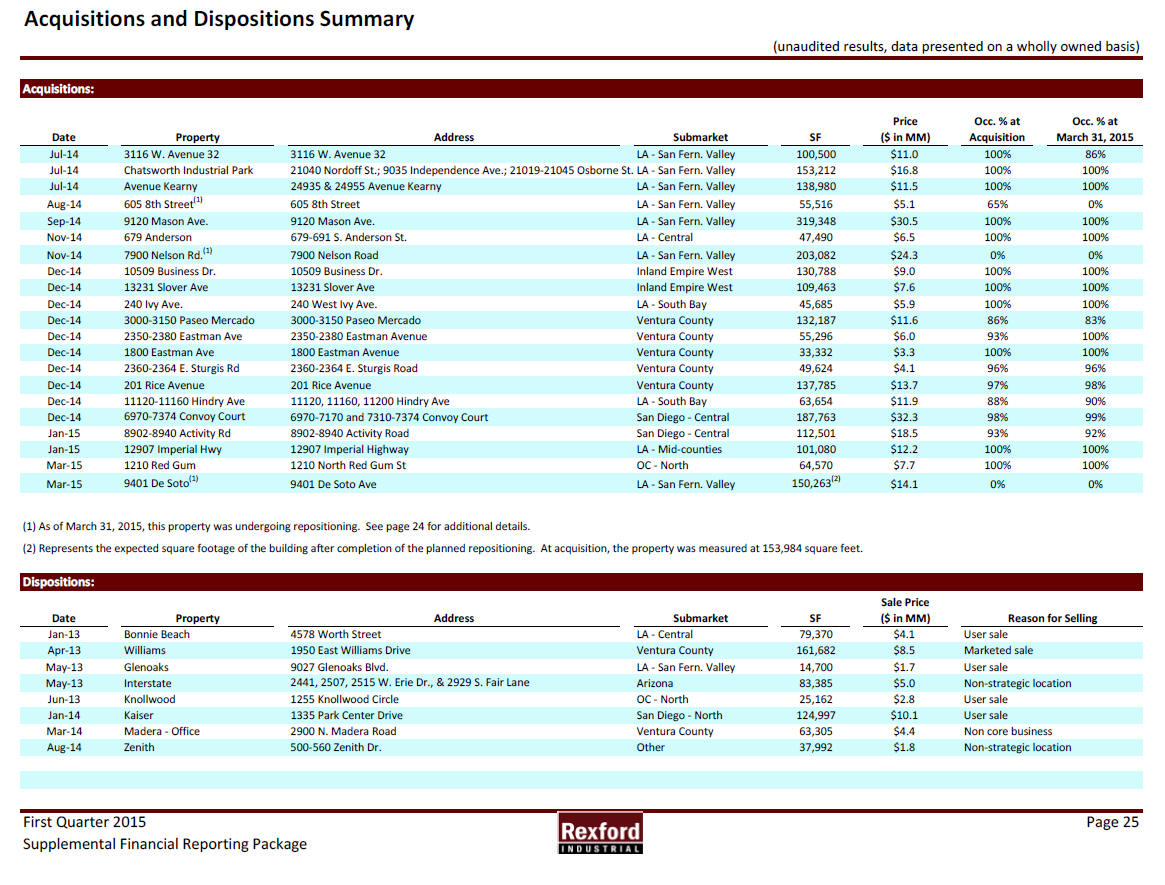

Acquisitions and Dispositions Summary (unaudited results, data presented on a wholly owned basis) Acquisitions: Date Property Address Submarket SF Price ($ in MM) Occ. % at Acquisition Occ. % at March 31, 2015 Jul-14 3116 W. Avenue 32 3116 W. Avenue 32 LA - San Fern. Valley 100,500 $11.0 100% 86% Jul-14 Chatsworth Industrial Park 21040 Nordoff St.; 9035 Independence Ave.; 21019-21045 Osborne St. LA - San Fern. Valley 153,212 $16.8 100% 100% Jul-14 Avenue Kearny 24935 & 24955 Avenue Kearny LA - San Fern. Valley 138,980 $11.5 100% 100% Aug-14 605 8th Street(1) 605 8th Street LA - San Fern. Valley 55,516 $5.1 65% 0% Sep-14 9120 Mason Ave. 9120 Mason Ave. LA - San Fern. Valley 319,348 $30.5 100% 100% Nov-14 679 Anderson 679-691 S. Anderson St. LA - Central 47,490 $6.5 100% 100% Nov-14 7900 Nelson Rd.(1) 7900 Nelson Road LA - San Fern. Valley 203,082 $24.3 0% 0% Dec-14 10509 Business Dr. 10509 Business Dr. Inland Empire West 130,788 $9.0 100% 100% Dec-14 13231 Slover Ave 13231 Slover Ave Inland Empire West 109,463 $7.6 100% 100% Dec-14 240 Ivy Ave. 240 West Ivy Ave. LA - South Bay 45,685 $5.9 100% 100% Dec-14 3000-3150 Paseo Mercado 3000-3150 Paseo Mercado Ventura County 132,187 $11.6 86% 83% Dec-14 2350-2380 Eastman Ave 2350-2380 Eastman Avenue Ventura County 55,296 $6.0 93% 100% Dec-14 1800 Eastman Ave 1800 Eastman Avenue Ventura County 33,332 $3.3 100% 100% Dec-14 2360-2364 E. Sturgis Rd 2360-2364 E. Sturgis Road Ventura County 49,624 $4.1 96% 96% Dec-14 201 Rice Avenue 201 Rice Avenue Ventura County 137,785 $13.7 97% 98% Dec-14 11120-11160 Hindry Ave 11120, 11160, 11200 Hindry Ave LA - South Bay 63,654 $11.9 88% 90% Dec-14 6970-7374 Convoy Court 6970-7170 and 7310-7374 Convoy Court San Diego - Central 187,763 $32.3 98% 99% Jan-15 8902-8940 Activity Rd 8902-8940 Activity Road San Diego - Central 112,501 $18.5 93% 92% Jan-15 12907 Imperial Hwy 12907 Imperial Highway LA - Mid-counties 101,080 $12.2 100% 100% Mar-15 1210 Red Gum 1210 North Red Gum St OC - North 64,570 $7.7 100% 100% Mar-15 9401 De Soto(1) 9401 De Soto Ave LA - San Fern. Valley 150,263(2) $14.1 0% 0% (1) As of March 31, 2015, this property was undergoing repositioning. See page 24 for additional details. (2) Represents the expected square footage of the building after completion of the planned repositioning. At acquisition, the property was measured at 153,984 square feet. Dispositions: Date Property Address Submarket SF Sale Price ($ in MM) Reason for Selling Jan-13 Bonnie Beach 4578 Worth Street LA - Central 79,370 $4.1 User sale Apr-13 Williams 1950 East Williams Drive Ventura County 161,682 $8.5 Marketed sale May-13 Glenoaks 9027 Glenoaks Blvd. LA - San Fern. Valley 14,700 $1.7 User sale May-13 Interstate 2441, 2507, 2515 W. Erie Dr., & 2929 S. Fair Lane Arizona 83,385 $5.0 Non-strategic location Jun-13 Knollwood 1255 Knollwood Circle OC - North 25,162 $2.8 User sale Jan-14 Kaiser 1335 Park Center Drive San Diego - North 124,997 $10.1 User sale Mar-14 Madera - Office 2900 N. Madera Road Ventura County 63,305 $4.4 Non core business Aug-14 Zenith 500-560 Zenith Dr. Other 37,992 $1.8 Non-strategic location First Quarter 2015 Page 25 Supplemental Financial Reporting Package

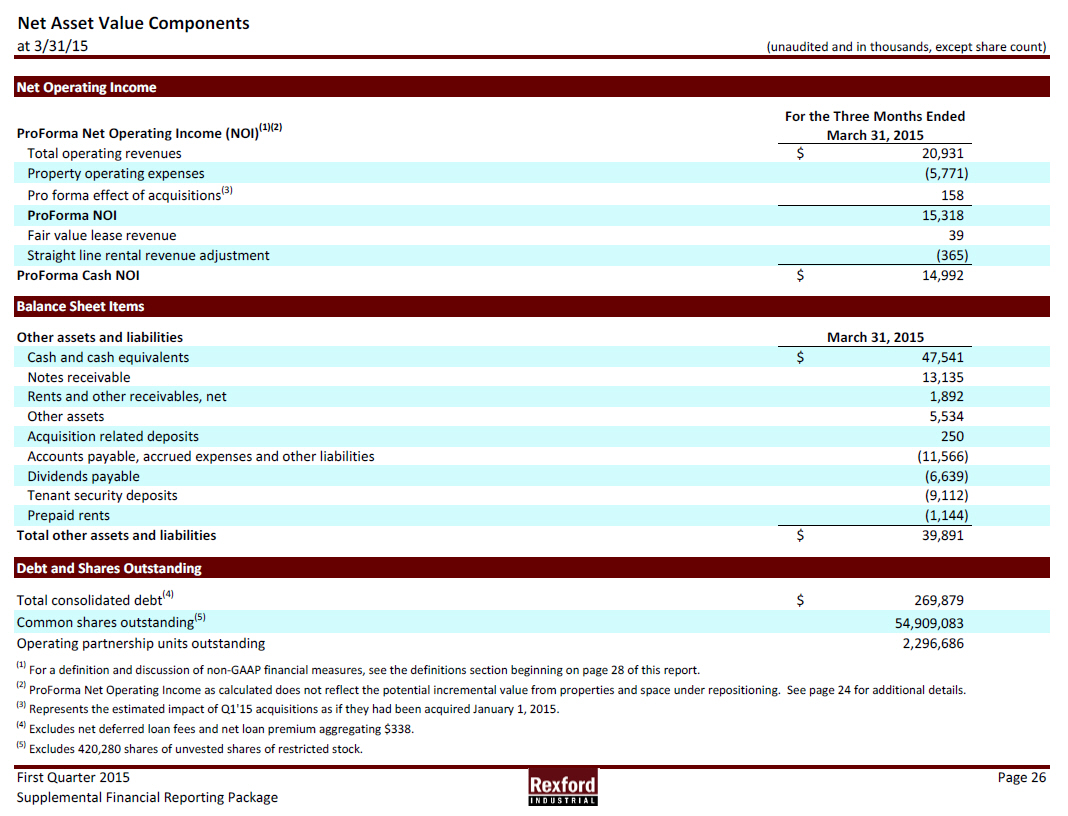

Net Asset Value Components at 3/31/15 (unaudited and in thousands, except share count) ProForma Net Operating Income (NOI)(1)(2) For the Three Months Ended March 31, 2015 Total operating revenues $ 20,931 Property operating expenses (5,771) Pro forma effect of acquisitions(3) 158 ProForma NOI 15,318 Fair value lease revenue 39 Straight line rental revenue adjustment (365) ProForma Cash NOI $ 14,992 Other assets and liabilities March 31, 2015 Cash and cash equivalents $ 47,541 Notes receivable 13,135 Rents and other receivables, net 1,892 Other assets 5,534 Acquisition related deposits 250 Accounts payable, accrued expenses and other liabilities (11,566) Dividends payable (6,639) Tenant security deposits (9,112) Prepaid rents (1,144) Total other assets and liabilities $ 39,891 Total consolidated debt(4) $ 269,879 Common shares outstanding(5) 5 4,909,083 Operating partnership units outstanding 2,296,686 (1) For a definition and discussion of non-GAAP financial measures, see the definitions section beginning on page 28 of this report. (2) ProForma Net Operating Income as calculated does not reflect the potential incremental value from properties and space under repositioning. See page 24 for additional details. (3) Represents the estimated impact of Q1'15 acquisitions as if they had been acquired January 1, 2015. (4) Excludes net deferred loan fees and net loan premium aggregating $338. (5) Excludes 420,280 shares of unvested shares of restricted stock. First Quarter 2015 Page 26 Supplemental Financial Reporting Package Balance Sheet Items Net Operating Income Debt and Shares Outstanding

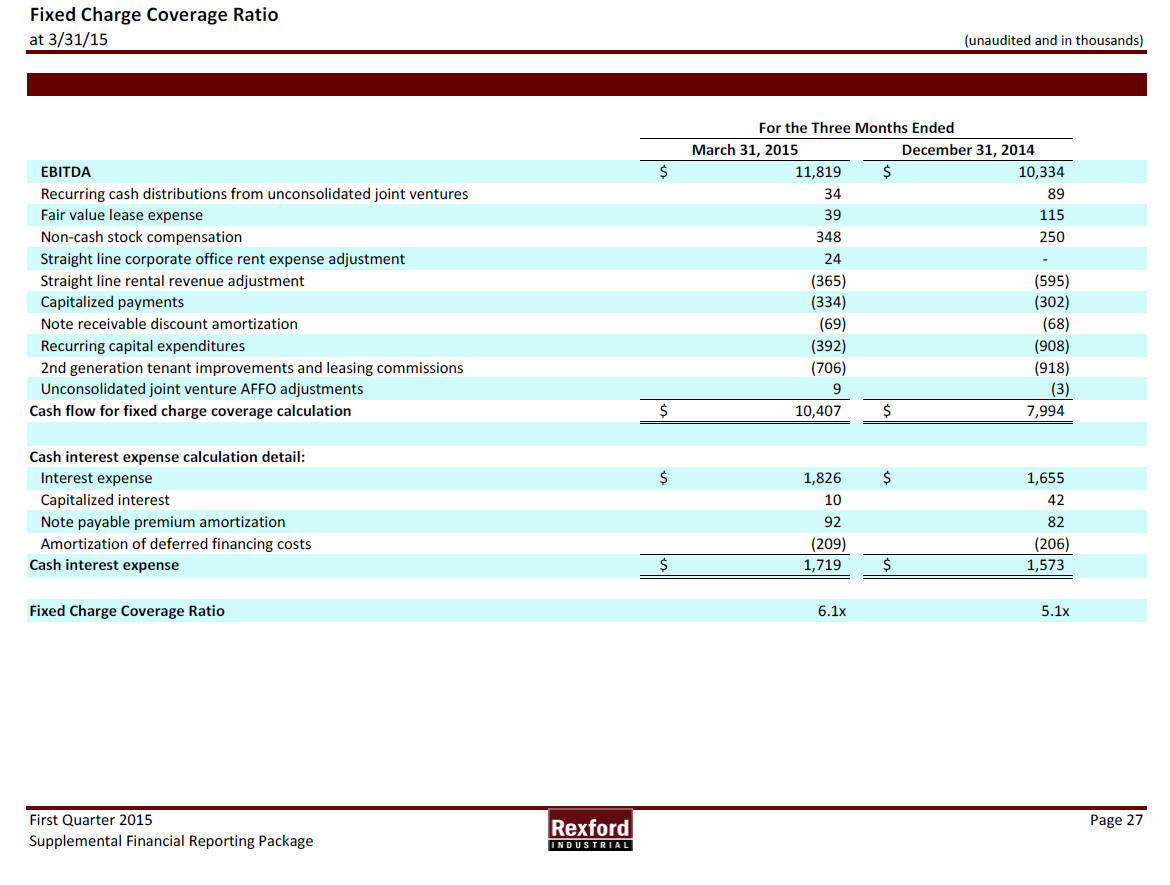

Fixed Charge Coverage Ratio at 3/31/15 (unaudited and in thousands) March 31, 2015 December 31, 2014 EBITDA $ 11,819 $ 10,334 Recurring cash distributions from unconsolidated joint ventures 34 89 Fair value lease expense 39 115 Non-cash stock compensation 348 250 Straight line corporate office rent expense adjustment 24 - Straight line rental revenue adjustment (365) (595) Capitalized payments (334) (302) Note receivable discount amortization (69) (68) Recurring capital expenditures (392) (908) 2nd generation tenant improvements and leasing commissions (706) (918) Unconsolidated joint venture AFFO adjustments 9 (3) Cash flow for fixed charge coverage calculation $ 10,407 $ 7,994 Cash interest expense calculation detail: Interest expense $ 1,826 $ 1,655 Capitalized interest 10 42 Note payable premium amortization 92 82 Amortization of deferred financing costs (209) (206) Cash interest expense $ 1,719 $ 1,573 Fixed Charge Coverage Ratio 6.1x 5.1x First Quarter 2015 Page 27 Supplemental Financial Reporting Package For the Three Months Ended

Definitions / Discussion of Non-GAAP Financial Measures First Quarter 2015 Page 28 Supplemental Financial Reporting Package Adjusted Funds from Operations (AFFO): We calculate adjusted funds from operations, or AFFO, by adding to or subtracting from FFO (i) non-cash operating revenues and expenses, (ii) capitalized operating expenditures such as leasing payroll, (iii) recurring capital expenditures required to maintain and re-tenant our properties, (iv) regular principal payments required to service our debt, and (v) 2nd generation tenant improvements and leasing commissions. Management uses AFFO as a supplemental performance measure because it provides a performance measure that, when compared year over year, captures trends in portfolio operating results. We also believe that, as a widely recognized measure of the performance of REITs, AFFO will be used by investors as a basis to assess our performance in comparison to other REITs. However, because AFFO may exclude certain non-recurring capital expenditures and leasing costs, the utility of AFFO as a measure of our performance is limited. Additionally, other Equity REITs may not calculate AFFO using the method we do. As a result, our AFFO may not be comparable to such other Equity REITs’ AFFO. AFFO should be considered only as a supplement to net income (as computed in accordance with GAAP) as a measure of our performance. Annualized Base Rent: Calculated for each lease as the latest monthly contracted base rent per the terms of such lease multiplied by 12. Excludes billboard and antenna revenue and rent abatements. Capital Expenditures, Non-recurring: Expenditures made in respect of a property for improvement to the appearance of such property or any other major upgrade or renovation of such property, and further includes capital expenditures for seismic upgrades, or capital expenditures for deferred maintenance existing at the time such property was acquired. Capital Expenditures, Recurring: Expenditures made in respect of a property for maintenance of such property and replacement of items due to ordinary wear and tear including, but not limited to, expenditures made for maintenance or replacement of parking lot, roofing materials, mechanical systems, HVAC systems and other structural systems. Recurring capital expenditures shall not include any of the following: (a) improvements to the appearance of such property or any other major upgrade or renovation of such property not necessary for proper maintenance or marketability of such property; (b) capital expenditures for seismic upgrades; or (c) capital expenditures for deferred maintenance for such property existing at the time such property was acquired. Capital Expenditures, First Generation: Capital expenditures for newly acquired space, newly developed or redeveloped space, or change in use. EBITDA and Adjusted EBITDA: We believe that EBITDA is helpful to investors as a supplemental measure of our operating performance as a real estate company because it is a direct measure of the actual operating results of our industrial properties. We also use this measure in ratios to compare our performance to that of our industry peers. In addition, we believe EBITDA is frequently used by securities analysts, investors and other interested parties in the evaluation of Equity REITs. However, because EBITDA is calculated before recurring cash charges including interest expense and income taxes, and is not adjusted for capital expenditures or other recurring cash requirements of our business, its utility as a measure of our liquidity is limited. Accordingly, EBITDA should not be considered an alternative to cash flow from operating activities (as computed in accordance with GAAP) as a measure of our liquidity. EBITDA should not be considered as an alternative to net income or loss as an indicator of our operating performance. Other Equity REITs may calculate EBITDA differently than we do; accordingly, our EBITDA may not be comparable to such other Equity REITs’ EBITDA. Adjusted EBITDA includes add backs of non-cash stock based compensation expense, loss on extinguishment of debt, non-recurring legal fees and the pro-forma effects of acquisitions and assets classified as held for sale. Investment to Date and Total: Reflects the total purchase price for a property plus additional or planned tangible investment subsequent to acquisition. Funds from Operations (FFO): We calculate FFO before non-controlling interest in accordance with the standards established by the National Association of Real Estate Investment Trusts (“NAREIT”). FFO represents net income (loss) (computed in accordance with GAAP), excluding gains (or losses) from sales of depreciable operating property, real estate related depreciation and amortization (excluding amortization of deferred financing costs) and after adjustments for unconsolidated partnerships and joint ventures. Management uses FFO as a supplemental performance measure because, in excluding real estate related depreciation and amortization, gains and losses from property dispositions, other than temporary impairments of unconsolidated real estate entities, and impairment on our investment in real estate, it provides a performance measure that, when compared year over year, captures trends in occupancy rates, rental rates and operating costs. We also believe that, as a widely recognized measure of performance used by other REITs, FFO may be used by investors as a basis to compare our operating performance with that of other REITs. However, because FFO excludes depreciation and amortization and captures neither the changes in the value of our properties that result from use or market conditions nor the level of capital expenditures and leasing commissions necessary to maintain the operating performance of our properties, all of which have real economic effects and could materially impact our results from operations, the utility of FFO as a measure of our performance is limited. Other equity REITs may not calculate or interpret FFO in accordance with the NAREIT definition as we do, and, accordingly, our FFO may not be comparable to such other REITs’ FFO. FFO should not be used as a measure of our liquidity, and is not indicative of funds available for our cash needs, including our ability to pay dividends. Cash NOI: Cash basis NOI is a non-GAAP measure, which we calculate by adding or subtracting from NOI i) fair value lease revenue and ii) straight-line rent adjustment. We use Cash NOI, together with NOI, as a supplemental performance measure. Cash NOI should not be used as a measure of our liquidity, nor is it indicative of funds available to fund our cash needs. Cash NOI should not be used as a substitute for cash flow from operating activities computed in accordance with GAAP. We use Cash NOI to help evaluate the performance of the Company as a whole, as well as the performance of our Same Property Portfolio.

Definitions / Discussion of Non-GAAP Financial Measures First Quarter 2015 Page 29 Supplemental Financial Reporting Package Properties Under Repositioning: Typically defined as properties where a significant amount of space is held vacant in order to implement capital improvements that improve the market rentability and leasing functionality of that space. Considered completed once investment is fully or nearly fully deployed and the property is marketable for leasing. Uncommenced Leases: Reflects signed leases that have not yet commenced as of the reporting date. NOI: Includes the revenue and expense directly attributable to our real estate properties calculated in accordance with GAAP. Calculated as total revenue from real estate operations including i) rental revenues ii) tenant reimbursements, and iii) other income less property expenses and other property expenses (before interest expense, depreciation and amortization). We use NOI as a supplemental performance measure because, in excluding real estate depreciation and amortization expense and gains (or losses) from property dispositions, it provides a performance measure that, when compared year over year, captures trends in occupancy rates, rental rates and operating costs. We also believe that NOI will be useful to investors as a basis to compare our operating performance with that of other REITs. However, because NOI excludes depreciation and amortization expense and captures neither the changes in the value of our properties that result from use or market conditions, nor the level of capital expenditures and leasing commissions necessary to maintain the operating performance of our properties (all of which have real economic effect and could materially impact our results from operations), the utility of NOI as a measure of our performance is limited. Other equity REITs may not calculate NOI in a similar manner and, accordingly, our NOI may not be comparable to such other REITs’ NOI. Accordingly, NOI should be considered only as a supplement to net income as a measure of our performance. NOI should not be used as a measure of our liquidity, nor is it indicative of funds available to fund our cash needs. NOI should not be used as a substitute for cash flow from operating activities in accordance with GAAP. We use NOI to help evaluate the performance of the Company as a whole, as well as the performance of our Same Property Portfolio. Rent Change - Cash: Compares the first month cash rent excluding any abatement on new leases to the last month rent for the most recent expiring lease. Data included for comparable leases only. Comparable leases generally exclude properties under repositioning, short-term leases, and space that has been vacant for over one year. Rent Change - GAAP: Compares GAAP rent, which straightlines rental rate increases and abatement, on new leases to GAAP rent for the most recent expiring lease. Data included for comparable leases only. Comparable leases generally exclude properties under repositioning, short-term leases, and space that has been vacant for over one year. Same Property Portfolio: Determined independently for each period presented. Our Same Property Portfolio is a subset of our consolidated portfolio and includes properties that were wholly-owned by us during the entire span of both periods being compared. The Company’s computation of same property performance may not be comparable to other REITs. Recurring Funds From Operations (Recurring FFO): We calculate Recurring FFO by adjusting FFO to exclude the effect of non-recurring expenses and acquisition expenses. Stabilized Same Property Portfolio: Our Stabilized Same Property Portfolio represents the properties included in our Same Property Portfolio, adjusted to exclude spaces that were under repositioning. Proforma NOI: Proforma NOI is calculated by adding to NOI the estimated impact of current period acquisitions as if they had been acquired at the beginning of the reportable period. These estimates do not purport to be indicative of what operating results would have been had the acquisitions actually occured at the beginning of the reportable period and may not be indicative of future operating results. Space Under Repositioning: Defined as space held vacant in order to implement capital improvements to change the leasing functionality of that space. Considered completed once the repositioning has been completed and the unit is marketable for leasing.